June 12, 2026

Weekly Energy News

Market Update

Natural gas markets pulled back this week after the EIA reported a 108-Bcf injection — 10 Bcf above the Platts consensus of 98 Bcf and the largest weekly build since June 2025. The July contract dropped approximately 5-6 cents following the report, hitting an intraday low of $3.054/MMBtu.

July 2026 NYMEX closed Thursday at $3.087

High for the day $3.204

Low for the day $3.054

Early trading for the prompt month is trading at $3.084

https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

https://www.fxempire.com/commodities/natural-gas

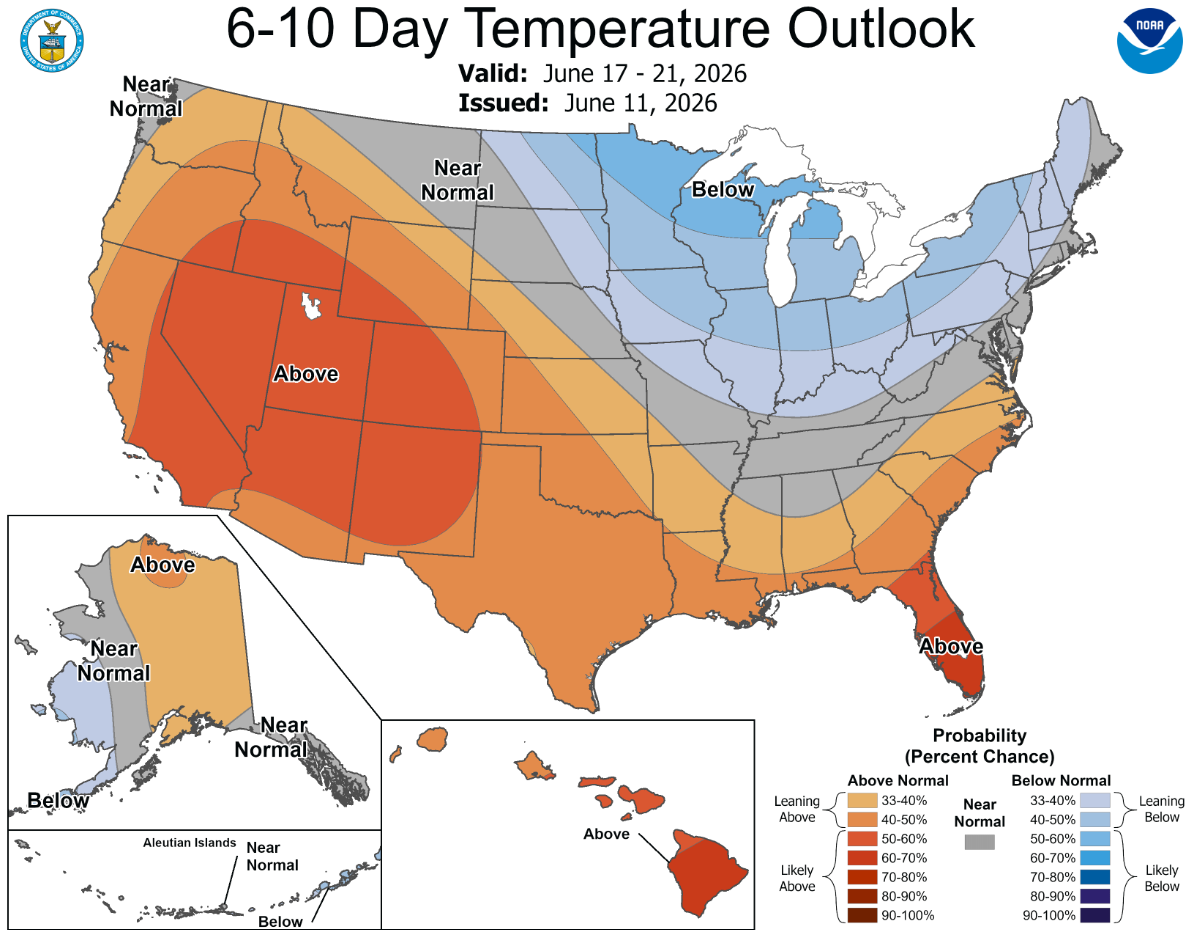

Near-term weather has added to the pressure. The Great Lakes region faces a 40-50% chance of cooler-than-normal temperatures June 17-21, and US gas-fired power demand is projected to average roughly 41.6 Bcf/d through June 25 — below year-ago levels.

On the supply side, Freeport LNG completed maintenance on one liquefaction train June 11, pushing total USLNG feedgas demand to 19.3 Bcf/d — still below the ~20.5 Bcf/d April average but a positive sign for demand recovery.

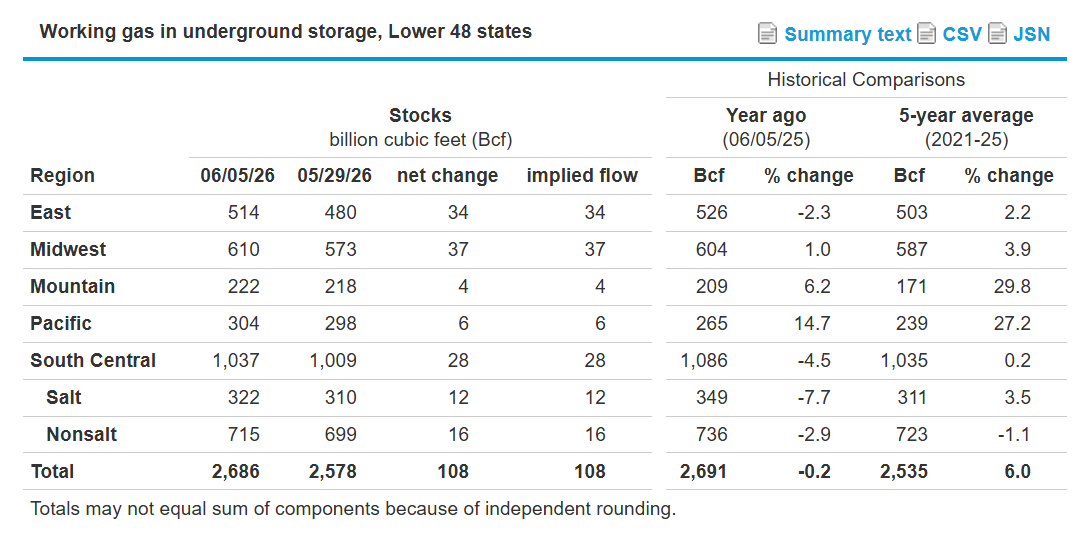

Total US storage stands at2,686 Bcf — 151 Bcf above the five-year average but now 5 Bcf below year-ago levels, a notable shift from the surplus the market carried earlier in the injection season.

Analysts project the next EIA report will show an injection of ~79 Bcf, slightly above the five-year average of 73 Bcf but well below last year's 97-Bcf injection.

EIA Storage Report

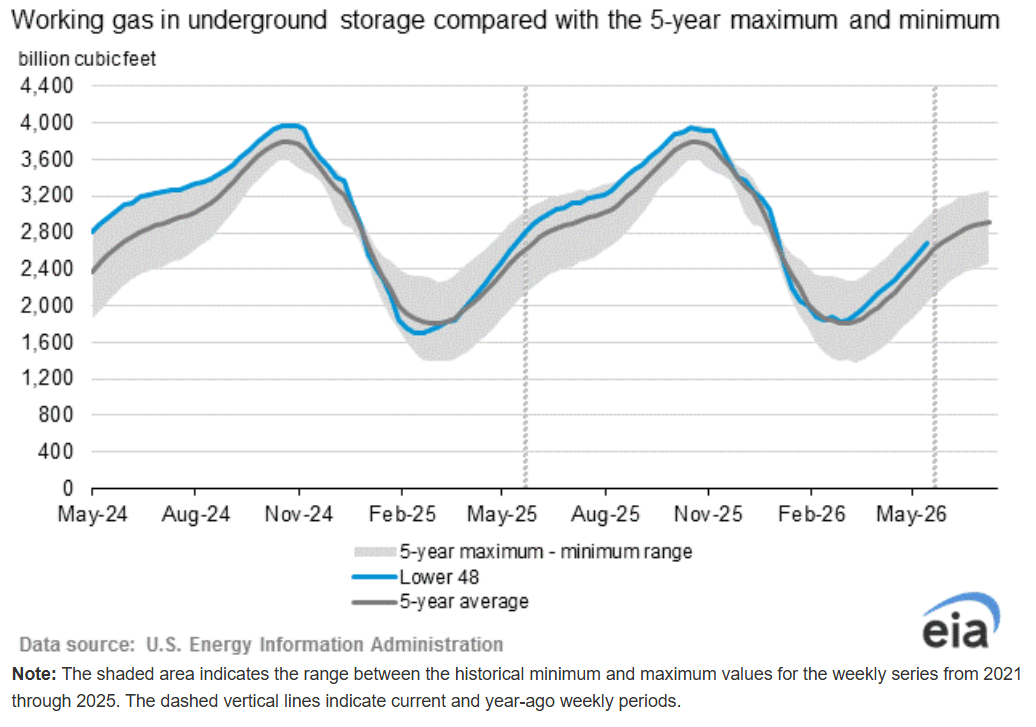

Working gas in storage totaled 2,686 Bcf as of June 5, 2026 — a 108-Bcf weekly increase that exceeded the five-year average build of 95 Bcf and the year-ago addition of 110 Bcf. Inventories are 151 Bcf above the five-year average of 2,535 Bcf and 5 Bcf below year-ago levels, remaining within the historical five-year range.

Weather

NOAA confirmed this week that El Niño has officially formed and is expected to strengthen significantly through 2026. There is a ~90% chance it reaches at least "strong" intensity, a 60%+ chance of "very strong," and roughly a one-in-three chance of a rare "super El Niño." WMO puts the probability of El Niño persisting through at least November 2026 at ~90%.

For gas markets, El Niño typically brings warmer, drier conditions — supporting stronger summer cooling demand and higher power-sector gas burn. It also tends to suppress Atlantic hurricane activity; NOAA forecasts a below-normal season with 8-14 named storms, reducing but not eliminating the risk of Gulf Coast production disruptions.

Near-term, the picture is more mixed: cooler-than-normal temperatures are expected across the Midwest and Great Lakes through mid-to-late June. The July outlook calls for above-normal temperatures across most of the country, which should support demand heading into the peak of summer.

Market Data:

June 12, 2026

Weekly Energy News

June 12, 2026

Market Update

Natural gas markets pulled back this week after the EIA reported a 108-Bcf injection — 10 Bcf above the Platts consensus of 98 Bcf and the largest weekly build since June 2025. The July contract dropped approximately 5-6 cents following the report, hitting an intraday low of $3.054/MMBtu.

July 2026 NYMEX closed Thursday at $3.087

High for the day $3.204

Low for the day $3.054

Early trading for the prompt month is trading at $3.084

https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

https://www.fxempire.com/commodities/natural-gas

Near-term weather has added to the pressure. The Great Lakes region faces a 40-50% chance of cooler-than-normal temperatures June 17-21, and US gas-fired power demand is projected to average roughly 41.6 Bcf/d through June 25 — below year-ago levels.

On the supply side, Freeport LNG completed maintenance on one liquefaction train June 11, pushing total USLNG feedgas demand to 19.3 Bcf/d — still below the ~20.5 Bcf/d April average but a positive sign for demand recovery.

Total US storage stands at2,686 Bcf — 151 Bcf above the five-year average but now 5 Bcf below year-ago levels, a notable shift from the surplus the market carried earlier in the injection season.

Analysts project the next EIA report will show an injection of ~79 Bcf, slightly above the five-year average of 73 Bcf but well below last year's 97-Bcf injection.

EIA Storage Report

Working gas in storage totaled 2,686 Bcf as of June 5, 2026 — a 108-Bcf weekly increase that exceeded the five-year average build of 95 Bcf and the year-ago addition of 110 Bcf. Inventories are 151 Bcf above the five-year average of 2,535 Bcf and 5 Bcf below year-ago levels, remaining within the historical five-year range.

Weather

NOAA confirmed this week that El Niño has officially formed and is expected to strengthen significantly through 2026. There is a ~90% chance it reaches at least "strong" intensity, a 60%+ chance of "very strong," and roughly a one-in-three chance of a rare "super El Niño." WMO puts the probability of El Niño persisting through at least November 2026 at ~90%.

For gas markets, El Niño typically brings warmer, drier conditions — supporting stronger summer cooling demand and higher power-sector gas burn. It also tends to suppress Atlantic hurricane activity; NOAA forecasts a below-normal season with 8-14 named storms, reducing but not eliminating the risk of Gulf Coast production disruptions.

Near-term, the picture is more mixed: cooler-than-normal temperatures are expected across the Midwest and Great Lakes through mid-to-late June. The July outlook calls for above-normal temperatures across most of the country, which should support demand heading into the peak of summer.

Market Data:

June 12, 2026

June 12, 2026

Weekly Energy News

Market Update

Natural gas markets pulled back this week after the EIA reported a 108-Bcf injection — 10 Bcf above the Platts consensus of 98 Bcf and the largest weekly build since June 2025. The July contract dropped approximately 5-6 cents following the report, hitting an intraday low of $3.054/MMBtu.

July 2026 NYMEX closed Thursday at $3.087

High for the day $3.204

Low for the day $3.054

Early trading for the prompt month is trading at $3.084

https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

https://www.fxempire.com/commodities/natural-gas

Near-term weather has added to the pressure. The Great Lakes region faces a 40-50% chance of cooler-than-normal temperatures June 17-21, and US gas-fired power demand is projected to average roughly 41.6 Bcf/d through June 25 — below year-ago levels.

On the supply side, Freeport LNG completed maintenance on one liquefaction train June 11, pushing total USLNG feedgas demand to 19.3 Bcf/d — still below the ~20.5 Bcf/d April average but a positive sign for demand recovery.

Total US storage stands at2,686 Bcf — 151 Bcf above the five-year average but now 5 Bcf below year-ago levels, a notable shift from the surplus the market carried earlier in the injection season.

Analysts project the next EIA report will show an injection of ~79 Bcf, slightly above the five-year average of 73 Bcf but well below last year's 97-Bcf injection.

EIA Storage Report

Working gas in storage totaled 2,686 Bcf as of June 5, 2026 — a 108-Bcf weekly increase that exceeded the five-year average build of 95 Bcf and the year-ago addition of 110 Bcf. Inventories are 151 Bcf above the five-year average of 2,535 Bcf and 5 Bcf below year-ago levels, remaining within the historical five-year range.

Weather

NOAA confirmed this week that El Niño has officially formed and is expected to strengthen significantly through 2026. There is a ~90% chance it reaches at least "strong" intensity, a 60%+ chance of "very strong," and roughly a one-in-three chance of a rare "super El Niño." WMO puts the probability of El Niño persisting through at least November 2026 at ~90%.

For gas markets, El Niño typically brings warmer, drier conditions — supporting stronger summer cooling demand and higher power-sector gas burn. It also tends to suppress Atlantic hurricane activity; NOAA forecasts a below-normal season with 8-14 named storms, reducing but not eliminating the risk of Gulf Coast production disruptions.

Near-term, the picture is more mixed: cooler-than-normal temperatures are expected across the Midwest and Great Lakes through mid-to-late June. The July outlook calls for above-normal temperatures across most of the country, which should support demand heading into the peak of summer.

June 12, 2026

Weekly Energy News

Market Update

Natural gas markets pulled back this week after the EIA reported a 108-Bcf injection — 10 Bcf above the Platts consensus of 98 Bcf and the largest weekly build since June 2025. The July contract dropped approximately 5-6 cents following the report, hitting an intraday low of $3.054/MMBtu.

July 2026 NYMEX closed Thursday at $3.087

High for the day $3.204

Low for the day $3.054

Early trading for the prompt month is trading at $3.084

https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

https://www.fxempire.com/commodities/natural-gas

Near-term weather has added to the pressure. The Great Lakes region faces a 40-50% chance of cooler-than-normal temperatures June 17-21, and US gas-fired power demand is projected to average roughly 41.6 Bcf/d through June 25 — below year-ago levels.

On the supply side, Freeport LNG completed maintenance on one liquefaction train June 11, pushing total USLNG feedgas demand to 19.3 Bcf/d — still below the ~20.5 Bcf/d April average but a positive sign for demand recovery.

Total US storage stands at2,686 Bcf — 151 Bcf above the five-year average but now 5 Bcf below year-ago levels, a notable shift from the surplus the market carried earlier in the injection season.

Analysts project the next EIA report will show an injection of ~79 Bcf, slightly above the five-year average of 73 Bcf but well below last year's 97-Bcf injection.

EIA Storage Report

Working gas in storage totaled 2,686 Bcf as of June 5, 2026 — a 108-Bcf weekly increase that exceeded the five-year average build of 95 Bcf and the year-ago addition of 110 Bcf. Inventories are 151 Bcf above the five-year average of 2,535 Bcf and 5 Bcf below year-ago levels, remaining within the historical five-year range.

Weather

NOAA confirmed this week that El Niño has officially formed and is expected to strengthen significantly through 2026. There is a ~90% chance it reaches at least "strong" intensity, a 60%+ chance of "very strong," and roughly a one-in-three chance of a rare "super El Niño." WMO puts the probability of El Niño persisting through at least November 2026 at ~90%.

For gas markets, El Niño typically brings warmer, drier conditions — supporting stronger summer cooling demand and higher power-sector gas burn. It also tends to suppress Atlantic hurricane activity; NOAA forecasts a below-normal season with 8-14 named storms, reducing but not eliminating the risk of Gulf Coast production disruptions.

Near-term, the picture is more mixed: cooler-than-normal temperatures are expected across the Midwest and Great Lakes through mid-to-late June. The July outlook calls for above-normal temperatures across most of the country, which should support demand heading into the peak of summer.

June 12, 2026

Weekly Energy News

Market Update

Natural gas markets pulled back this week after the EIA reported a 108-Bcf injection — 10 Bcf above the Platts consensus of 98 Bcf and the largest weekly build since June 2025. The July contract dropped approximately 5-6 cents following the report, hitting an intraday low of $3.054/MMBtu.

July 2026 NYMEX closed Thursday at $3.087

High for the day $3.204

Low for the day $3.054

Early trading for the prompt month is trading at $3.084

https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

https://www.fxempire.com/commodities/natural-gas

Near-term weather has added to the pressure. The Great Lakes region faces a 40-50% chance of cooler-than-normal temperatures June 17-21, and US gas-fired power demand is projected to average roughly 41.6 Bcf/d through June 25 — below year-ago levels.

On the supply side, Freeport LNG completed maintenance on one liquefaction train June 11, pushing total USLNG feedgas demand to 19.3 Bcf/d — still below the ~20.5 Bcf/d April average but a positive sign for demand recovery.

Total US storage stands at2,686 Bcf — 151 Bcf above the five-year average but now 5 Bcf below year-ago levels, a notable shift from the surplus the market carried earlier in the injection season.

Analysts project the next EIA report will show an injection of ~79 Bcf, slightly above the five-year average of 73 Bcf but well below last year's 97-Bcf injection.

EIA Storage Report

Working gas in storage totaled 2,686 Bcf as of June 5, 2026 — a 108-Bcf weekly increase that exceeded the five-year average build of 95 Bcf and the year-ago addition of 110 Bcf. Inventories are 151 Bcf above the five-year average of 2,535 Bcf and 5 Bcf below year-ago levels, remaining within the historical five-year range.

Weather

NOAA confirmed this week that El Niño has officially formed and is expected to strengthen significantly through 2026. There is a ~90% chance it reaches at least "strong" intensity, a 60%+ chance of "very strong," and roughly a one-in-three chance of a rare "super El Niño." WMO puts the probability of El Niño persisting through at least November 2026 at ~90%.

For gas markets, El Niño typically brings warmer, drier conditions — supporting stronger summer cooling demand and higher power-sector gas burn. It also tends to suppress Atlantic hurricane activity; NOAA forecasts a below-normal season with 8-14 named storms, reducing but not eliminating the risk of Gulf Coast production disruptions.

Near-term, the picture is more mixed: cooler-than-normal temperatures are expected across the Midwest and Great Lakes through mid-to-late June. The July outlook calls for above-normal temperatures across most of the country, which should support demand heading into the peak of summer.

June 12, 2026

Market Update

Natural gas markets pulled back this week after the EIA reported a 108-Bcf injection — 10 Bcf above the Platts consensus of 98 Bcf and the largest weekly build since June 2025. The July contract dropped approximately 5-6 cents following the report, hitting an intraday low of $3.054/MMBtu.

July 2026 NYMEX closed Thursday at $3.087

High for the day $3.204

Low for the day $3.054

Early trading for the prompt month is trading at $3.084

https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

https://www.fxempire.com/commodities/natural-gas

Near-term weather has added to the pressure. The Great Lakes region faces a 40-50% chance of cooler-than-normal temperatures June 17-21, and US gas-fired power demand is projected to average roughly 41.6 Bcf/d through June 25 — below year-ago levels.

On the supply side, Freeport LNG completed maintenance on one liquefaction train June 11, pushing total USLNG feedgas demand to 19.3 Bcf/d — still below the ~20.5 Bcf/d April average but a positive sign for demand recovery.

Total US storage stands at2,686 Bcf — 151 Bcf above the five-year average but now 5 Bcf below year-ago levels, a notable shift from the surplus the market carried earlier in the injection season.

Analysts project the next EIA report will show an injection of ~79 Bcf, slightly above the five-year average of 73 Bcf but well below last year's 97-Bcf injection.

EIA Storage Report

Working gas in storage totaled 2,686 Bcf as of June 5, 2026 — a 108-Bcf weekly increase that exceeded the five-year average build of 95 Bcf and the year-ago addition of 110 Bcf. Inventories are 151 Bcf above the five-year average of 2,535 Bcf and 5 Bcf below year-ago levels, remaining within the historical five-year range.

Weather

NOAA confirmed this week that El Niño has officially formed and is expected to strengthen significantly through 2026. There is a ~90% chance it reaches at least "strong" intensity, a 60%+ chance of "very strong," and roughly a one-in-three chance of a rare "super El Niño." WMO puts the probability of El Niño persisting through at least November 2026 at ~90%.

For gas markets, El Niño typically brings warmer, drier conditions — supporting stronger summer cooling demand and higher power-sector gas burn. It also tends to suppress Atlantic hurricane activity; NOAA forecasts a below-normal season with 8-14 named storms, reducing but not eliminating the risk of Gulf Coast production disruptions.

Near-term, the picture is more mixed: cooler-than-normal temperatures are expected across the Midwest and Great Lakes through mid-to-late June. The July outlook calls for above-normal temperatures across most of the country, which should support demand heading into the peak of summer.

June 12, 2026

Weekly Energy News

Market Update

Natural gas markets pulled back this week after the EIA reported a 108-Bcf injection — 10 Bcf above the Platts consensus of 98 Bcf and the largest weekly build since June 2025. The July contract dropped approximately 5-6 cents following the report, hitting an intraday low of $3.054/MMBtu.

July 2026 NYMEX closed Thursday at $3.087

High for the day $3.204

Low for the day $3.054

Early trading for the prompt month is trading at $3.084

https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

https://www.fxempire.com/commodities/natural-gas

Near-term weather has added to the pressure. The Great Lakes region faces a 40-50% chance of cooler-than-normal temperatures June 17-21, and US gas-fired power demand is projected to average roughly 41.6 Bcf/d through June 25 — below year-ago levels.

On the supply side, Freeport LNG completed maintenance on one liquefaction train June 11, pushing total USLNG feedgas demand to 19.3 Bcf/d — still below the ~20.5 Bcf/d April average but a positive sign for demand recovery.

Total US storage stands at2,686 Bcf — 151 Bcf above the five-year average but now 5 Bcf below year-ago levels, a notable shift from the surplus the market carried earlier in the injection season.

Analysts project the next EIA report will show an injection of ~79 Bcf, slightly above the five-year average of 73 Bcf but well below last year's 97-Bcf injection.

EIA Storage Report

Working gas in storage totaled 2,686 Bcf as of June 5, 2026 — a 108-Bcf weekly increase that exceeded the five-year average build of 95 Bcf and the year-ago addition of 110 Bcf. Inventories are 151 Bcf above the five-year average of 2,535 Bcf and 5 Bcf below year-ago levels, remaining within the historical five-year range.

Weather

NOAA confirmed this week that El Niño has officially formed and is expected to strengthen significantly through 2026. There is a ~90% chance it reaches at least "strong" intensity, a 60%+ chance of "very strong," and roughly a one-in-three chance of a rare "super El Niño." WMO puts the probability of El Niño persisting through at least November 2026 at ~90%.

For gas markets, El Niño typically brings warmer, drier conditions — supporting stronger summer cooling demand and higher power-sector gas burn. It also tends to suppress Atlantic hurricane activity; NOAA forecasts a below-normal season with 8-14 named storms, reducing but not eliminating the risk of Gulf Coast production disruptions.

Near-term, the picture is more mixed: cooler-than-normal temperatures are expected across the Midwest and Great Lakes through mid-to-late June. The July outlook calls for above-normal temperatures across most of the country, which should support demand heading into the peak of summer.

June 12, 2026

Weekly Energy News

Market Update

Natural gas markets pulled back this week after the EIA reported a 108-Bcf injection — 10 Bcf above the Platts consensus of 98 Bcf and the largest weekly build since June 2025. The July contract dropped approximately 5-6 cents following the report, hitting an intraday low of $3.054/MMBtu.

July 2026 NYMEX closed Thursday at $3.087

High for the day $3.204

Low for the day $3.054

Early trading for the prompt month is trading at $3.084

https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

https://www.fxempire.com/commodities/natural-gas

Near-term weather has added to the pressure. The Great Lakes region faces a 40-50% chance of cooler-than-normal temperatures June 17-21, and US gas-fired power demand is projected to average roughly 41.6 Bcf/d through June 25 — below year-ago levels.

On the supply side, Freeport LNG completed maintenance on one liquefaction train June 11, pushing total USLNG feedgas demand to 19.3 Bcf/d — still below the ~20.5 Bcf/d April average but a positive sign for demand recovery.

Total US storage stands at2,686 Bcf — 151 Bcf above the five-year average but now 5 Bcf below year-ago levels, a notable shift from the surplus the market carried earlier in the injection season.

Analysts project the next EIA report will show an injection of ~79 Bcf, slightly above the five-year average of 73 Bcf but well below last year's 97-Bcf injection.

EIA Storage Report

Working gas in storage totaled 2,686 Bcf as of June 5, 2026 — a 108-Bcf weekly increase that exceeded the five-year average build of 95 Bcf and the year-ago addition of 110 Bcf. Inventories are 151 Bcf above the five-year average of 2,535 Bcf and 5 Bcf below year-ago levels, remaining within the historical five-year range.

Weather

NOAA confirmed this week that El Niño has officially formed and is expected to strengthen significantly through 2026. There is a ~90% chance it reaches at least "strong" intensity, a 60%+ chance of "very strong," and roughly a one-in-three chance of a rare "super El Niño." WMO puts the probability of El Niño persisting through at least November 2026 at ~90%.

For gas markets, El Niño typically brings warmer, drier conditions — supporting stronger summer cooling demand and higher power-sector gas burn. It also tends to suppress Atlantic hurricane activity; NOAA forecasts a below-normal season with 8-14 named storms, reducing but not eliminating the risk of Gulf Coast production disruptions.

Near-term, the picture is more mixed: cooler-than-normal temperatures are expected across the Midwest and Great Lakes through mid-to-late June. The July outlook calls for above-normal temperatures across most of the country, which should support demand heading into the peak of summer.

Make Your Choice Gas Selection in Three Easy Steps

Click here to access our online tool, or call our Choice gas commodity experts at 1 (877) 790-4990.

Step 1: Enter your account number

- Your Black Hills Energy account number is located at the top right-hand corner of your bill.

Step 2: Review price options and make your selection

Step 3: Confirm your selection and enter your control number

- You received a control number in your 2026 Choice Gas selection packet mailed to you from Black Hills Energy. If you cannot locate this, you can retrieve your control number by calling 877-245-3506 or visit choicegas.com

Once enrolled, you will be removed from supplier marketing communications within 24 hours.

Sign Up for Our Energy Newsletters

Sign UpRecent Posts