June 19, 2026

Weekly Energy News

Market Update

Natural gas prices remain firm this week, supported by Thursday's bullish EIA storage report and rising summer heat. July 2026 NYMEX futures settled at $3.233/MMBtu on Thursday, June 18 — up 8.8 cents on the day — after the EIA reported a smaller-than-expected 73 Bcf injection for the week ended June 12. The build came in 3 Bcf below the consensus estimate of 76 Bcf and was the smallest weekly build since early May, as rising temperatures pulled more gas into the power sector. Friday, June 19 is the Juneteenth federal holiday; Platts Gas Daily will not publish, and U.S. financial markets are closed.

July 2026 NYMEX was trading at $3.225/MMBtu Friday morning, down approximately 0.8 cents from the prior settlement

· Thursday settlement: $3.233/MMBtu (up 8.8 cents)

· Thursday high: $3.246 | Thursday low: $3.125

Early trading for the prompt month is at $3.224:

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

The storage story is the key driver this week. For the first time this injection season, U.S. working gas inventories have slipped below year-ago levels — now 29 Bcf behind the 2025 comparison week. As recently as April, storage had been running more than 100 Bcf above last year; that cushion is gone, eroded by a combination of strong summer cooling demand, robust LNG feed gas requirements, and more modest injection rates. On the supply side, the Waha Hub in West Texas returned to positive territory on June 16 for the first time since February, settling at $1.850/MMBtu on June 18, reflecting easing Permian Basin takeaway constraints and sustained export demand along the Gulf Coast.

Looking ahead, the focus shifts to summer heat and continued tightening. CERA’s preliminary estimate for the next EIA report (week ending June 19) is 58–68Bcf, well below the five-year average of 75 Bcf for that week — a setup that would further narrow the year-over-year gap. Gas-fired power demand is expected to average roughly 40.5 Bcf/d through early July, with daily peaks approaching or exceeding 43 Bcf/d as population-weighted temperatures climb toward 80°F.

EIA Storage Report

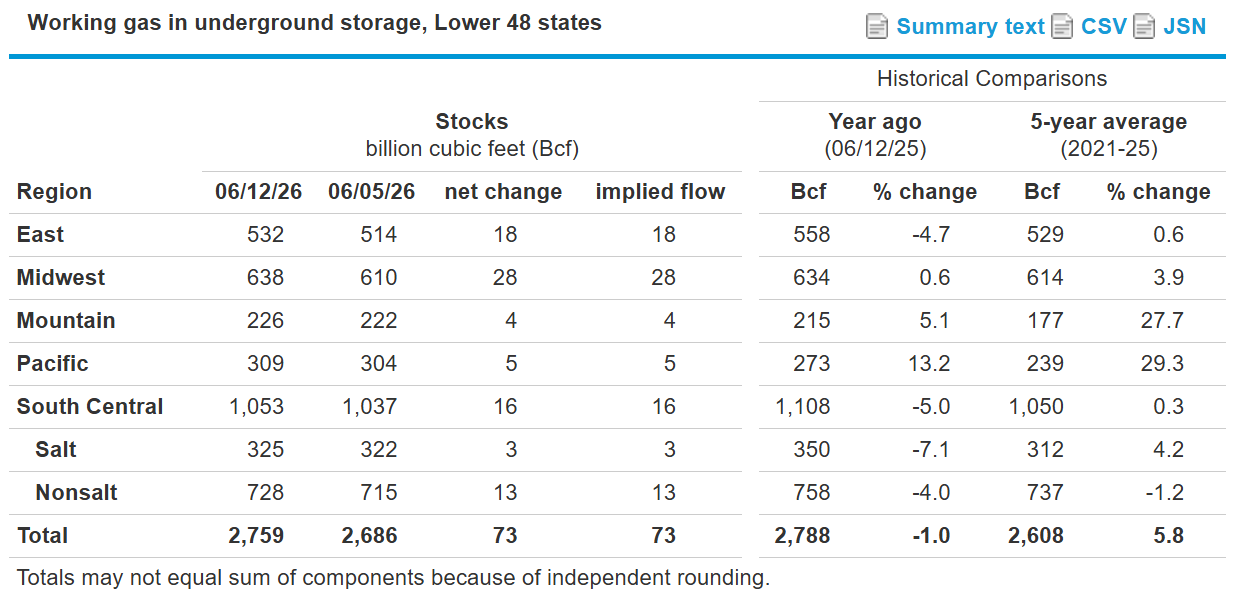

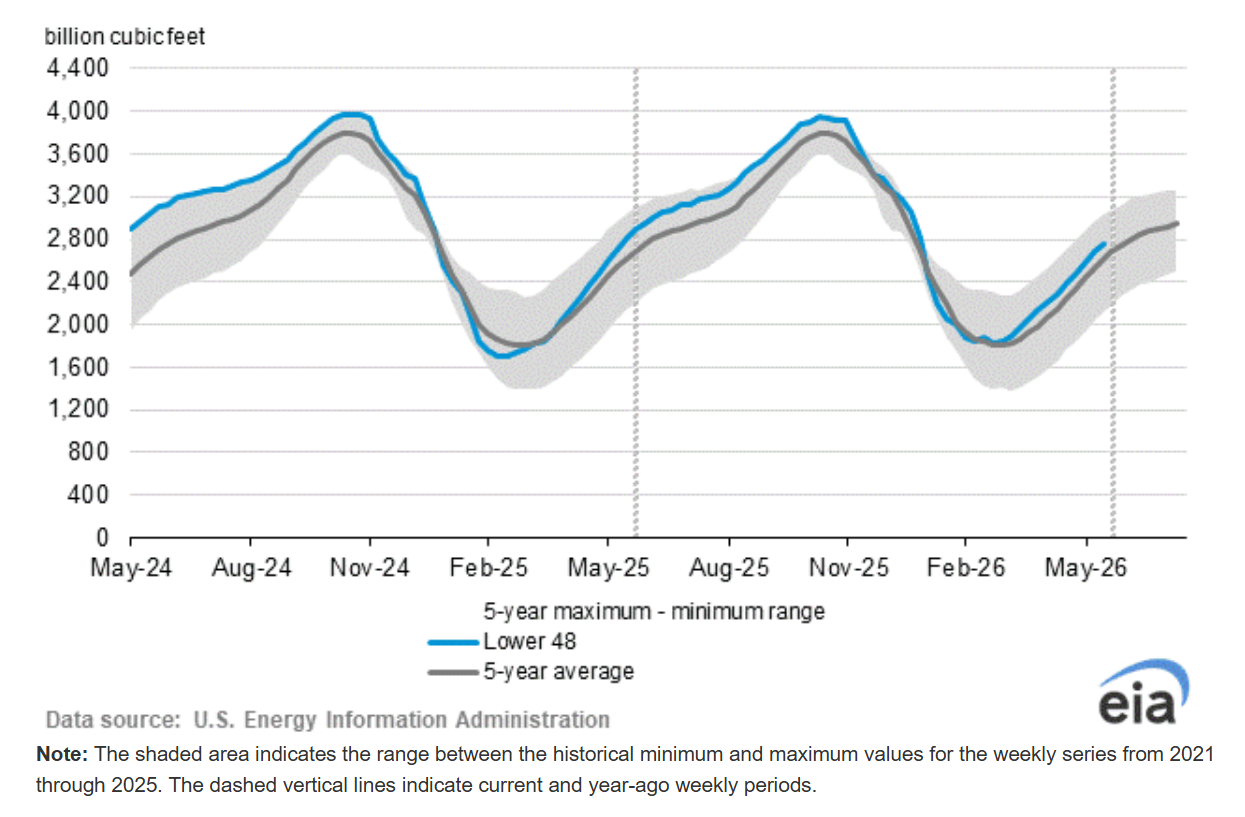

According to the EIA, working natural gas in storage totaled 2,759 Bcf as of June 12, 2026, reflecting a 73 Bcf increase from the prior week. That injection came in 3 Bcf below the Platts consensus estimate of 76 Bcf — the smallest weekly build since early May — and was right in line with the five-year average of 73 Bcf for this week. Total storage is now 151 Bcf above the five-year average of 2,608 Bcf but 29 Bcf below year-ago levels of 2,788 Bcf — the first week this injection season that inventories have slipped below 2025 levels. Overall inventories remain within the historical five-year range.

Weather

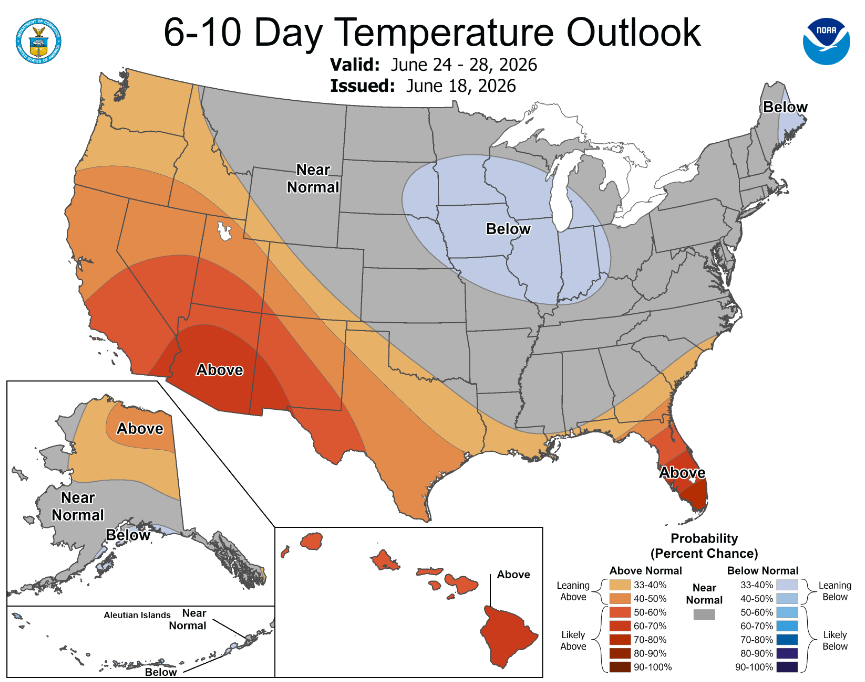

NOAA’s 8–14 Day Outlook (valid June 24–30, 2026) calls for above-normal temperatures across essentially the entire contiguous United States. The strongest probability of above-normal temperatures is concentrated in the South, Southeast, and Florida, where persistent ridging aloft is expected to lock in sustained heat through the period. The West and Central U.S. also lean above normal. Only portions of the far Northern Plains hold any meaningful chance of near-normal temperatures. Population-weighted temperatures are expected to rise to near 80°F by early July, keeping gas-fired power demand elevated and providing fundamental support for natural gas prices heading into peak cooling season.

Market Data:

June 19, 2026

Weekly Energy News

June 19, 2026

Market Update

Natural gas prices remain firm this week, supported by Thursday's bullish EIA storage report and rising summer heat. July 2026 NYMEX futures settled at $3.233/MMBtu on Thursday, June 18 — up 8.8 cents on the day — after the EIA reported a smaller-than-expected 73 Bcf injection for the week ended June 12. The build came in 3 Bcf below the consensus estimate of 76 Bcf and was the smallest weekly build since early May, as rising temperatures pulled more gas into the power sector. Friday, June 19 is the Juneteenth federal holiday; Platts Gas Daily will not publish, and U.S. financial markets are closed.

July 2026 NYMEX was trading at $3.225/MMBtu Friday morning, down approximately 0.8 cents from the prior settlement

· Thursday settlement: $3.233/MMBtu (up 8.8 cents)

· Thursday high: $3.246 | Thursday low: $3.125

Early trading for the prompt month is at $3.224:

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

The storage story is the key driver this week. For the first time this injection season, U.S. working gas inventories have slipped below year-ago levels — now 29 Bcf behind the 2025 comparison week. As recently as April, storage had been running more than 100 Bcf above last year; that cushion is gone, eroded by a combination of strong summer cooling demand, robust LNG feed gas requirements, and more modest injection rates. On the supply side, the Waha Hub in West Texas returned to positive territory on June 16 for the first time since February, settling at $1.850/MMBtu on June 18, reflecting easing Permian Basin takeaway constraints and sustained export demand along the Gulf Coast.

Looking ahead, the focus shifts to summer heat and continued tightening. CERA’s preliminary estimate for the next EIA report (week ending June 19) is 58–68Bcf, well below the five-year average of 75 Bcf for that week — a setup that would further narrow the year-over-year gap. Gas-fired power demand is expected to average roughly 40.5 Bcf/d through early July, with daily peaks approaching or exceeding 43 Bcf/d as population-weighted temperatures climb toward 80°F.

EIA Storage Report

According to the EIA, working natural gas in storage totaled 2,759 Bcf as of June 12, 2026, reflecting a 73 Bcf increase from the prior week. That injection came in 3 Bcf below the Platts consensus estimate of 76 Bcf — the smallest weekly build since early May — and was right in line with the five-year average of 73 Bcf for this week. Total storage is now 151 Bcf above the five-year average of 2,608 Bcf but 29 Bcf below year-ago levels of 2,788 Bcf — the first week this injection season that inventories have slipped below 2025 levels. Overall inventories remain within the historical five-year range.

Weather

NOAA’s 8–14 Day Outlook (valid June 24–30, 2026) calls for above-normal temperatures across essentially the entire contiguous United States. The strongest probability of above-normal temperatures is concentrated in the South, Southeast, and Florida, where persistent ridging aloft is expected to lock in sustained heat through the period. The West and Central U.S. also lean above normal. Only portions of the far Northern Plains hold any meaningful chance of near-normal temperatures. Population-weighted temperatures are expected to rise to near 80°F by early July, keeping gas-fired power demand elevated and providing fundamental support for natural gas prices heading into peak cooling season.

Market Data:

June 19, 2026

June 19, 2026

Weekly Energy News

Market Update

Natural gas prices remain firm this week, supported by Thursday's bullish EIA storage report and rising summer heat. July 2026 NYMEX futures settled at $3.233/MMBtu on Thursday, June 18 — up 8.8 cents on the day — after the EIA reported a smaller-than-expected 73 Bcf injection for the week ended June 12. The build came in 3 Bcf below the consensus estimate of 76 Bcf and was the smallest weekly build since early May, as rising temperatures pulled more gas into the power sector. Friday, June 19 is the Juneteenth federal holiday; Platts Gas Daily will not publish, and U.S. financial markets are closed.

July 2026 NYMEX was trading at $3.225/MMBtu Friday morning, down approximately 0.8 cents from the prior settlement

· Thursday settlement: $3.233/MMBtu (up 8.8 cents)

· Thursday high: $3.246 | Thursday low: $3.125

Early trading for the prompt month is at $3.224:

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

The storage story is the key driver this week. For the first time this injection season, U.S. working gas inventories have slipped below year-ago levels — now 29 Bcf behind the 2025 comparison week. As recently as April, storage had been running more than 100 Bcf above last year; that cushion is gone, eroded by a combination of strong summer cooling demand, robust LNG feed gas requirements, and more modest injection rates. On the supply side, the Waha Hub in West Texas returned to positive territory on June 16 for the first time since February, settling at $1.850/MMBtu on June 18, reflecting easing Permian Basin takeaway constraints and sustained export demand along the Gulf Coast.

Looking ahead, the focus shifts to summer heat and continued tightening. CERA’s preliminary estimate for the next EIA report (week ending June 19) is 58–68Bcf, well below the five-year average of 75 Bcf for that week — a setup that would further narrow the year-over-year gap. Gas-fired power demand is expected to average roughly 40.5 Bcf/d through early July, with daily peaks approaching or exceeding 43 Bcf/d as population-weighted temperatures climb toward 80°F.

EIA Storage Report

According to the EIA, working natural gas in storage totaled 2,759 Bcf as of June 12, 2026, reflecting a 73 Bcf increase from the prior week. That injection came in 3 Bcf below the Platts consensus estimate of 76 Bcf — the smallest weekly build since early May — and was right in line with the five-year average of 73 Bcf for this week. Total storage is now 151 Bcf above the five-year average of 2,608 Bcf but 29 Bcf below year-ago levels of 2,788 Bcf — the first week this injection season that inventories have slipped below 2025 levels. Overall inventories remain within the historical five-year range.

Weather

NOAA’s 8–14 Day Outlook (valid June 24–30, 2026) calls for above-normal temperatures across essentially the entire contiguous United States. The strongest probability of above-normal temperatures is concentrated in the South, Southeast, and Florida, where persistent ridging aloft is expected to lock in sustained heat through the period. The West and Central U.S. also lean above normal. Only portions of the far Northern Plains hold any meaningful chance of near-normal temperatures. Population-weighted temperatures are expected to rise to near 80°F by early July, keeping gas-fired power demand elevated and providing fundamental support for natural gas prices heading into peak cooling season.

June 19, 2026

Weekly Energy News

Market Update

Natural gas prices remain firm this week, supported by Thursday's bullish EIA storage report and rising summer heat. July 2026 NYMEX futures settled at $3.233/MMBtu on Thursday, June 18 — up 8.8 cents on the day — after the EIA reported a smaller-than-expected 73 Bcf injection for the week ended June 12. The build came in 3 Bcf below the consensus estimate of 76 Bcf and was the smallest weekly build since early May, as rising temperatures pulled more gas into the power sector. Friday, June 19 is the Juneteenth federal holiday; Platts Gas Daily will not publish, and U.S. financial markets are closed.

July 2026 NYMEX was trading at $3.225/MMBtu Friday morning, down approximately 0.8 cents from the prior settlement

· Thursday settlement: $3.233/MMBtu (up 8.8 cents)

· Thursday high: $3.246 | Thursday low: $3.125

Early trading for the prompt month is at $3.224:

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

The storage story is the key driver this week. For the first time this injection season, U.S. working gas inventories have slipped below year-ago levels — now 29 Bcf behind the 2025 comparison week. As recently as April, storage had been running more than 100 Bcf above last year; that cushion is gone, eroded by a combination of strong summer cooling demand, robust LNG feed gas requirements, and more modest injection rates. On the supply side, the Waha Hub in West Texas returned to positive territory on June 16 for the first time since February, settling at $1.850/MMBtu on June 18, reflecting easing Permian Basin takeaway constraints and sustained export demand along the Gulf Coast.

Looking ahead, the focus shifts to summer heat and continued tightening. CERA’s preliminary estimate for the next EIA report (week ending June 19) is 58–68Bcf, well below the five-year average of 75 Bcf for that week — a setup that would further narrow the year-over-year gap. Gas-fired power demand is expected to average roughly 40.5 Bcf/d through early July, with daily peaks approaching or exceeding 43 Bcf/d as population-weighted temperatures climb toward 80°F.

EIA Storage Report

According to the EIA, working natural gas in storage totaled 2,759 Bcf as of June 12, 2026, reflecting a 73 Bcf increase from the prior week. That injection came in 3 Bcf below the Platts consensus estimate of 76 Bcf — the smallest weekly build since early May — and was right in line with the five-year average of 73 Bcf for this week. Total storage is now 151 Bcf above the five-year average of 2,608 Bcf but 29 Bcf below year-ago levels of 2,788 Bcf — the first week this injection season that inventories have slipped below 2025 levels. Overall inventories remain within the historical five-year range.

Weather

NOAA’s 8–14 Day Outlook (valid June 24–30, 2026) calls for above-normal temperatures across essentially the entire contiguous United States. The strongest probability of above-normal temperatures is concentrated in the South, Southeast, and Florida, where persistent ridging aloft is expected to lock in sustained heat through the period. The West and Central U.S. also lean above normal. Only portions of the far Northern Plains hold any meaningful chance of near-normal temperatures. Population-weighted temperatures are expected to rise to near 80°F by early July, keeping gas-fired power demand elevated and providing fundamental support for natural gas prices heading into peak cooling season.

June 19, 2026

Weekly Energy News

Market Update

Natural gas prices remain firm this week, supported by Thursday's bullish EIA storage report and rising summer heat. July 2026 NYMEX futures settled at $3.233/MMBtu on Thursday, June 18 — up 8.8 cents on the day — after the EIA reported a smaller-than-expected 73 Bcf injection for the week ended June 12. The build came in 3 Bcf below the consensus estimate of 76 Bcf and was the smallest weekly build since early May, as rising temperatures pulled more gas into the power sector. Friday, June 19 is the Juneteenth federal holiday; Platts Gas Daily will not publish, and U.S. financial markets are closed.

July 2026 NYMEX was trading at $3.225/MMBtu Friday morning, down approximately 0.8 cents from the prior settlement

· Thursday settlement: $3.233/MMBtu (up 8.8 cents)

· Thursday high: $3.246 | Thursday low: $3.125

Early trading for the prompt month is at $3.224:

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

The storage story is the key driver this week. For the first time this injection season, U.S. working gas inventories have slipped below year-ago levels — now 29 Bcf behind the 2025 comparison week. As recently as April, storage had been running more than 100 Bcf above last year; that cushion is gone, eroded by a combination of strong summer cooling demand, robust LNG feed gas requirements, and more modest injection rates. On the supply side, the Waha Hub in West Texas returned to positive territory on June 16 for the first time since February, settling at $1.850/MMBtu on June 18, reflecting easing Permian Basin takeaway constraints and sustained export demand along the Gulf Coast.

Looking ahead, the focus shifts to summer heat and continued tightening. CERA’s preliminary estimate for the next EIA report (week ending June 19) is 58–68Bcf, well below the five-year average of 75 Bcf for that week — a setup that would further narrow the year-over-year gap. Gas-fired power demand is expected to average roughly 40.5 Bcf/d through early July, with daily peaks approaching or exceeding 43 Bcf/d as population-weighted temperatures climb toward 80°F.

EIA Storage Report

According to the EIA, working natural gas in storage totaled 2,759 Bcf as of June 12, 2026, reflecting a 73 Bcf increase from the prior week. That injection came in 3 Bcf below the Platts consensus estimate of 76 Bcf — the smallest weekly build since early May — and was right in line with the five-year average of 73 Bcf for this week. Total storage is now 151 Bcf above the five-year average of 2,608 Bcf but 29 Bcf below year-ago levels of 2,788 Bcf — the first week this injection season that inventories have slipped below 2025 levels. Overall inventories remain within the historical five-year range.

Weather

NOAA’s 8–14 Day Outlook (valid June 24–30, 2026) calls for above-normal temperatures across essentially the entire contiguous United States. The strongest probability of above-normal temperatures is concentrated in the South, Southeast, and Florida, where persistent ridging aloft is expected to lock in sustained heat through the period. The West and Central U.S. also lean above normal. Only portions of the far Northern Plains hold any meaningful chance of near-normal temperatures. Population-weighted temperatures are expected to rise to near 80°F by early July, keeping gas-fired power demand elevated and providing fundamental support for natural gas prices heading into peak cooling season.

June 19, 2026

Market Update

Natural gas prices remain firm this week, supported by Thursday's bullish EIA storage report and rising summer heat. July 2026 NYMEX futures settled at $3.233/MMBtu on Thursday, June 18 — up 8.8 cents on the day — after the EIA reported a smaller-than-expected 73 Bcf injection for the week ended June 12. The build came in 3 Bcf below the consensus estimate of 76 Bcf and was the smallest weekly build since early May, as rising temperatures pulled more gas into the power sector. Friday, June 19 is the Juneteenth federal holiday; Platts Gas Daily will not publish, and U.S. financial markets are closed.

July 2026 NYMEX was trading at $3.225/MMBtu Friday morning, down approximately 0.8 cents from the prior settlement

· Thursday settlement: $3.233/MMBtu (up 8.8 cents)

· Thursday high: $3.246 | Thursday low: $3.125

Early trading for the prompt month is at $3.224:

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

The storage story is the key driver this week. For the first time this injection season, U.S. working gas inventories have slipped below year-ago levels — now 29 Bcf behind the 2025 comparison week. As recently as April, storage had been running more than 100 Bcf above last year; that cushion is gone, eroded by a combination of strong summer cooling demand, robust LNG feed gas requirements, and more modest injection rates. On the supply side, the Waha Hub in West Texas returned to positive territory on June 16 for the first time since February, settling at $1.850/MMBtu on June 18, reflecting easing Permian Basin takeaway constraints and sustained export demand along the Gulf Coast.

Looking ahead, the focus shifts to summer heat and continued tightening. CERA’s preliminary estimate for the next EIA report (week ending June 19) is 58–68Bcf, well below the five-year average of 75 Bcf for that week — a setup that would further narrow the year-over-year gap. Gas-fired power demand is expected to average roughly 40.5 Bcf/d through early July, with daily peaks approaching or exceeding 43 Bcf/d as population-weighted temperatures climb toward 80°F.

EIA Storage Report

According to the EIA, working natural gas in storage totaled 2,759 Bcf as of June 12, 2026, reflecting a 73 Bcf increase from the prior week. That injection came in 3 Bcf below the Platts consensus estimate of 76 Bcf — the smallest weekly build since early May — and was right in line with the five-year average of 73 Bcf for this week. Total storage is now 151 Bcf above the five-year average of 2,608 Bcf but 29 Bcf below year-ago levels of 2,788 Bcf — the first week this injection season that inventories have slipped below 2025 levels. Overall inventories remain within the historical five-year range.

Weather

NOAA’s 8–14 Day Outlook (valid June 24–30, 2026) calls for above-normal temperatures across essentially the entire contiguous United States. The strongest probability of above-normal temperatures is concentrated in the South, Southeast, and Florida, where persistent ridging aloft is expected to lock in sustained heat through the period. The West and Central U.S. also lean above normal. Only portions of the far Northern Plains hold any meaningful chance of near-normal temperatures. Population-weighted temperatures are expected to rise to near 80°F by early July, keeping gas-fired power demand elevated and providing fundamental support for natural gas prices heading into peak cooling season.

June 19, 2026

Weekly Energy News

Market Update

Natural gas prices remain firm this week, supported by Thursday's bullish EIA storage report and rising summer heat. July 2026 NYMEX futures settled at $3.233/MMBtu on Thursday, June 18 — up 8.8 cents on the day — after the EIA reported a smaller-than-expected 73 Bcf injection for the week ended June 12. The build came in 3 Bcf below the consensus estimate of 76 Bcf and was the smallest weekly build since early May, as rising temperatures pulled more gas into the power sector. Friday, June 19 is the Juneteenth federal holiday; Platts Gas Daily will not publish, and U.S. financial markets are closed.

July 2026 NYMEX was trading at $3.225/MMBtu Friday morning, down approximately 0.8 cents from the prior settlement

· Thursday settlement: $3.233/MMBtu (up 8.8 cents)

· Thursday high: $3.246 | Thursday low: $3.125

Early trading for the prompt month is at $3.224:

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

The storage story is the key driver this week. For the first time this injection season, U.S. working gas inventories have slipped below year-ago levels — now 29 Bcf behind the 2025 comparison week. As recently as April, storage had been running more than 100 Bcf above last year; that cushion is gone, eroded by a combination of strong summer cooling demand, robust LNG feed gas requirements, and more modest injection rates. On the supply side, the Waha Hub in West Texas returned to positive territory on June 16 for the first time since February, settling at $1.850/MMBtu on June 18, reflecting easing Permian Basin takeaway constraints and sustained export demand along the Gulf Coast.

Looking ahead, the focus shifts to summer heat and continued tightening. CERA’s preliminary estimate for the next EIA report (week ending June 19) is 58–68Bcf, well below the five-year average of 75 Bcf for that week — a setup that would further narrow the year-over-year gap. Gas-fired power demand is expected to average roughly 40.5 Bcf/d through early July, with daily peaks approaching or exceeding 43 Bcf/d as population-weighted temperatures climb toward 80°F.

EIA Storage Report

According to the EIA, working natural gas in storage totaled 2,759 Bcf as of June 12, 2026, reflecting a 73 Bcf increase from the prior week. That injection came in 3 Bcf below the Platts consensus estimate of 76 Bcf — the smallest weekly build since early May — and was right in line with the five-year average of 73 Bcf for this week. Total storage is now 151 Bcf above the five-year average of 2,608 Bcf but 29 Bcf below year-ago levels of 2,788 Bcf — the first week this injection season that inventories have slipped below 2025 levels. Overall inventories remain within the historical five-year range.

Weather

NOAA’s 8–14 Day Outlook (valid June 24–30, 2026) calls for above-normal temperatures across essentially the entire contiguous United States. The strongest probability of above-normal temperatures is concentrated in the South, Southeast, and Florida, where persistent ridging aloft is expected to lock in sustained heat through the period. The West and Central U.S. also lean above normal. Only portions of the far Northern Plains hold any meaningful chance of near-normal temperatures. Population-weighted temperatures are expected to rise to near 80°F by early July, keeping gas-fired power demand elevated and providing fundamental support for natural gas prices heading into peak cooling season.

June 19, 2026

Weekly Energy News

Market Update

Natural gas prices remain firm this week, supported by Thursday's bullish EIA storage report and rising summer heat. July 2026 NYMEX futures settled at $3.233/MMBtu on Thursday, June 18 — up 8.8 cents on the day — after the EIA reported a smaller-than-expected 73 Bcf injection for the week ended June 12. The build came in 3 Bcf below the consensus estimate of 76 Bcf and was the smallest weekly build since early May, as rising temperatures pulled more gas into the power sector. Friday, June 19 is the Juneteenth federal holiday; Platts Gas Daily will not publish, and U.S. financial markets are closed.

July 2026 NYMEX was trading at $3.225/MMBtu Friday morning, down approximately 0.8 cents from the prior settlement

· Thursday settlement: $3.233/MMBtu (up 8.8 cents)

· Thursday high: $3.246 | Thursday low: $3.125

Early trading for the prompt month is at $3.224:

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

The storage story is the key driver this week. For the first time this injection season, U.S. working gas inventories have slipped below year-ago levels — now 29 Bcf behind the 2025 comparison week. As recently as April, storage had been running more than 100 Bcf above last year; that cushion is gone, eroded by a combination of strong summer cooling demand, robust LNG feed gas requirements, and more modest injection rates. On the supply side, the Waha Hub in West Texas returned to positive territory on June 16 for the first time since February, settling at $1.850/MMBtu on June 18, reflecting easing Permian Basin takeaway constraints and sustained export demand along the Gulf Coast.

Looking ahead, the focus shifts to summer heat and continued tightening. CERA’s preliminary estimate for the next EIA report (week ending June 19) is 58–68Bcf, well below the five-year average of 75 Bcf for that week — a setup that would further narrow the year-over-year gap. Gas-fired power demand is expected to average roughly 40.5 Bcf/d through early July, with daily peaks approaching or exceeding 43 Bcf/d as population-weighted temperatures climb toward 80°F.

EIA Storage Report

According to the EIA, working natural gas in storage totaled 2,759 Bcf as of June 12, 2026, reflecting a 73 Bcf increase from the prior week. That injection came in 3 Bcf below the Platts consensus estimate of 76 Bcf — the smallest weekly build since early May — and was right in line with the five-year average of 73 Bcf for this week. Total storage is now 151 Bcf above the five-year average of 2,608 Bcf but 29 Bcf below year-ago levels of 2,788 Bcf — the first week this injection season that inventories have slipped below 2025 levels. Overall inventories remain within the historical five-year range.

Weather

NOAA’s 8–14 Day Outlook (valid June 24–30, 2026) calls for above-normal temperatures across essentially the entire contiguous United States. The strongest probability of above-normal temperatures is concentrated in the South, Southeast, and Florida, where persistent ridging aloft is expected to lock in sustained heat through the period. The West and Central U.S. also lean above normal. Only portions of the far Northern Plains hold any meaningful chance of near-normal temperatures. Population-weighted temperatures are expected to rise to near 80°F by early July, keeping gas-fired power demand elevated and providing fundamental support for natural gas prices heading into peak cooling season.

Make Your Choice Gas Selection in Three Easy Steps

Click here to access our online tool, or call our Choice gas commodity experts at 1 (877) 790-4990.

Step 1: Enter your account number

- Your Black Hills Energy account number is located at the top right-hand corner of your bill.

Step 2: Review price options and make your selection

Step 3: Confirm your selection and enter your control number

- You received a control number in your 2026 Choice Gas selection packet mailed to you from Black Hills Energy. If you cannot locate this, you can retrieve your control number by calling 877-245-3506 or visit choicegas.com

Once enrolled, you will be removed from supplier marketing communications within 24 hours.

Sign Up for Our Energy Newsletters

Sign UpRecent Posts