March 6, 2026

Weekly Energy News

Market Commentary: Henry Hub cash prices hit a seven‑week low on March 5 as US gas demand fell to its lowest level since mid‑November. Prices briefly dipped to $2.85/MMBtu before settling near $2.89/MMBtu, with warmer temperatures expected to keep spot prices under pressure.

Forward pricing has been stronger. After rolling to March at $2.84/MMBtu, the balance‑of‑month contract climbed above $3/MMBtu. A potential late‑March cool‑down could lift cash prices again before milder April weather returns.

April 2026 NYMEX closed Thursday at $3.003

· High for the day $3.046

· Low for the day $2.920

Early trading for the prompt month is trading at $3.081

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

International Markets: The conflict in Iran has greatly impacted international energy markets. Qatar, the second largest liquified natural gas (LNG) exporter in the world, stopped production of LNG after attacks by Iranian drones. About 20 percent of global LNG exports come from the Persian Gulf and are shipped through the Strait of Hormuz. On Monday, European natural gas futures soared to the highest levels in three years. With the U.S. being the largest LNG exporter in the world, we could see more domestic production allocated to international markets.

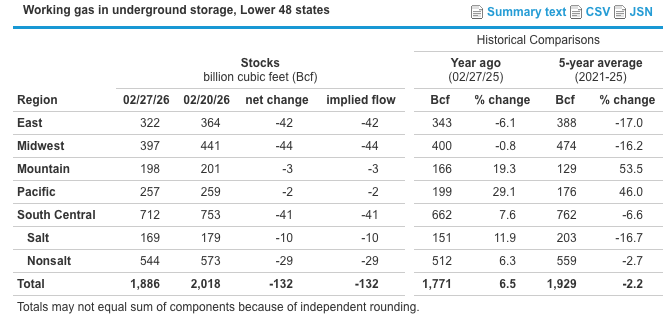

EIA Storage: The US Energy Information Administration reported a 132 Bcf withdrawal from natural gas storage for the week ending Feb. 27—slightly above expectations of 125 Bcf and higher than both the five‑year average pull of 96 Bcf and last year’s 106 Bcf. The storage deficit to the five‑year average widened to 43 Bcf (2.2%), while the surplus to 2025 levels narrowed to 115 Bcf (6.5%).

NYMEX Henry Hub April futures traded between $2.92 and $2.96/MMBtu following the report, later rising to $2.99/MMBtu—up 7 cents from the prior settlement.

Regionally, withdrawals were below average in the Pacific and Mountain regions but above average in the East, Midwest, and South Central, expanding regional imbalances. Stocks remain 53.5% above the five‑year average in the Mountain region and 46% above in the Pacific, while other regions sit well below normal.

These disparities are contributing to steep basis discounts across the Rockies and western markets. On March 4, the Cheyenne Hub April forward contract traded $1.50/MMBtu below Henry Hub, and even California’s typically premium SoCal Gas city‑gate showed a 48‑cent discount.

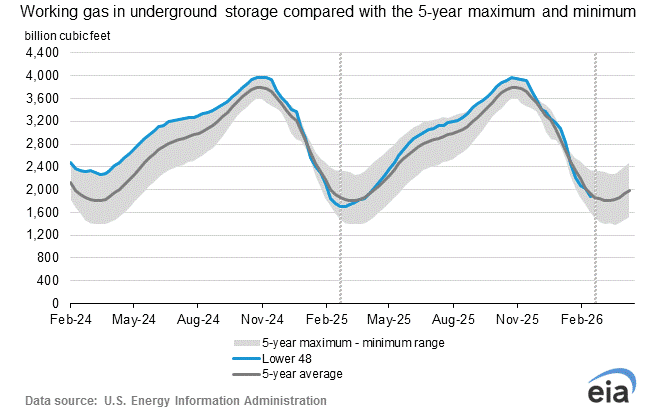

Summary: Working gas in storage totaled 1,886 Bcf as of February 27, 2026, according to EIA estimates. This reflects a 132 Bcf withdrawal from the previous week. Inventories are 115 Bcf above year‑ago levels but 43 Bcf below the five‑year average of 1,929 Bcf. Overall, storage levels remain within the five‑year historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: March is expected to start active and warmer than normal, with severe weather risks increasing as we move into late next week. A brief break in activity may develop around mid‑month.

Severe weather potential is forecast to ramp up during the latter half of next week—especially across southern regions—and expand into the Midwest by next weekend. The upper‑air pattern favors a western trough pushing energy eastward into the Plains, and ample low‑level moisture should support multiple severe weather events.

Snow chances will persist through the first half of March, with enough cold air in place on the northern side of passing systems despite generally above‑average temperatures. However, as the month progresses, accumulating snow will become less likely unless the polar vortex sends a renewed push of Arctic air into the region. Midwest Weather. “March Outlook.” Midwest Weather (Substack), 2026. Subscriber-only newsletter.

Market Data:

March 6, 2026

Weekly Energy News

March 6, 2026

Market Commentary: Henry Hub cash prices hit a seven‑week low on March 5 as US gas demand fell to its lowest level since mid‑November. Prices briefly dipped to $2.85/MMBtu before settling near $2.89/MMBtu, with warmer temperatures expected to keep spot prices under pressure.

Forward pricing has been stronger. After rolling to March at $2.84/MMBtu, the balance‑of‑month contract climbed above $3/MMBtu. A potential late‑March cool‑down could lift cash prices again before milder April weather returns.

April 2026 NYMEX closed Thursday at $3.003

· High for the day $3.046

· Low for the day $2.920

Early trading for the prompt month is trading at $3.081

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

International Markets: The conflict in Iran has greatly impacted international energy markets. Qatar, the second largest liquified natural gas (LNG) exporter in the world, stopped production of LNG after attacks by Iranian drones. About 20 percent of global LNG exports come from the Persian Gulf and are shipped through the Strait of Hormuz. On Monday, European natural gas futures soared to the highest levels in three years. With the U.S. being the largest LNG exporter in the world, we could see more domestic production allocated to international markets.

EIA Storage: The US Energy Information Administration reported a 132 Bcf withdrawal from natural gas storage for the week ending Feb. 27—slightly above expectations of 125 Bcf and higher than both the five‑year average pull of 96 Bcf and last year’s 106 Bcf. The storage deficit to the five‑year average widened to 43 Bcf (2.2%), while the surplus to 2025 levels narrowed to 115 Bcf (6.5%).

NYMEX Henry Hub April futures traded between $2.92 and $2.96/MMBtu following the report, later rising to $2.99/MMBtu—up 7 cents from the prior settlement.

Regionally, withdrawals were below average in the Pacific and Mountain regions but above average in the East, Midwest, and South Central, expanding regional imbalances. Stocks remain 53.5% above the five‑year average in the Mountain region and 46% above in the Pacific, while other regions sit well below normal.

These disparities are contributing to steep basis discounts across the Rockies and western markets. On March 4, the Cheyenne Hub April forward contract traded $1.50/MMBtu below Henry Hub, and even California’s typically premium SoCal Gas city‑gate showed a 48‑cent discount.

Summary: Working gas in storage totaled 1,886 Bcf as of February 27, 2026, according to EIA estimates. This reflects a 132 Bcf withdrawal from the previous week. Inventories are 115 Bcf above year‑ago levels but 43 Bcf below the five‑year average of 1,929 Bcf. Overall, storage levels remain within the five‑year historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: March is expected to start active and warmer than normal, with severe weather risks increasing as we move into late next week. A brief break in activity may develop around mid‑month.

Severe weather potential is forecast to ramp up during the latter half of next week—especially across southern regions—and expand into the Midwest by next weekend. The upper‑air pattern favors a western trough pushing energy eastward into the Plains, and ample low‑level moisture should support multiple severe weather events.

Snow chances will persist through the first half of March, with enough cold air in place on the northern side of passing systems despite generally above‑average temperatures. However, as the month progresses, accumulating snow will become less likely unless the polar vortex sends a renewed push of Arctic air into the region. Midwest Weather. “March Outlook.” Midwest Weather (Substack), 2026. Subscriber-only newsletter.

Market Data:

March 6, 2026

March 6, 2026

Weekly Energy News

Market Commentary: Henry Hub cash prices hit a seven‑week low on March 5 as US gas demand fell to its lowest level since mid‑November. Prices briefly dipped to $2.85/MMBtu before settling near $2.89/MMBtu, with warmer temperatures expected to keep spot prices under pressure.

Forward pricing has been stronger. After rolling to March at $2.84/MMBtu, the balance‑of‑month contract climbed above $3/MMBtu. A potential late‑March cool‑down could lift cash prices again before milder April weather returns.

April 2026 NYMEX closed Thursday at $3.003

· High for the day $3.046

· Low for the day $2.920

Early trading for the prompt month is trading at $3.081

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

International Markets: The conflict in Iran has greatly impacted international energy markets. Qatar, the second largest liquified natural gas (LNG) exporter in the world, stopped production of LNG after attacks by Iranian drones. About 20 percent of global LNG exports come from the Persian Gulf and are shipped through the Strait of Hormuz. On Monday, European natural gas futures soared to the highest levels in three years. With the U.S. being the largest LNG exporter in the world, we could see more domestic production allocated to international markets.

EIA Storage: The US Energy Information Administration reported a 132 Bcf withdrawal from natural gas storage for the week ending Feb. 27—slightly above expectations of 125 Bcf and higher than both the five‑year average pull of 96 Bcf and last year’s 106 Bcf. The storage deficit to the five‑year average widened to 43 Bcf (2.2%), while the surplus to 2025 levels narrowed to 115 Bcf (6.5%).

NYMEX Henry Hub April futures traded between $2.92 and $2.96/MMBtu following the report, later rising to $2.99/MMBtu—up 7 cents from the prior settlement.

Regionally, withdrawals were below average in the Pacific and Mountain regions but above average in the East, Midwest, and South Central, expanding regional imbalances. Stocks remain 53.5% above the five‑year average in the Mountain region and 46% above in the Pacific, while other regions sit well below normal.

These disparities are contributing to steep basis discounts across the Rockies and western markets. On March 4, the Cheyenne Hub April forward contract traded $1.50/MMBtu below Henry Hub, and even California’s typically premium SoCal Gas city‑gate showed a 48‑cent discount.

Summary: Working gas in storage totaled 1,886 Bcf as of February 27, 2026, according to EIA estimates. This reflects a 132 Bcf withdrawal from the previous week. Inventories are 115 Bcf above year‑ago levels but 43 Bcf below the five‑year average of 1,929 Bcf. Overall, storage levels remain within the five‑year historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: March is expected to start active and warmer than normal, with severe weather risks increasing as we move into late next week. A brief break in activity may develop around mid‑month.

Severe weather potential is forecast to ramp up during the latter half of next week—especially across southern regions—and expand into the Midwest by next weekend. The upper‑air pattern favors a western trough pushing energy eastward into the Plains, and ample low‑level moisture should support multiple severe weather events.

Snow chances will persist through the first half of March, with enough cold air in place on the northern side of passing systems despite generally above‑average temperatures. However, as the month progresses, accumulating snow will become less likely unless the polar vortex sends a renewed push of Arctic air into the region. Midwest Weather. “March Outlook.” Midwest Weather (Substack), 2026. Subscriber-only newsletter.

March 6, 2026

Weekly Energy News

Market Commentary: Henry Hub cash prices hit a seven‑week low on March 5 as US gas demand fell to its lowest level since mid‑November. Prices briefly dipped to $2.85/MMBtu before settling near $2.89/MMBtu, with warmer temperatures expected to keep spot prices under pressure.

Forward pricing has been stronger. After rolling to March at $2.84/MMBtu, the balance‑of‑month contract climbed above $3/MMBtu. A potential late‑March cool‑down could lift cash prices again before milder April weather returns.

April 2026 NYMEX closed Thursday at $3.003

· High for the day $3.046

· Low for the day $2.920

Early trading for the prompt month is trading at $3.081

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

International Markets: The conflict in Iran has greatly impacted international energy markets. Qatar, the second largest liquified natural gas (LNG) exporter in the world, stopped production of LNG after attacks by Iranian drones. About 20 percent of global LNG exports come from the Persian Gulf and are shipped through the Strait of Hormuz. On Monday, European natural gas futures soared to the highest levels in three years. With the U.S. being the largest LNG exporter in the world, we could see more domestic production allocated to international markets.

EIA Storage: The US Energy Information Administration reported a 132 Bcf withdrawal from natural gas storage for the week ending Feb. 27—slightly above expectations of 125 Bcf and higher than both the five‑year average pull of 96 Bcf and last year’s 106 Bcf. The storage deficit to the five‑year average widened to 43 Bcf (2.2%), while the surplus to 2025 levels narrowed to 115 Bcf (6.5%).

NYMEX Henry Hub April futures traded between $2.92 and $2.96/MMBtu following the report, later rising to $2.99/MMBtu—up 7 cents from the prior settlement.

Regionally, withdrawals were below average in the Pacific and Mountain regions but above average in the East, Midwest, and South Central, expanding regional imbalances. Stocks remain 53.5% above the five‑year average in the Mountain region and 46% above in the Pacific, while other regions sit well below normal.

These disparities are contributing to steep basis discounts across the Rockies and western markets. On March 4, the Cheyenne Hub April forward contract traded $1.50/MMBtu below Henry Hub, and even California’s typically premium SoCal Gas city‑gate showed a 48‑cent discount.

Summary: Working gas in storage totaled 1,886 Bcf as of February 27, 2026, according to EIA estimates. This reflects a 132 Bcf withdrawal from the previous week. Inventories are 115 Bcf above year‑ago levels but 43 Bcf below the five‑year average of 1,929 Bcf. Overall, storage levels remain within the five‑year historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: March is expected to start active and warmer than normal, with severe weather risks increasing as we move into late next week. A brief break in activity may develop around mid‑month.

Severe weather potential is forecast to ramp up during the latter half of next week—especially across southern regions—and expand into the Midwest by next weekend. The upper‑air pattern favors a western trough pushing energy eastward into the Plains, and ample low‑level moisture should support multiple severe weather events.

Snow chances will persist through the first half of March, with enough cold air in place on the northern side of passing systems despite generally above‑average temperatures. However, as the month progresses, accumulating snow will become less likely unless the polar vortex sends a renewed push of Arctic air into the region. Midwest Weather. “March Outlook.” Midwest Weather (Substack), 2026. Subscriber-only newsletter.

March 6, 2026

Weekly Energy News

Market Commentary: Henry Hub cash prices hit a seven‑week low on March 5 as US gas demand fell to its lowest level since mid‑November. Prices briefly dipped to $2.85/MMBtu before settling near $2.89/MMBtu, with warmer temperatures expected to keep spot prices under pressure.

Forward pricing has been stronger. After rolling to March at $2.84/MMBtu, the balance‑of‑month contract climbed above $3/MMBtu. A potential late‑March cool‑down could lift cash prices again before milder April weather returns.

April 2026 NYMEX closed Thursday at $3.003

· High for the day $3.046

· Low for the day $2.920

Early trading for the prompt month is trading at $3.081

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

International Markets: The conflict in Iran has greatly impacted international energy markets. Qatar, the second largest liquified natural gas (LNG) exporter in the world, stopped production of LNG after attacks by Iranian drones. About 20 percent of global LNG exports come from the Persian Gulf and are shipped through the Strait of Hormuz. On Monday, European natural gas futures soared to the highest levels in three years. With the U.S. being the largest LNG exporter in the world, we could see more domestic production allocated to international markets.

EIA Storage: The US Energy Information Administration reported a 132 Bcf withdrawal from natural gas storage for the week ending Feb. 27—slightly above expectations of 125 Bcf and higher than both the five‑year average pull of 96 Bcf and last year’s 106 Bcf. The storage deficit to the five‑year average widened to 43 Bcf (2.2%), while the surplus to 2025 levels narrowed to 115 Bcf (6.5%).

NYMEX Henry Hub April futures traded between $2.92 and $2.96/MMBtu following the report, later rising to $2.99/MMBtu—up 7 cents from the prior settlement.

Regionally, withdrawals were below average in the Pacific and Mountain regions but above average in the East, Midwest, and South Central, expanding regional imbalances. Stocks remain 53.5% above the five‑year average in the Mountain region and 46% above in the Pacific, while other regions sit well below normal.

These disparities are contributing to steep basis discounts across the Rockies and western markets. On March 4, the Cheyenne Hub April forward contract traded $1.50/MMBtu below Henry Hub, and even California’s typically premium SoCal Gas city‑gate showed a 48‑cent discount.

Summary: Working gas in storage totaled 1,886 Bcf as of February 27, 2026, according to EIA estimates. This reflects a 132 Bcf withdrawal from the previous week. Inventories are 115 Bcf above year‑ago levels but 43 Bcf below the five‑year average of 1,929 Bcf. Overall, storage levels remain within the five‑year historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: March is expected to start active and warmer than normal, with severe weather risks increasing as we move into late next week. A brief break in activity may develop around mid‑month.

Severe weather potential is forecast to ramp up during the latter half of next week—especially across southern regions—and expand into the Midwest by next weekend. The upper‑air pattern favors a western trough pushing energy eastward into the Plains, and ample low‑level moisture should support multiple severe weather events.

Snow chances will persist through the first half of March, with enough cold air in place on the northern side of passing systems despite generally above‑average temperatures. However, as the month progresses, accumulating snow will become less likely unless the polar vortex sends a renewed push of Arctic air into the region. Midwest Weather. “March Outlook.” Midwest Weather (Substack), 2026. Subscriber-only newsletter.

March 6, 2026

Market Commentary: Henry Hub cash prices hit a seven‑week low on March 5 as US gas demand fell to its lowest level since mid‑November. Prices briefly dipped to $2.85/MMBtu before settling near $2.89/MMBtu, with warmer temperatures expected to keep spot prices under pressure.

Forward pricing has been stronger. After rolling to March at $2.84/MMBtu, the balance‑of‑month contract climbed above $3/MMBtu. A potential late‑March cool‑down could lift cash prices again before milder April weather returns.

April 2026 NYMEX closed Thursday at $3.003

· High for the day $3.046

· Low for the day $2.920

Early trading for the prompt month is trading at $3.081

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

International Markets: The conflict in Iran has greatly impacted international energy markets. Qatar, the second largest liquified natural gas (LNG) exporter in the world, stopped production of LNG after attacks by Iranian drones. About 20 percent of global LNG exports come from the Persian Gulf and are shipped through the Strait of Hormuz. On Monday, European natural gas futures soared to the highest levels in three years. With the U.S. being the largest LNG exporter in the world, we could see more domestic production allocated to international markets.

EIA Storage: The US Energy Information Administration reported a 132 Bcf withdrawal from natural gas storage for the week ending Feb. 27—slightly above expectations of 125 Bcf and higher than both the five‑year average pull of 96 Bcf and last year’s 106 Bcf. The storage deficit to the five‑year average widened to 43 Bcf (2.2%), while the surplus to 2025 levels narrowed to 115 Bcf (6.5%).

NYMEX Henry Hub April futures traded between $2.92 and $2.96/MMBtu following the report, later rising to $2.99/MMBtu—up 7 cents from the prior settlement.

Regionally, withdrawals were below average in the Pacific and Mountain regions but above average in the East, Midwest, and South Central, expanding regional imbalances. Stocks remain 53.5% above the five‑year average in the Mountain region and 46% above in the Pacific, while other regions sit well below normal.

These disparities are contributing to steep basis discounts across the Rockies and western markets. On March 4, the Cheyenne Hub April forward contract traded $1.50/MMBtu below Henry Hub, and even California’s typically premium SoCal Gas city‑gate showed a 48‑cent discount.

Summary: Working gas in storage totaled 1,886 Bcf as of February 27, 2026, according to EIA estimates. This reflects a 132 Bcf withdrawal from the previous week. Inventories are 115 Bcf above year‑ago levels but 43 Bcf below the five‑year average of 1,929 Bcf. Overall, storage levels remain within the five‑year historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: March is expected to start active and warmer than normal, with severe weather risks increasing as we move into late next week. A brief break in activity may develop around mid‑month.

Severe weather potential is forecast to ramp up during the latter half of next week—especially across southern regions—and expand into the Midwest by next weekend. The upper‑air pattern favors a western trough pushing energy eastward into the Plains, and ample low‑level moisture should support multiple severe weather events.

Snow chances will persist through the first half of March, with enough cold air in place on the northern side of passing systems despite generally above‑average temperatures. However, as the month progresses, accumulating snow will become less likely unless the polar vortex sends a renewed push of Arctic air into the region. Midwest Weather. “March Outlook.” Midwest Weather (Substack), 2026. Subscriber-only newsletter.

March 6, 2026

Weekly Energy News

Market Commentary: Henry Hub cash prices hit a seven‑week low on March 5 as US gas demand fell to its lowest level since mid‑November. Prices briefly dipped to $2.85/MMBtu before settling near $2.89/MMBtu, with warmer temperatures expected to keep spot prices under pressure.

Forward pricing has been stronger. After rolling to March at $2.84/MMBtu, the balance‑of‑month contract climbed above $3/MMBtu. A potential late‑March cool‑down could lift cash prices again before milder April weather returns.

April 2026 NYMEX closed Thursday at $3.003

· High for the day $3.046

· Low for the day $2.920

Early trading for the prompt month is trading at $3.081

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

International Markets: The conflict in Iran has greatly impacted international energy markets. Qatar, the second largest liquified natural gas (LNG) exporter in the world, stopped production of LNG after attacks by Iranian drones. About 20 percent of global LNG exports come from the Persian Gulf and are shipped through the Strait of Hormuz. On Monday, European natural gas futures soared to the highest levels in three years. With the U.S. being the largest LNG exporter in the world, we could see more domestic production allocated to international markets.

EIA Storage: The US Energy Information Administration reported a 132 Bcf withdrawal from natural gas storage for the week ending Feb. 27—slightly above expectations of 125 Bcf and higher than both the five‑year average pull of 96 Bcf and last year’s 106 Bcf. The storage deficit to the five‑year average widened to 43 Bcf (2.2%), while the surplus to 2025 levels narrowed to 115 Bcf (6.5%).

NYMEX Henry Hub April futures traded between $2.92 and $2.96/MMBtu following the report, later rising to $2.99/MMBtu—up 7 cents from the prior settlement.

Regionally, withdrawals were below average in the Pacific and Mountain regions but above average in the East, Midwest, and South Central, expanding regional imbalances. Stocks remain 53.5% above the five‑year average in the Mountain region and 46% above in the Pacific, while other regions sit well below normal.

These disparities are contributing to steep basis discounts across the Rockies and western markets. On March 4, the Cheyenne Hub April forward contract traded $1.50/MMBtu below Henry Hub, and even California’s typically premium SoCal Gas city‑gate showed a 48‑cent discount.

Summary: Working gas in storage totaled 1,886 Bcf as of February 27, 2026, according to EIA estimates. This reflects a 132 Bcf withdrawal from the previous week. Inventories are 115 Bcf above year‑ago levels but 43 Bcf below the five‑year average of 1,929 Bcf. Overall, storage levels remain within the five‑year historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: March is expected to start active and warmer than normal, with severe weather risks increasing as we move into late next week. A brief break in activity may develop around mid‑month.

Severe weather potential is forecast to ramp up during the latter half of next week—especially across southern regions—and expand into the Midwest by next weekend. The upper‑air pattern favors a western trough pushing energy eastward into the Plains, and ample low‑level moisture should support multiple severe weather events.

Snow chances will persist through the first half of March, with enough cold air in place on the northern side of passing systems despite generally above‑average temperatures. However, as the month progresses, accumulating snow will become less likely unless the polar vortex sends a renewed push of Arctic air into the region. Midwest Weather. “March Outlook.” Midwest Weather (Substack), 2026. Subscriber-only newsletter.

March 6, 2026

Weekly Energy News

Market Commentary: Henry Hub cash prices hit a seven‑week low on March 5 as US gas demand fell to its lowest level since mid‑November. Prices briefly dipped to $2.85/MMBtu before settling near $2.89/MMBtu, with warmer temperatures expected to keep spot prices under pressure.

Forward pricing has been stronger. After rolling to March at $2.84/MMBtu, the balance‑of‑month contract climbed above $3/MMBtu. A potential late‑March cool‑down could lift cash prices again before milder April weather returns.

April 2026 NYMEX closed Thursday at $3.003

· High for the day $3.046

· Low for the day $2.920

Early trading for the prompt month is trading at $3.081

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

International Markets: The conflict in Iran has greatly impacted international energy markets. Qatar, the second largest liquified natural gas (LNG) exporter in the world, stopped production of LNG after attacks by Iranian drones. About 20 percent of global LNG exports come from the Persian Gulf and are shipped through the Strait of Hormuz. On Monday, European natural gas futures soared to the highest levels in three years. With the U.S. being the largest LNG exporter in the world, we could see more domestic production allocated to international markets.

EIA Storage: The US Energy Information Administration reported a 132 Bcf withdrawal from natural gas storage for the week ending Feb. 27—slightly above expectations of 125 Bcf and higher than both the five‑year average pull of 96 Bcf and last year’s 106 Bcf. The storage deficit to the five‑year average widened to 43 Bcf (2.2%), while the surplus to 2025 levels narrowed to 115 Bcf (6.5%).

NYMEX Henry Hub April futures traded between $2.92 and $2.96/MMBtu following the report, later rising to $2.99/MMBtu—up 7 cents from the prior settlement.

Regionally, withdrawals were below average in the Pacific and Mountain regions but above average in the East, Midwest, and South Central, expanding regional imbalances. Stocks remain 53.5% above the five‑year average in the Mountain region and 46% above in the Pacific, while other regions sit well below normal.

These disparities are contributing to steep basis discounts across the Rockies and western markets. On March 4, the Cheyenne Hub April forward contract traded $1.50/MMBtu below Henry Hub, and even California’s typically premium SoCal Gas city‑gate showed a 48‑cent discount.

Summary: Working gas in storage totaled 1,886 Bcf as of February 27, 2026, according to EIA estimates. This reflects a 132 Bcf withdrawal from the previous week. Inventories are 115 Bcf above year‑ago levels but 43 Bcf below the five‑year average of 1,929 Bcf. Overall, storage levels remain within the five‑year historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: March is expected to start active and warmer than normal, with severe weather risks increasing as we move into late next week. A brief break in activity may develop around mid‑month.

Severe weather potential is forecast to ramp up during the latter half of next week—especially across southern regions—and expand into the Midwest by next weekend. The upper‑air pattern favors a western trough pushing energy eastward into the Plains, and ample low‑level moisture should support multiple severe weather events.

Snow chances will persist through the first half of March, with enough cold air in place on the northern side of passing systems despite generally above‑average temperatures. However, as the month progresses, accumulating snow will become less likely unless the polar vortex sends a renewed push of Arctic air into the region. Midwest Weather. “March Outlook.” Midwest Weather (Substack), 2026. Subscriber-only newsletter.

Make Your Choice Gas Selection in Three Easy Steps

Click here to access our online tool, or call our Choice gas commodity experts at 1 (877) 790-4990.

Step 1: Enter your account number

- Your Black Hills Energy account number is located at the top right-hand corner of your bill.

Step 2: Review price options and make your selection

Step 3: Confirm your selection and enter your control number

- You received a control number in your 2026 Choice Gas selection packet mailed to you from Black Hills Energy. If you cannot locate this, you can retrieve your control number by calling 877-245-3506 or visit choicegas.com

Once enrolled, you will be removed from supplier marketing communications within 24 hours.

Sign Up for Our Energy Newsletters

Sign UpRecent Posts