May 8, 2026

Weekly Energy News

Market Update: The U.S. Energy Information Administration reported on May 7, a 63 Bcf injection for the prior week that came in below market expectations.

Following the release of the EIA storage report, the NYMEX June natural gas futures contract climbed nearly 10 cents over the next hour, reaching an intraday high of $2.80/MMBtu as traders reacted to the tighter-than-expected build, according to CME Group data.

The reported injection was 7 Bcf, or roughly 10%, below the consensus estimate from the Platts gas storage survey, which had projected a 70-Bcf increase in inventories for the week ending May 1.

After hitting the upper $2.80s/MMBtu, the prompt-month June contract had pulled back in recent sessions, falling as low as $2.67/MMBtu in the hour leading up to the EIA report.

Despite the post-report rally, analysts noted that prices may face renewed downward pressure amid relatively loose market fundamentals.

“Natural gas market fundamentals remain soft, with storage 153 Bcf above five-year norms, LNG demand down 2.5 Bcf/d from April highs, and production recovering,” said Eli Rubin, senior energy analyst at EBW Analytics, in a May 7 market note.

Rubin also noted that weather-related demand could weaken further as late-season heating needs fade, with a projected 50-gHDD decline in heating demand from Week 1 to Week 3 potentially reopening the door for triple-digit weekly storage injections.

Looking ahead, most analysts expect the EIA’s first storage report for May to show a slightly larger build, likely in the low-70 Bcf range.

June 2026 NYMEX closed Thursday at $2.769

· High for the day $2.813

· Low for the day $2.676

Early trading for the prompt month is trading at $2.785

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

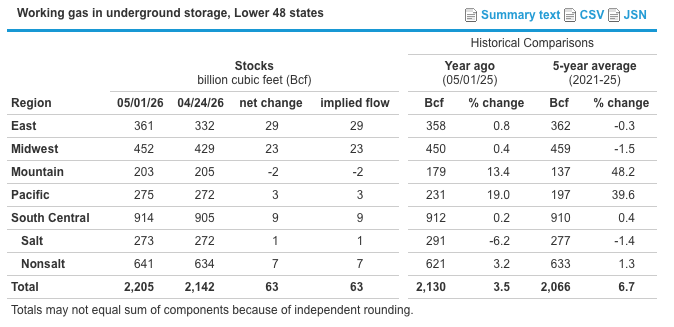

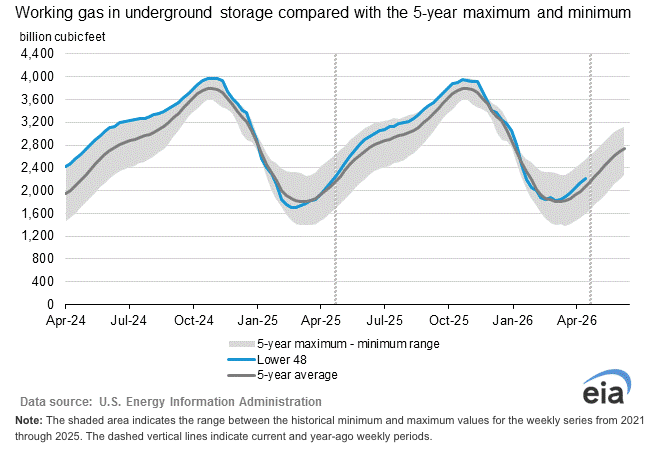

EIA Storage Report: According to EIA estimates, working gas in storage totaled 2,205 Bcf as of Friday, May 1, 2026, reflecting a net injection of 63 Bcf from the prior week. Storage levels were 75 Bcf above the same time last year and 139 Bcf higher than the five-year average of 2,066 Bcf. Total working gas inventories remain within the historical five-year range.

Weather: The updated May outlook calls for a highly variable weather pattern across the U.S. as forecasters monitor shifting atmospheric conditions, the Madden-Julian Oscillation (MJO), and the potential development of El Niño later this summer.

After an unusually warm start to spring, a major pattern shift has brought cooler-than-normal temperatures to the eastern half of the country. Several cold fronts are expected to keep temperatures below normal across parts of the Great Plains, Great Lakes, and Northeast through early May.

By mid-month, forecast models indicate warmer conditions returning as upper-level ridging expands across much of the U.S. This transition is expected to push temperatures above normal across much of the central and western U.S., with the strongest warmth focused in the Pacific Northwest. Due to the expected swings between cooler and warmer periods, much of the eastern U.S. is forecast to see near-normal temperatures overall for the month.

On the precipitation side, above-normal rainfall is favored from Texas through the Gulf Coast and Lower Mississippi Valley during the first half of May, with the heaviest precipitation expected across portions of southeastern Texas and Louisiana. Wetter-than-normal conditions are also possible across parts of the Southeast and eastern Maine.

Meanwhile, drier-than-normal conditions are expected across the Pacific Northwest, Northern Rockies, and portions of the Northern and Central Plains as warmer and more stable weather develops later in the month.

Market Data:

May 8, 2026

Weekly Energy News

May 8, 2026

Market Update: The U.S. Energy Information Administration reported on May 7, a 63 Bcf injection for the prior week that came in below market expectations.

Following the release of the EIA storage report, the NYMEX June natural gas futures contract climbed nearly 10 cents over the next hour, reaching an intraday high of $2.80/MMBtu as traders reacted to the tighter-than-expected build, according to CME Group data.

The reported injection was 7 Bcf, or roughly 10%, below the consensus estimate from the Platts gas storage survey, which had projected a 70-Bcf increase in inventories for the week ending May 1.

After hitting the upper $2.80s/MMBtu, the prompt-month June contract had pulled back in recent sessions, falling as low as $2.67/MMBtu in the hour leading up to the EIA report.

Despite the post-report rally, analysts noted that prices may face renewed downward pressure amid relatively loose market fundamentals.

“Natural gas market fundamentals remain soft, with storage 153 Bcf above five-year norms, LNG demand down 2.5 Bcf/d from April highs, and production recovering,” said Eli Rubin, senior energy analyst at EBW Analytics, in a May 7 market note.

Rubin also noted that weather-related demand could weaken further as late-season heating needs fade, with a projected 50-gHDD decline in heating demand from Week 1 to Week 3 potentially reopening the door for triple-digit weekly storage injections.

Looking ahead, most analysts expect the EIA’s first storage report for May to show a slightly larger build, likely in the low-70 Bcf range.

June 2026 NYMEX closed Thursday at $2.769

· High for the day $2.813

· Low for the day $2.676

Early trading for the prompt month is trading at $2.785

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: According to EIA estimates, working gas in storage totaled 2,205 Bcf as of Friday, May 1, 2026, reflecting a net injection of 63 Bcf from the prior week. Storage levels were 75 Bcf above the same time last year and 139 Bcf higher than the five-year average of 2,066 Bcf. Total working gas inventories remain within the historical five-year range.

Weather: The updated May outlook calls for a highly variable weather pattern across the U.S. as forecasters monitor shifting atmospheric conditions, the Madden-Julian Oscillation (MJO), and the potential development of El Niño later this summer.

After an unusually warm start to spring, a major pattern shift has brought cooler-than-normal temperatures to the eastern half of the country. Several cold fronts are expected to keep temperatures below normal across parts of the Great Plains, Great Lakes, and Northeast through early May.

By mid-month, forecast models indicate warmer conditions returning as upper-level ridging expands across much of the U.S. This transition is expected to push temperatures above normal across much of the central and western U.S., with the strongest warmth focused in the Pacific Northwest. Due to the expected swings between cooler and warmer periods, much of the eastern U.S. is forecast to see near-normal temperatures overall for the month.

On the precipitation side, above-normal rainfall is favored from Texas through the Gulf Coast and Lower Mississippi Valley during the first half of May, with the heaviest precipitation expected across portions of southeastern Texas and Louisiana. Wetter-than-normal conditions are also possible across parts of the Southeast and eastern Maine.

Meanwhile, drier-than-normal conditions are expected across the Pacific Northwest, Northern Rockies, and portions of the Northern and Central Plains as warmer and more stable weather develops later in the month.

Market Data:

May 8, 2026

May 8, 2026

Weekly Energy News

Market Update: The U.S. Energy Information Administration reported on May 7, a 63 Bcf injection for the prior week that came in below market expectations.

Following the release of the EIA storage report, the NYMEX June natural gas futures contract climbed nearly 10 cents over the next hour, reaching an intraday high of $2.80/MMBtu as traders reacted to the tighter-than-expected build, according to CME Group data.

The reported injection was 7 Bcf, or roughly 10%, below the consensus estimate from the Platts gas storage survey, which had projected a 70-Bcf increase in inventories for the week ending May 1.

After hitting the upper $2.80s/MMBtu, the prompt-month June contract had pulled back in recent sessions, falling as low as $2.67/MMBtu in the hour leading up to the EIA report.

Despite the post-report rally, analysts noted that prices may face renewed downward pressure amid relatively loose market fundamentals.

“Natural gas market fundamentals remain soft, with storage 153 Bcf above five-year norms, LNG demand down 2.5 Bcf/d from April highs, and production recovering,” said Eli Rubin, senior energy analyst at EBW Analytics, in a May 7 market note.

Rubin also noted that weather-related demand could weaken further as late-season heating needs fade, with a projected 50-gHDD decline in heating demand from Week 1 to Week 3 potentially reopening the door for triple-digit weekly storage injections.

Looking ahead, most analysts expect the EIA’s first storage report for May to show a slightly larger build, likely in the low-70 Bcf range.

June 2026 NYMEX closed Thursday at $2.769

· High for the day $2.813

· Low for the day $2.676

Early trading for the prompt month is trading at $2.785

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: According to EIA estimates, working gas in storage totaled 2,205 Bcf as of Friday, May 1, 2026, reflecting a net injection of 63 Bcf from the prior week. Storage levels were 75 Bcf above the same time last year and 139 Bcf higher than the five-year average of 2,066 Bcf. Total working gas inventories remain within the historical five-year range.

Weather: The updated May outlook calls for a highly variable weather pattern across the U.S. as forecasters monitor shifting atmospheric conditions, the Madden-Julian Oscillation (MJO), and the potential development of El Niño later this summer.

After an unusually warm start to spring, a major pattern shift has brought cooler-than-normal temperatures to the eastern half of the country. Several cold fronts are expected to keep temperatures below normal across parts of the Great Plains, Great Lakes, and Northeast through early May.

By mid-month, forecast models indicate warmer conditions returning as upper-level ridging expands across much of the U.S. This transition is expected to push temperatures above normal across much of the central and western U.S., with the strongest warmth focused in the Pacific Northwest. Due to the expected swings between cooler and warmer periods, much of the eastern U.S. is forecast to see near-normal temperatures overall for the month.

On the precipitation side, above-normal rainfall is favored from Texas through the Gulf Coast and Lower Mississippi Valley during the first half of May, with the heaviest precipitation expected across portions of southeastern Texas and Louisiana. Wetter-than-normal conditions are also possible across parts of the Southeast and eastern Maine.

Meanwhile, drier-than-normal conditions are expected across the Pacific Northwest, Northern Rockies, and portions of the Northern and Central Plains as warmer and more stable weather develops later in the month.

May 8, 2026

Weekly Energy News

Market Update: The U.S. Energy Information Administration reported on May 7, a 63 Bcf injection for the prior week that came in below market expectations.

Following the release of the EIA storage report, the NYMEX June natural gas futures contract climbed nearly 10 cents over the next hour, reaching an intraday high of $2.80/MMBtu as traders reacted to the tighter-than-expected build, according to CME Group data.

The reported injection was 7 Bcf, or roughly 10%, below the consensus estimate from the Platts gas storage survey, which had projected a 70-Bcf increase in inventories for the week ending May 1.

After hitting the upper $2.80s/MMBtu, the prompt-month June contract had pulled back in recent sessions, falling as low as $2.67/MMBtu in the hour leading up to the EIA report.

Despite the post-report rally, analysts noted that prices may face renewed downward pressure amid relatively loose market fundamentals.

“Natural gas market fundamentals remain soft, with storage 153 Bcf above five-year norms, LNG demand down 2.5 Bcf/d from April highs, and production recovering,” said Eli Rubin, senior energy analyst at EBW Analytics, in a May 7 market note.

Rubin also noted that weather-related demand could weaken further as late-season heating needs fade, with a projected 50-gHDD decline in heating demand from Week 1 to Week 3 potentially reopening the door for triple-digit weekly storage injections.

Looking ahead, most analysts expect the EIA’s first storage report for May to show a slightly larger build, likely in the low-70 Bcf range.

June 2026 NYMEX closed Thursday at $2.769

· High for the day $2.813

· Low for the day $2.676

Early trading for the prompt month is trading at $2.785

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: According to EIA estimates, working gas in storage totaled 2,205 Bcf as of Friday, May 1, 2026, reflecting a net injection of 63 Bcf from the prior week. Storage levels were 75 Bcf above the same time last year and 139 Bcf higher than the five-year average of 2,066 Bcf. Total working gas inventories remain within the historical five-year range.

Weather: The updated May outlook calls for a highly variable weather pattern across the U.S. as forecasters monitor shifting atmospheric conditions, the Madden-Julian Oscillation (MJO), and the potential development of El Niño later this summer.

After an unusually warm start to spring, a major pattern shift has brought cooler-than-normal temperatures to the eastern half of the country. Several cold fronts are expected to keep temperatures below normal across parts of the Great Plains, Great Lakes, and Northeast through early May.

By mid-month, forecast models indicate warmer conditions returning as upper-level ridging expands across much of the U.S. This transition is expected to push temperatures above normal across much of the central and western U.S., with the strongest warmth focused in the Pacific Northwest. Due to the expected swings between cooler and warmer periods, much of the eastern U.S. is forecast to see near-normal temperatures overall for the month.

On the precipitation side, above-normal rainfall is favored from Texas through the Gulf Coast and Lower Mississippi Valley during the first half of May, with the heaviest precipitation expected across portions of southeastern Texas and Louisiana. Wetter-than-normal conditions are also possible across parts of the Southeast and eastern Maine.

Meanwhile, drier-than-normal conditions are expected across the Pacific Northwest, Northern Rockies, and portions of the Northern and Central Plains as warmer and more stable weather develops later in the month.

May 8, 2026

Weekly Energy News

Market Update: The U.S. Energy Information Administration reported on May 7, a 63 Bcf injection for the prior week that came in below market expectations.

Following the release of the EIA storage report, the NYMEX June natural gas futures contract climbed nearly 10 cents over the next hour, reaching an intraday high of $2.80/MMBtu as traders reacted to the tighter-than-expected build, according to CME Group data.

The reported injection was 7 Bcf, or roughly 10%, below the consensus estimate from the Platts gas storage survey, which had projected a 70-Bcf increase in inventories for the week ending May 1.

After hitting the upper $2.80s/MMBtu, the prompt-month June contract had pulled back in recent sessions, falling as low as $2.67/MMBtu in the hour leading up to the EIA report.

Despite the post-report rally, analysts noted that prices may face renewed downward pressure amid relatively loose market fundamentals.

“Natural gas market fundamentals remain soft, with storage 153 Bcf above five-year norms, LNG demand down 2.5 Bcf/d from April highs, and production recovering,” said Eli Rubin, senior energy analyst at EBW Analytics, in a May 7 market note.

Rubin also noted that weather-related demand could weaken further as late-season heating needs fade, with a projected 50-gHDD decline in heating demand from Week 1 to Week 3 potentially reopening the door for triple-digit weekly storage injections.

Looking ahead, most analysts expect the EIA’s first storage report for May to show a slightly larger build, likely in the low-70 Bcf range.

June 2026 NYMEX closed Thursday at $2.769

· High for the day $2.813

· Low for the day $2.676

Early trading for the prompt month is trading at $2.785

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: According to EIA estimates, working gas in storage totaled 2,205 Bcf as of Friday, May 1, 2026, reflecting a net injection of 63 Bcf from the prior week. Storage levels were 75 Bcf above the same time last year and 139 Bcf higher than the five-year average of 2,066 Bcf. Total working gas inventories remain within the historical five-year range.

Weather: The updated May outlook calls for a highly variable weather pattern across the U.S. as forecasters monitor shifting atmospheric conditions, the Madden-Julian Oscillation (MJO), and the potential development of El Niño later this summer.

After an unusually warm start to spring, a major pattern shift has brought cooler-than-normal temperatures to the eastern half of the country. Several cold fronts are expected to keep temperatures below normal across parts of the Great Plains, Great Lakes, and Northeast through early May.

By mid-month, forecast models indicate warmer conditions returning as upper-level ridging expands across much of the U.S. This transition is expected to push temperatures above normal across much of the central and western U.S., with the strongest warmth focused in the Pacific Northwest. Due to the expected swings between cooler and warmer periods, much of the eastern U.S. is forecast to see near-normal temperatures overall for the month.

On the precipitation side, above-normal rainfall is favored from Texas through the Gulf Coast and Lower Mississippi Valley during the first half of May, with the heaviest precipitation expected across portions of southeastern Texas and Louisiana. Wetter-than-normal conditions are also possible across parts of the Southeast and eastern Maine.

Meanwhile, drier-than-normal conditions are expected across the Pacific Northwest, Northern Rockies, and portions of the Northern and Central Plains as warmer and more stable weather develops later in the month.

May 8, 2026

Market Update: The U.S. Energy Information Administration reported on May 7, a 63 Bcf injection for the prior week that came in below market expectations.

Following the release of the EIA storage report, the NYMEX June natural gas futures contract climbed nearly 10 cents over the next hour, reaching an intraday high of $2.80/MMBtu as traders reacted to the tighter-than-expected build, according to CME Group data.

The reported injection was 7 Bcf, or roughly 10%, below the consensus estimate from the Platts gas storage survey, which had projected a 70-Bcf increase in inventories for the week ending May 1.

After hitting the upper $2.80s/MMBtu, the prompt-month June contract had pulled back in recent sessions, falling as low as $2.67/MMBtu in the hour leading up to the EIA report.

Despite the post-report rally, analysts noted that prices may face renewed downward pressure amid relatively loose market fundamentals.

“Natural gas market fundamentals remain soft, with storage 153 Bcf above five-year norms, LNG demand down 2.5 Bcf/d from April highs, and production recovering,” said Eli Rubin, senior energy analyst at EBW Analytics, in a May 7 market note.

Rubin also noted that weather-related demand could weaken further as late-season heating needs fade, with a projected 50-gHDD decline in heating demand from Week 1 to Week 3 potentially reopening the door for triple-digit weekly storage injections.

Looking ahead, most analysts expect the EIA’s first storage report for May to show a slightly larger build, likely in the low-70 Bcf range.

June 2026 NYMEX closed Thursday at $2.769

· High for the day $2.813

· Low for the day $2.676

Early trading for the prompt month is trading at $2.785

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: According to EIA estimates, working gas in storage totaled 2,205 Bcf as of Friday, May 1, 2026, reflecting a net injection of 63 Bcf from the prior week. Storage levels were 75 Bcf above the same time last year and 139 Bcf higher than the five-year average of 2,066 Bcf. Total working gas inventories remain within the historical five-year range.

Weather: The updated May outlook calls for a highly variable weather pattern across the U.S. as forecasters monitor shifting atmospheric conditions, the Madden-Julian Oscillation (MJO), and the potential development of El Niño later this summer.

After an unusually warm start to spring, a major pattern shift has brought cooler-than-normal temperatures to the eastern half of the country. Several cold fronts are expected to keep temperatures below normal across parts of the Great Plains, Great Lakes, and Northeast through early May.

By mid-month, forecast models indicate warmer conditions returning as upper-level ridging expands across much of the U.S. This transition is expected to push temperatures above normal across much of the central and western U.S., with the strongest warmth focused in the Pacific Northwest. Due to the expected swings between cooler and warmer periods, much of the eastern U.S. is forecast to see near-normal temperatures overall for the month.

On the precipitation side, above-normal rainfall is favored from Texas through the Gulf Coast and Lower Mississippi Valley during the first half of May, with the heaviest precipitation expected across portions of southeastern Texas and Louisiana. Wetter-than-normal conditions are also possible across parts of the Southeast and eastern Maine.

Meanwhile, drier-than-normal conditions are expected across the Pacific Northwest, Northern Rockies, and portions of the Northern and Central Plains as warmer and more stable weather develops later in the month.

May 8, 2026

Weekly Energy News

Market Update: The U.S. Energy Information Administration reported on May 7, a 63 Bcf injection for the prior week that came in below market expectations.

Following the release of the EIA storage report, the NYMEX June natural gas futures contract climbed nearly 10 cents over the next hour, reaching an intraday high of $2.80/MMBtu as traders reacted to the tighter-than-expected build, according to CME Group data.

The reported injection was 7 Bcf, or roughly 10%, below the consensus estimate from the Platts gas storage survey, which had projected a 70-Bcf increase in inventories for the week ending May 1.

After hitting the upper $2.80s/MMBtu, the prompt-month June contract had pulled back in recent sessions, falling as low as $2.67/MMBtu in the hour leading up to the EIA report.

Despite the post-report rally, analysts noted that prices may face renewed downward pressure amid relatively loose market fundamentals.

“Natural gas market fundamentals remain soft, with storage 153 Bcf above five-year norms, LNG demand down 2.5 Bcf/d from April highs, and production recovering,” said Eli Rubin, senior energy analyst at EBW Analytics, in a May 7 market note.

Rubin also noted that weather-related demand could weaken further as late-season heating needs fade, with a projected 50-gHDD decline in heating demand from Week 1 to Week 3 potentially reopening the door for triple-digit weekly storage injections.

Looking ahead, most analysts expect the EIA’s first storage report for May to show a slightly larger build, likely in the low-70 Bcf range.

June 2026 NYMEX closed Thursday at $2.769

· High for the day $2.813

· Low for the day $2.676

Early trading for the prompt month is trading at $2.785

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: According to EIA estimates, working gas in storage totaled 2,205 Bcf as of Friday, May 1, 2026, reflecting a net injection of 63 Bcf from the prior week. Storage levels were 75 Bcf above the same time last year and 139 Bcf higher than the five-year average of 2,066 Bcf. Total working gas inventories remain within the historical five-year range.

Weather: The updated May outlook calls for a highly variable weather pattern across the U.S. as forecasters monitor shifting atmospheric conditions, the Madden-Julian Oscillation (MJO), and the potential development of El Niño later this summer.

After an unusually warm start to spring, a major pattern shift has brought cooler-than-normal temperatures to the eastern half of the country. Several cold fronts are expected to keep temperatures below normal across parts of the Great Plains, Great Lakes, and Northeast through early May.

By mid-month, forecast models indicate warmer conditions returning as upper-level ridging expands across much of the U.S. This transition is expected to push temperatures above normal across much of the central and western U.S., with the strongest warmth focused in the Pacific Northwest. Due to the expected swings between cooler and warmer periods, much of the eastern U.S. is forecast to see near-normal temperatures overall for the month.

On the precipitation side, above-normal rainfall is favored from Texas through the Gulf Coast and Lower Mississippi Valley during the first half of May, with the heaviest precipitation expected across portions of southeastern Texas and Louisiana. Wetter-than-normal conditions are also possible across parts of the Southeast and eastern Maine.

Meanwhile, drier-than-normal conditions are expected across the Pacific Northwest, Northern Rockies, and portions of the Northern and Central Plains as warmer and more stable weather develops later in the month.

May 8, 2026

Weekly Energy News

Market Update: The U.S. Energy Information Administration reported on May 7, a 63 Bcf injection for the prior week that came in below market expectations.

Following the release of the EIA storage report, the NYMEX June natural gas futures contract climbed nearly 10 cents over the next hour, reaching an intraday high of $2.80/MMBtu as traders reacted to the tighter-than-expected build, according to CME Group data.

The reported injection was 7 Bcf, or roughly 10%, below the consensus estimate from the Platts gas storage survey, which had projected a 70-Bcf increase in inventories for the week ending May 1.

After hitting the upper $2.80s/MMBtu, the prompt-month June contract had pulled back in recent sessions, falling as low as $2.67/MMBtu in the hour leading up to the EIA report.

Despite the post-report rally, analysts noted that prices may face renewed downward pressure amid relatively loose market fundamentals.

“Natural gas market fundamentals remain soft, with storage 153 Bcf above five-year norms, LNG demand down 2.5 Bcf/d from April highs, and production recovering,” said Eli Rubin, senior energy analyst at EBW Analytics, in a May 7 market note.

Rubin also noted that weather-related demand could weaken further as late-season heating needs fade, with a projected 50-gHDD decline in heating demand from Week 1 to Week 3 potentially reopening the door for triple-digit weekly storage injections.

Looking ahead, most analysts expect the EIA’s first storage report for May to show a slightly larger build, likely in the low-70 Bcf range.

June 2026 NYMEX closed Thursday at $2.769

· High for the day $2.813

· Low for the day $2.676

Early trading for the prompt month is trading at $2.785

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: According to EIA estimates, working gas in storage totaled 2,205 Bcf as of Friday, May 1, 2026, reflecting a net injection of 63 Bcf from the prior week. Storage levels were 75 Bcf above the same time last year and 139 Bcf higher than the five-year average of 2,066 Bcf. Total working gas inventories remain within the historical five-year range.

Weather: The updated May outlook calls for a highly variable weather pattern across the U.S. as forecasters monitor shifting atmospheric conditions, the Madden-Julian Oscillation (MJO), and the potential development of El Niño later this summer.

After an unusually warm start to spring, a major pattern shift has brought cooler-than-normal temperatures to the eastern half of the country. Several cold fronts are expected to keep temperatures below normal across parts of the Great Plains, Great Lakes, and Northeast through early May.

By mid-month, forecast models indicate warmer conditions returning as upper-level ridging expands across much of the U.S. This transition is expected to push temperatures above normal across much of the central and western U.S., with the strongest warmth focused in the Pacific Northwest. Due to the expected swings between cooler and warmer periods, much of the eastern U.S. is forecast to see near-normal temperatures overall for the month.

On the precipitation side, above-normal rainfall is favored from Texas through the Gulf Coast and Lower Mississippi Valley during the first half of May, with the heaviest precipitation expected across portions of southeastern Texas and Louisiana. Wetter-than-normal conditions are also possible across parts of the Southeast and eastern Maine.

Meanwhile, drier-than-normal conditions are expected across the Pacific Northwest, Northern Rockies, and portions of the Northern and Central Plains as warmer and more stable weather develops later in the month.

Make Your Choice Gas Selection in Three Easy Steps

Click here to access our online tool, or call our Choice gas commodity experts at 1 (877) 790-4990.

Step 1: Enter your account number

- Your Black Hills Energy account number is located at the top right-hand corner of your bill.

Step 2: Review price options and make your selection

Step 3: Confirm your selection and enter your control number

- You received a control number in your 2026 Choice Gas selection packet mailed to you from Black Hills Energy. If you cannot locate this, you can retrieve your control number by calling 877-245-3506 or visit choicegas.com

Once enrolled, you will be removed from supplier marketing communications within 24 hours.

Sign Up for Our Energy Newsletters

Sign UpRecent Posts