May 15, 2026

Weekly Energy News

Market Update: NYMEX natural gas futures rebounded on May 14 following a weekly storage injection that came in slightly below expectations, near the five-year average, and significantly lower than the same period in 2025.

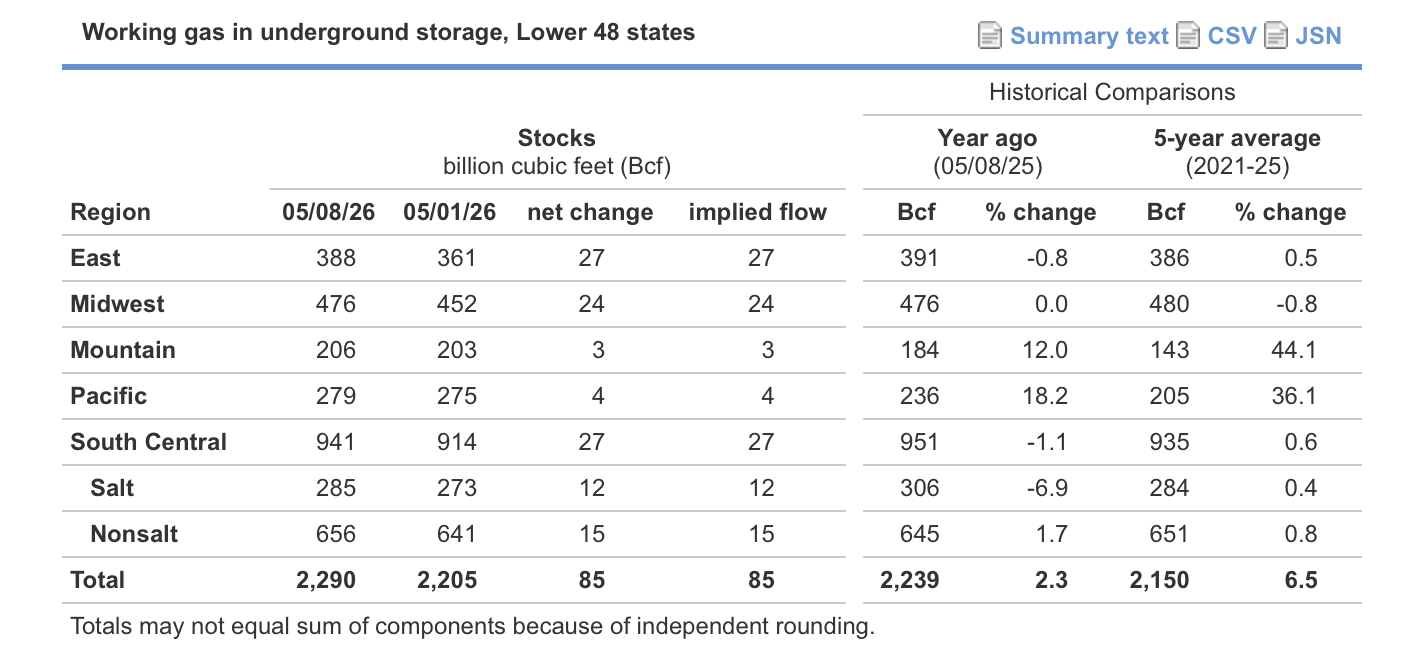

According to the US Energy Information Administration (EIA), natural gas inventories increased by 85 billion cubic feet (Bcf) for the week ending May 8. The injection was just under the 86 Bcf consensus estimate from the May 12 Platts survey, part of S&P Global Energy.

The reported build was slightly above the five-year average injection of 84 Bcf, but remained supportive for prices compared to the 109 Bcf injection recorded during the same week last year. As a result, the storage deficit versus the five-year average widened to 140 Bcf, or 6.5%, while the surplus compared to 2025 inventories narrowed to 51 Bcf, or 2.3%. Last year, inventories were bolstered by a seven-week stretch of triple-digit injections from late April through early June.

Market fundamentals loosened by roughly 3 Bcf/d during the week ending May 8, following a 63 Bcf injection the prior week. Gas demand from the power sector declined by 2.1 Bcf/d as cooler temperatures spread across Texas and the Southeast. LNG feedgas demand also fell by 1.3 Bcf/d due to seasonal maintenance activity, according to CERA data. Although dry gas production increased by 900 MMcf/d, that gain was more than offset by a 1.3 Bcf/d drop in net Canadian imports.

In the current storage week, the market has loosened by an additional 1.6 Bcf/d, according to CERA data. Warmer weather led to a 3.2 Bcf/d decline in residential and commercial demand, which outweighed a 1.9 Bcf/d increase in power-sector demand. LNG feedgas demand also slipped by 400 MMcf/d to average 17.9 Bcf/d, its lowest level since January.

The recent decline in demand could allow the storage surplus versus the five-year average to expand further. S&P Global Energy’s CERA supply-demand and daily storage models are projecting injections between 93 Bcf and 102 Bcf for the week ending May 15. While that would exceed the five-year average injection of 92 Bcf, it would still trail last year’s 119 Bcf build for the same week.

June 2026 NYMEX closed Thursday at $2.894

· High for the day $2.922

· Low for the day $2.798

Early trading for the prompt month is trading at $2.925

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

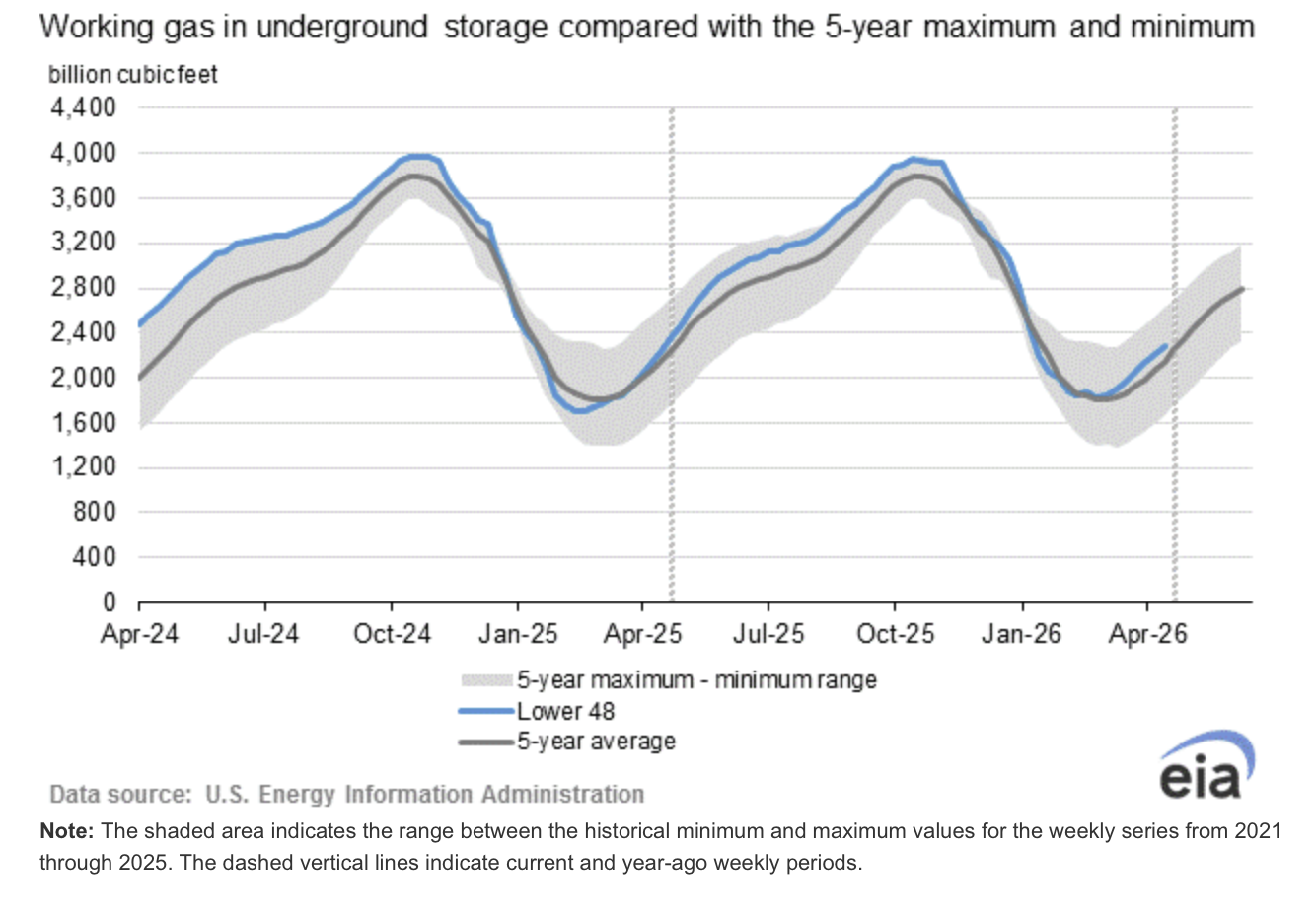

EIA Storage Report: Working gas inventories totaled 2,290 Bcf as of Friday, May 8, 2026, according to estimates from the EIA. That marks an increase of 85 Bcf from the prior week. Storage levels were 51 Bcf above year-ago levels and 140 Bcf higher than the five-year average of 2,150 Bcf. Overall, working gas inventories remain within the historical five-year range.

Weather: The latest NOAA outlook points to warmer-than-normal temperatures across much of the United States through the end of May, especially along the East Coast and in Florida. The West Coast is also expected to see warmer conditions, while the central part of the country, including portions of Texas and the Plains, may experience temperatures closer to seasonal averages due to increased cloud cover and unsettled weather patterns.

NOAA is also forecasting above-normal rainfall across much of the central and eastern U.S. over the next two weeks. Texas, Oklahoma, and parts of New Mexico could see the greatest chances for heavier precipitation, while the northern West Coast is expected to remain drier than normal.

Looking further into late May, warmer weather is expected to expand across most of the country, increasing cooling demand as air conditioners begin running more consistently heading into summer. Wetter conditions are still favored across much of the South and eastern U.S., particularly in Texas and the Southeast.

Market Data:

May 15, 2026

Weekly Energy News

May 15, 2026

Market Update: NYMEX natural gas futures rebounded on May 14 following a weekly storage injection that came in slightly below expectations, near the five-year average, and significantly lower than the same period in 2025.

According to the US Energy Information Administration (EIA), natural gas inventories increased by 85 billion cubic feet (Bcf) for the week ending May 8. The injection was just under the 86 Bcf consensus estimate from the May 12 Platts survey, part of S&P Global Energy.

The reported build was slightly above the five-year average injection of 84 Bcf, but remained supportive for prices compared to the 109 Bcf injection recorded during the same week last year. As a result, the storage deficit versus the five-year average widened to 140 Bcf, or 6.5%, while the surplus compared to 2025 inventories narrowed to 51 Bcf, or 2.3%. Last year, inventories were bolstered by a seven-week stretch of triple-digit injections from late April through early June.

Market fundamentals loosened by roughly 3 Bcf/d during the week ending May 8, following a 63 Bcf injection the prior week. Gas demand from the power sector declined by 2.1 Bcf/d as cooler temperatures spread across Texas and the Southeast. LNG feedgas demand also fell by 1.3 Bcf/d due to seasonal maintenance activity, according to CERA data. Although dry gas production increased by 900 MMcf/d, that gain was more than offset by a 1.3 Bcf/d drop in net Canadian imports.

In the current storage week, the market has loosened by an additional 1.6 Bcf/d, according to CERA data. Warmer weather led to a 3.2 Bcf/d decline in residential and commercial demand, which outweighed a 1.9 Bcf/d increase in power-sector demand. LNG feedgas demand also slipped by 400 MMcf/d to average 17.9 Bcf/d, its lowest level since January.

The recent decline in demand could allow the storage surplus versus the five-year average to expand further. S&P Global Energy’s CERA supply-demand and daily storage models are projecting injections between 93 Bcf and 102 Bcf for the week ending May 15. While that would exceed the five-year average injection of 92 Bcf, it would still trail last year’s 119 Bcf build for the same week.

June 2026 NYMEX closed Thursday at $2.894

· High for the day $2.922

· Low for the day $2.798

Early trading for the prompt month is trading at $2.925

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: Working gas inventories totaled 2,290 Bcf as of Friday, May 8, 2026, according to estimates from the EIA. That marks an increase of 85 Bcf from the prior week. Storage levels were 51 Bcf above year-ago levels and 140 Bcf higher than the five-year average of 2,150 Bcf. Overall, working gas inventories remain within the historical five-year range.

Weather: The latest NOAA outlook points to warmer-than-normal temperatures across much of the United States through the end of May, especially along the East Coast and in Florida. The West Coast is also expected to see warmer conditions, while the central part of the country, including portions of Texas and the Plains, may experience temperatures closer to seasonal averages due to increased cloud cover and unsettled weather patterns.

NOAA is also forecasting above-normal rainfall across much of the central and eastern U.S. over the next two weeks. Texas, Oklahoma, and parts of New Mexico could see the greatest chances for heavier precipitation, while the northern West Coast is expected to remain drier than normal.

Looking further into late May, warmer weather is expected to expand across most of the country, increasing cooling demand as air conditioners begin running more consistently heading into summer. Wetter conditions are still favored across much of the South and eastern U.S., particularly in Texas and the Southeast.

Market Data:

May 15, 2026

May 15, 2026

Weekly Energy News

Market Update: NYMEX natural gas futures rebounded on May 14 following a weekly storage injection that came in slightly below expectations, near the five-year average, and significantly lower than the same period in 2025.

According to the US Energy Information Administration (EIA), natural gas inventories increased by 85 billion cubic feet (Bcf) for the week ending May 8. The injection was just under the 86 Bcf consensus estimate from the May 12 Platts survey, part of S&P Global Energy.

The reported build was slightly above the five-year average injection of 84 Bcf, but remained supportive for prices compared to the 109 Bcf injection recorded during the same week last year. As a result, the storage deficit versus the five-year average widened to 140 Bcf, or 6.5%, while the surplus compared to 2025 inventories narrowed to 51 Bcf, or 2.3%. Last year, inventories were bolstered by a seven-week stretch of triple-digit injections from late April through early June.

Market fundamentals loosened by roughly 3 Bcf/d during the week ending May 8, following a 63 Bcf injection the prior week. Gas demand from the power sector declined by 2.1 Bcf/d as cooler temperatures spread across Texas and the Southeast. LNG feedgas demand also fell by 1.3 Bcf/d due to seasonal maintenance activity, according to CERA data. Although dry gas production increased by 900 MMcf/d, that gain was more than offset by a 1.3 Bcf/d drop in net Canadian imports.

In the current storage week, the market has loosened by an additional 1.6 Bcf/d, according to CERA data. Warmer weather led to a 3.2 Bcf/d decline in residential and commercial demand, which outweighed a 1.9 Bcf/d increase in power-sector demand. LNG feedgas demand also slipped by 400 MMcf/d to average 17.9 Bcf/d, its lowest level since January.

The recent decline in demand could allow the storage surplus versus the five-year average to expand further. S&P Global Energy’s CERA supply-demand and daily storage models are projecting injections between 93 Bcf and 102 Bcf for the week ending May 15. While that would exceed the five-year average injection of 92 Bcf, it would still trail last year’s 119 Bcf build for the same week.

June 2026 NYMEX closed Thursday at $2.894

· High for the day $2.922

· Low for the day $2.798

Early trading for the prompt month is trading at $2.925

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: Working gas inventories totaled 2,290 Bcf as of Friday, May 8, 2026, according to estimates from the EIA. That marks an increase of 85 Bcf from the prior week. Storage levels were 51 Bcf above year-ago levels and 140 Bcf higher than the five-year average of 2,150 Bcf. Overall, working gas inventories remain within the historical five-year range.

Weather: The latest NOAA outlook points to warmer-than-normal temperatures across much of the United States through the end of May, especially along the East Coast and in Florida. The West Coast is also expected to see warmer conditions, while the central part of the country, including portions of Texas and the Plains, may experience temperatures closer to seasonal averages due to increased cloud cover and unsettled weather patterns.

NOAA is also forecasting above-normal rainfall across much of the central and eastern U.S. over the next two weeks. Texas, Oklahoma, and parts of New Mexico could see the greatest chances for heavier precipitation, while the northern West Coast is expected to remain drier than normal.

Looking further into late May, warmer weather is expected to expand across most of the country, increasing cooling demand as air conditioners begin running more consistently heading into summer. Wetter conditions are still favored across much of the South and eastern U.S., particularly in Texas and the Southeast.

May 15, 2026

Weekly Energy News

Market Update: NYMEX natural gas futures rebounded on May 14 following a weekly storage injection that came in slightly below expectations, near the five-year average, and significantly lower than the same period in 2025.

According to the US Energy Information Administration (EIA), natural gas inventories increased by 85 billion cubic feet (Bcf) for the week ending May 8. The injection was just under the 86 Bcf consensus estimate from the May 12 Platts survey, part of S&P Global Energy.

The reported build was slightly above the five-year average injection of 84 Bcf, but remained supportive for prices compared to the 109 Bcf injection recorded during the same week last year. As a result, the storage deficit versus the five-year average widened to 140 Bcf, or 6.5%, while the surplus compared to 2025 inventories narrowed to 51 Bcf, or 2.3%. Last year, inventories were bolstered by a seven-week stretch of triple-digit injections from late April through early June.

Market fundamentals loosened by roughly 3 Bcf/d during the week ending May 8, following a 63 Bcf injection the prior week. Gas demand from the power sector declined by 2.1 Bcf/d as cooler temperatures spread across Texas and the Southeast. LNG feedgas demand also fell by 1.3 Bcf/d due to seasonal maintenance activity, according to CERA data. Although dry gas production increased by 900 MMcf/d, that gain was more than offset by a 1.3 Bcf/d drop in net Canadian imports.

In the current storage week, the market has loosened by an additional 1.6 Bcf/d, according to CERA data. Warmer weather led to a 3.2 Bcf/d decline in residential and commercial demand, which outweighed a 1.9 Bcf/d increase in power-sector demand. LNG feedgas demand also slipped by 400 MMcf/d to average 17.9 Bcf/d, its lowest level since January.

The recent decline in demand could allow the storage surplus versus the five-year average to expand further. S&P Global Energy’s CERA supply-demand and daily storage models are projecting injections between 93 Bcf and 102 Bcf for the week ending May 15. While that would exceed the five-year average injection of 92 Bcf, it would still trail last year’s 119 Bcf build for the same week.

June 2026 NYMEX closed Thursday at $2.894

· High for the day $2.922

· Low for the day $2.798

Early trading for the prompt month is trading at $2.925

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: Working gas inventories totaled 2,290 Bcf as of Friday, May 8, 2026, according to estimates from the EIA. That marks an increase of 85 Bcf from the prior week. Storage levels were 51 Bcf above year-ago levels and 140 Bcf higher than the five-year average of 2,150 Bcf. Overall, working gas inventories remain within the historical five-year range.

Weather: The latest NOAA outlook points to warmer-than-normal temperatures across much of the United States through the end of May, especially along the East Coast and in Florida. The West Coast is also expected to see warmer conditions, while the central part of the country, including portions of Texas and the Plains, may experience temperatures closer to seasonal averages due to increased cloud cover and unsettled weather patterns.

NOAA is also forecasting above-normal rainfall across much of the central and eastern U.S. over the next two weeks. Texas, Oklahoma, and parts of New Mexico could see the greatest chances for heavier precipitation, while the northern West Coast is expected to remain drier than normal.

Looking further into late May, warmer weather is expected to expand across most of the country, increasing cooling demand as air conditioners begin running more consistently heading into summer. Wetter conditions are still favored across much of the South and eastern U.S., particularly in Texas and the Southeast.

May 15, 2026

Weekly Energy News

Market Update: NYMEX natural gas futures rebounded on May 14 following a weekly storage injection that came in slightly below expectations, near the five-year average, and significantly lower than the same period in 2025.

According to the US Energy Information Administration (EIA), natural gas inventories increased by 85 billion cubic feet (Bcf) for the week ending May 8. The injection was just under the 86 Bcf consensus estimate from the May 12 Platts survey, part of S&P Global Energy.

The reported build was slightly above the five-year average injection of 84 Bcf, but remained supportive for prices compared to the 109 Bcf injection recorded during the same week last year. As a result, the storage deficit versus the five-year average widened to 140 Bcf, or 6.5%, while the surplus compared to 2025 inventories narrowed to 51 Bcf, or 2.3%. Last year, inventories were bolstered by a seven-week stretch of triple-digit injections from late April through early June.

Market fundamentals loosened by roughly 3 Bcf/d during the week ending May 8, following a 63 Bcf injection the prior week. Gas demand from the power sector declined by 2.1 Bcf/d as cooler temperatures spread across Texas and the Southeast. LNG feedgas demand also fell by 1.3 Bcf/d due to seasonal maintenance activity, according to CERA data. Although dry gas production increased by 900 MMcf/d, that gain was more than offset by a 1.3 Bcf/d drop in net Canadian imports.

In the current storage week, the market has loosened by an additional 1.6 Bcf/d, according to CERA data. Warmer weather led to a 3.2 Bcf/d decline in residential and commercial demand, which outweighed a 1.9 Bcf/d increase in power-sector demand. LNG feedgas demand also slipped by 400 MMcf/d to average 17.9 Bcf/d, its lowest level since January.

The recent decline in demand could allow the storage surplus versus the five-year average to expand further. S&P Global Energy’s CERA supply-demand and daily storage models are projecting injections between 93 Bcf and 102 Bcf for the week ending May 15. While that would exceed the five-year average injection of 92 Bcf, it would still trail last year’s 119 Bcf build for the same week.

June 2026 NYMEX closed Thursday at $2.894

· High for the day $2.922

· Low for the day $2.798

Early trading for the prompt month is trading at $2.925

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: Working gas inventories totaled 2,290 Bcf as of Friday, May 8, 2026, according to estimates from the EIA. That marks an increase of 85 Bcf from the prior week. Storage levels were 51 Bcf above year-ago levels and 140 Bcf higher than the five-year average of 2,150 Bcf. Overall, working gas inventories remain within the historical five-year range.

Weather: The latest NOAA outlook points to warmer-than-normal temperatures across much of the United States through the end of May, especially along the East Coast and in Florida. The West Coast is also expected to see warmer conditions, while the central part of the country, including portions of Texas and the Plains, may experience temperatures closer to seasonal averages due to increased cloud cover and unsettled weather patterns.

NOAA is also forecasting above-normal rainfall across much of the central and eastern U.S. over the next two weeks. Texas, Oklahoma, and parts of New Mexico could see the greatest chances for heavier precipitation, while the northern West Coast is expected to remain drier than normal.

Looking further into late May, warmer weather is expected to expand across most of the country, increasing cooling demand as air conditioners begin running more consistently heading into summer. Wetter conditions are still favored across much of the South and eastern U.S., particularly in Texas and the Southeast.

May 15, 2026

Market Update: NYMEX natural gas futures rebounded on May 14 following a weekly storage injection that came in slightly below expectations, near the five-year average, and significantly lower than the same period in 2025.

According to the US Energy Information Administration (EIA), natural gas inventories increased by 85 billion cubic feet (Bcf) for the week ending May 8. The injection was just under the 86 Bcf consensus estimate from the May 12 Platts survey, part of S&P Global Energy.

The reported build was slightly above the five-year average injection of 84 Bcf, but remained supportive for prices compared to the 109 Bcf injection recorded during the same week last year. As a result, the storage deficit versus the five-year average widened to 140 Bcf, or 6.5%, while the surplus compared to 2025 inventories narrowed to 51 Bcf, or 2.3%. Last year, inventories were bolstered by a seven-week stretch of triple-digit injections from late April through early June.

Market fundamentals loosened by roughly 3 Bcf/d during the week ending May 8, following a 63 Bcf injection the prior week. Gas demand from the power sector declined by 2.1 Bcf/d as cooler temperatures spread across Texas and the Southeast. LNG feedgas demand also fell by 1.3 Bcf/d due to seasonal maintenance activity, according to CERA data. Although dry gas production increased by 900 MMcf/d, that gain was more than offset by a 1.3 Bcf/d drop in net Canadian imports.

In the current storage week, the market has loosened by an additional 1.6 Bcf/d, according to CERA data. Warmer weather led to a 3.2 Bcf/d decline in residential and commercial demand, which outweighed a 1.9 Bcf/d increase in power-sector demand. LNG feedgas demand also slipped by 400 MMcf/d to average 17.9 Bcf/d, its lowest level since January.

The recent decline in demand could allow the storage surplus versus the five-year average to expand further. S&P Global Energy’s CERA supply-demand and daily storage models are projecting injections between 93 Bcf and 102 Bcf for the week ending May 15. While that would exceed the five-year average injection of 92 Bcf, it would still trail last year’s 119 Bcf build for the same week.

June 2026 NYMEX closed Thursday at $2.894

· High for the day $2.922

· Low for the day $2.798

Early trading for the prompt month is trading at $2.925

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: Working gas inventories totaled 2,290 Bcf as of Friday, May 8, 2026, according to estimates from the EIA. That marks an increase of 85 Bcf from the prior week. Storage levels were 51 Bcf above year-ago levels and 140 Bcf higher than the five-year average of 2,150 Bcf. Overall, working gas inventories remain within the historical five-year range.

Weather: The latest NOAA outlook points to warmer-than-normal temperatures across much of the United States through the end of May, especially along the East Coast and in Florida. The West Coast is also expected to see warmer conditions, while the central part of the country, including portions of Texas and the Plains, may experience temperatures closer to seasonal averages due to increased cloud cover and unsettled weather patterns.

NOAA is also forecasting above-normal rainfall across much of the central and eastern U.S. over the next two weeks. Texas, Oklahoma, and parts of New Mexico could see the greatest chances for heavier precipitation, while the northern West Coast is expected to remain drier than normal.

Looking further into late May, warmer weather is expected to expand across most of the country, increasing cooling demand as air conditioners begin running more consistently heading into summer. Wetter conditions are still favored across much of the South and eastern U.S., particularly in Texas and the Southeast.

May 15, 2026

Weekly Energy News

Market Update: NYMEX natural gas futures rebounded on May 14 following a weekly storage injection that came in slightly below expectations, near the five-year average, and significantly lower than the same period in 2025.

According to the US Energy Information Administration (EIA), natural gas inventories increased by 85 billion cubic feet (Bcf) for the week ending May 8. The injection was just under the 86 Bcf consensus estimate from the May 12 Platts survey, part of S&P Global Energy.

The reported build was slightly above the five-year average injection of 84 Bcf, but remained supportive for prices compared to the 109 Bcf injection recorded during the same week last year. As a result, the storage deficit versus the five-year average widened to 140 Bcf, or 6.5%, while the surplus compared to 2025 inventories narrowed to 51 Bcf, or 2.3%. Last year, inventories were bolstered by a seven-week stretch of triple-digit injections from late April through early June.

Market fundamentals loosened by roughly 3 Bcf/d during the week ending May 8, following a 63 Bcf injection the prior week. Gas demand from the power sector declined by 2.1 Bcf/d as cooler temperatures spread across Texas and the Southeast. LNG feedgas demand also fell by 1.3 Bcf/d due to seasonal maintenance activity, according to CERA data. Although dry gas production increased by 900 MMcf/d, that gain was more than offset by a 1.3 Bcf/d drop in net Canadian imports.

In the current storage week, the market has loosened by an additional 1.6 Bcf/d, according to CERA data. Warmer weather led to a 3.2 Bcf/d decline in residential and commercial demand, which outweighed a 1.9 Bcf/d increase in power-sector demand. LNG feedgas demand also slipped by 400 MMcf/d to average 17.9 Bcf/d, its lowest level since January.

The recent decline in demand could allow the storage surplus versus the five-year average to expand further. S&P Global Energy’s CERA supply-demand and daily storage models are projecting injections between 93 Bcf and 102 Bcf for the week ending May 15. While that would exceed the five-year average injection of 92 Bcf, it would still trail last year’s 119 Bcf build for the same week.

June 2026 NYMEX closed Thursday at $2.894

· High for the day $2.922

· Low for the day $2.798

Early trading for the prompt month is trading at $2.925

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: Working gas inventories totaled 2,290 Bcf as of Friday, May 8, 2026, according to estimates from the EIA. That marks an increase of 85 Bcf from the prior week. Storage levels were 51 Bcf above year-ago levels and 140 Bcf higher than the five-year average of 2,150 Bcf. Overall, working gas inventories remain within the historical five-year range.

Weather: The latest NOAA outlook points to warmer-than-normal temperatures across much of the United States through the end of May, especially along the East Coast and in Florida. The West Coast is also expected to see warmer conditions, while the central part of the country, including portions of Texas and the Plains, may experience temperatures closer to seasonal averages due to increased cloud cover and unsettled weather patterns.

NOAA is also forecasting above-normal rainfall across much of the central and eastern U.S. over the next two weeks. Texas, Oklahoma, and parts of New Mexico could see the greatest chances for heavier precipitation, while the northern West Coast is expected to remain drier than normal.

Looking further into late May, warmer weather is expected to expand across most of the country, increasing cooling demand as air conditioners begin running more consistently heading into summer. Wetter conditions are still favored across much of the South and eastern U.S., particularly in Texas and the Southeast.

May 15, 2026

Weekly Energy News

Market Update: NYMEX natural gas futures rebounded on May 14 following a weekly storage injection that came in slightly below expectations, near the five-year average, and significantly lower than the same period in 2025.

According to the US Energy Information Administration (EIA), natural gas inventories increased by 85 billion cubic feet (Bcf) for the week ending May 8. The injection was just under the 86 Bcf consensus estimate from the May 12 Platts survey, part of S&P Global Energy.

The reported build was slightly above the five-year average injection of 84 Bcf, but remained supportive for prices compared to the 109 Bcf injection recorded during the same week last year. As a result, the storage deficit versus the five-year average widened to 140 Bcf, or 6.5%, while the surplus compared to 2025 inventories narrowed to 51 Bcf, or 2.3%. Last year, inventories were bolstered by a seven-week stretch of triple-digit injections from late April through early June.

Market fundamentals loosened by roughly 3 Bcf/d during the week ending May 8, following a 63 Bcf injection the prior week. Gas demand from the power sector declined by 2.1 Bcf/d as cooler temperatures spread across Texas and the Southeast. LNG feedgas demand also fell by 1.3 Bcf/d due to seasonal maintenance activity, according to CERA data. Although dry gas production increased by 900 MMcf/d, that gain was more than offset by a 1.3 Bcf/d drop in net Canadian imports.

In the current storage week, the market has loosened by an additional 1.6 Bcf/d, according to CERA data. Warmer weather led to a 3.2 Bcf/d decline in residential and commercial demand, which outweighed a 1.9 Bcf/d increase in power-sector demand. LNG feedgas demand also slipped by 400 MMcf/d to average 17.9 Bcf/d, its lowest level since January.

The recent decline in demand could allow the storage surplus versus the five-year average to expand further. S&P Global Energy’s CERA supply-demand and daily storage models are projecting injections between 93 Bcf and 102 Bcf for the week ending May 15. While that would exceed the five-year average injection of 92 Bcf, it would still trail last year’s 119 Bcf build for the same week.

June 2026 NYMEX closed Thursday at $2.894

· High for the day $2.922

· Low for the day $2.798

Early trading for the prompt month is trading at $2.925

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

EIA Storage Report: Working gas inventories totaled 2,290 Bcf as of Friday, May 8, 2026, according to estimates from the EIA. That marks an increase of 85 Bcf from the prior week. Storage levels were 51 Bcf above year-ago levels and 140 Bcf higher than the five-year average of 2,150 Bcf. Overall, working gas inventories remain within the historical five-year range.

Weather: The latest NOAA outlook points to warmer-than-normal temperatures across much of the United States through the end of May, especially along the East Coast and in Florida. The West Coast is also expected to see warmer conditions, while the central part of the country, including portions of Texas and the Plains, may experience temperatures closer to seasonal averages due to increased cloud cover and unsettled weather patterns.

NOAA is also forecasting above-normal rainfall across much of the central and eastern U.S. over the next two weeks. Texas, Oklahoma, and parts of New Mexico could see the greatest chances for heavier precipitation, while the northern West Coast is expected to remain drier than normal.

Looking further into late May, warmer weather is expected to expand across most of the country, increasing cooling demand as air conditioners begin running more consistently heading into summer. Wetter conditions are still favored across much of the South and eastern U.S., particularly in Texas and the Southeast.

Make Your Choice Gas Selection in Three Easy Steps

Click here to access our online tool, or call our Choice gas commodity experts at 1 (877) 790-4990.

Step 1: Enter your account number

- Your Black Hills Energy account number is located at the top right-hand corner of your bill.

Step 2: Review price options and make your selection

Step 3: Confirm your selection and enter your control number

- You received a control number in your 2026 Choice Gas selection packet mailed to you from Black Hills Energy. If you cannot locate this, you can retrieve your control number by calling 877-245-3506 or visit choicegas.com

Once enrolled, you will be removed from supplier marketing communications within 24 hours.

Sign Up for Our Energy Newsletters

Sign Up