March 27, 2026

Weekly Energy News

Market Commentary: The U.S. Energy Information Administration (EIA) reported a 54 Bcf withdrawal from U.S. natural gas storage for the week ending March 20, above market expectations of 48 Bcf. The larger-than-expected draw provided modest bullish support, with NYMEX May futures rising to around $2.96/MMBtu and the April contract briefly touching $3.00.

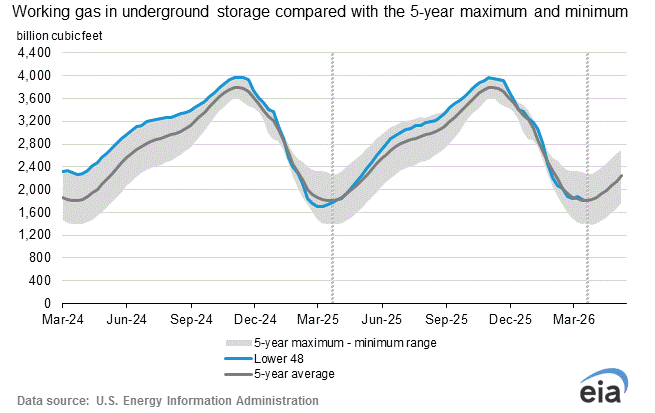

The withdrawal reduced total storage to 1.829 Tcf, likely marking the seasonal low. This followed an unusual mid-March injection the prior week. Compared to the five-year average draw of 21 Bcf for this period, the latest data was relatively supportive for prices.

April 2026 NYMEX closed Thursday at $2.999

· High for the day $3.025

· Low for the day $2.918

Early trading for the prompt month is trading at $3.049

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Outlook: Despite the bullish storage report, natural gas prices have softened back below $3/MMBtu as the market enters the spring shoulder season. Prices briefly approached $3.50 earlier in the month, driven by geopolitical tensions and strength in oil markets, but have since retreated to the low-$2.90s.

Looking ahead, fundamentals remain weak, with expectations for storage surpluses to widen in the coming weeks. Analysts anticipate a return to storage injections, with estimates around a 38 Bcf build for the week ending March 27—exceeding both last year’s 30 Bcf injection and contrasting with the five-year average withdrawal.

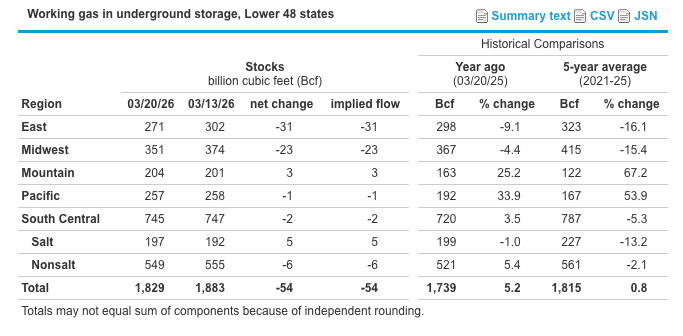

EIA Storage Report: Working gas in storage totaled 1,829 Bcf as of March 20, 2026, according to EIA estimates—down 54 Bcf week over week. Inventories were 90 Bcf higher than the same time last year and 14 Bcf above the five-year average (1,815 Bcf), remaining within the historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: Spring officially began on March 20, and early forecasts point to a warmer-than-normal season for much of the U.S. A large, record-setting heat dome has already brought summer-like conditions to parts of the West, with temperatures climbing into the 90s and even exceeding 100°F in some areas.

Looking ahead, the National Oceanic and Atmospheric Administration Spring Outlook (April–June) indicates above-average temperatures across most of the country, with the strongest likelihood centered in the central Great Basin, Rockies, and Southwest. Cooler exceptions may occur in portions of the northern Plains, Great Lakes, and Northeast.

Drought conditions are also expected to expand or intensify across the West and south-central Plains. In the near term, typical spring variability will continue, with alternating warm and cool periods across the Midwest and Northeast as the heat dome expands eastward.

Source: USA Today (March 21, 2026)

Market Data:

March 27, 2026

Weekly Energy News

March 27, 2026

Market Commentary: The U.S. Energy Information Administration (EIA) reported a 54 Bcf withdrawal from U.S. natural gas storage for the week ending March 20, above market expectations of 48 Bcf. The larger-than-expected draw provided modest bullish support, with NYMEX May futures rising to around $2.96/MMBtu and the April contract briefly touching $3.00.

The withdrawal reduced total storage to 1.829 Tcf, likely marking the seasonal low. This followed an unusual mid-March injection the prior week. Compared to the five-year average draw of 21 Bcf for this period, the latest data was relatively supportive for prices.

April 2026 NYMEX closed Thursday at $2.999

· High for the day $3.025

· Low for the day $2.918

Early trading for the prompt month is trading at $3.049

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Outlook: Despite the bullish storage report, natural gas prices have softened back below $3/MMBtu as the market enters the spring shoulder season. Prices briefly approached $3.50 earlier in the month, driven by geopolitical tensions and strength in oil markets, but have since retreated to the low-$2.90s.

Looking ahead, fundamentals remain weak, with expectations for storage surpluses to widen in the coming weeks. Analysts anticipate a return to storage injections, with estimates around a 38 Bcf build for the week ending March 27—exceeding both last year’s 30 Bcf injection and contrasting with the five-year average withdrawal.

EIA Storage Report: Working gas in storage totaled 1,829 Bcf as of March 20, 2026, according to EIA estimates—down 54 Bcf week over week. Inventories were 90 Bcf higher than the same time last year and 14 Bcf above the five-year average (1,815 Bcf), remaining within the historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: Spring officially began on March 20, and early forecasts point to a warmer-than-normal season for much of the U.S. A large, record-setting heat dome has already brought summer-like conditions to parts of the West, with temperatures climbing into the 90s and even exceeding 100°F in some areas.

Looking ahead, the National Oceanic and Atmospheric Administration Spring Outlook (April–June) indicates above-average temperatures across most of the country, with the strongest likelihood centered in the central Great Basin, Rockies, and Southwest. Cooler exceptions may occur in portions of the northern Plains, Great Lakes, and Northeast.

Drought conditions are also expected to expand or intensify across the West and south-central Plains. In the near term, typical spring variability will continue, with alternating warm and cool periods across the Midwest and Northeast as the heat dome expands eastward.

Source: USA Today (March 21, 2026)

Market Data:

March 27, 2026

March 27, 2026

Weekly Energy News

Market Commentary: The U.S. Energy Information Administration (EIA) reported a 54 Bcf withdrawal from U.S. natural gas storage for the week ending March 20, above market expectations of 48 Bcf. The larger-than-expected draw provided modest bullish support, with NYMEX May futures rising to around $2.96/MMBtu and the April contract briefly touching $3.00.

The withdrawal reduced total storage to 1.829 Tcf, likely marking the seasonal low. This followed an unusual mid-March injection the prior week. Compared to the five-year average draw of 21 Bcf for this period, the latest data was relatively supportive for prices.

April 2026 NYMEX closed Thursday at $2.999

· High for the day $3.025

· Low for the day $2.918

Early trading for the prompt month is trading at $3.049

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Outlook: Despite the bullish storage report, natural gas prices have softened back below $3/MMBtu as the market enters the spring shoulder season. Prices briefly approached $3.50 earlier in the month, driven by geopolitical tensions and strength in oil markets, but have since retreated to the low-$2.90s.

Looking ahead, fundamentals remain weak, with expectations for storage surpluses to widen in the coming weeks. Analysts anticipate a return to storage injections, with estimates around a 38 Bcf build for the week ending March 27—exceeding both last year’s 30 Bcf injection and contrasting with the five-year average withdrawal.

EIA Storage Report: Working gas in storage totaled 1,829 Bcf as of March 20, 2026, according to EIA estimates—down 54 Bcf week over week. Inventories were 90 Bcf higher than the same time last year and 14 Bcf above the five-year average (1,815 Bcf), remaining within the historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: Spring officially began on March 20, and early forecasts point to a warmer-than-normal season for much of the U.S. A large, record-setting heat dome has already brought summer-like conditions to parts of the West, with temperatures climbing into the 90s and even exceeding 100°F in some areas.

Looking ahead, the National Oceanic and Atmospheric Administration Spring Outlook (April–June) indicates above-average temperatures across most of the country, with the strongest likelihood centered in the central Great Basin, Rockies, and Southwest. Cooler exceptions may occur in portions of the northern Plains, Great Lakes, and Northeast.

Drought conditions are also expected to expand or intensify across the West and south-central Plains. In the near term, typical spring variability will continue, with alternating warm and cool periods across the Midwest and Northeast as the heat dome expands eastward.

Source: USA Today (March 21, 2026)

March 27, 2026

Weekly Energy News

Market Commentary: The U.S. Energy Information Administration (EIA) reported a 54 Bcf withdrawal from U.S. natural gas storage for the week ending March 20, above market expectations of 48 Bcf. The larger-than-expected draw provided modest bullish support, with NYMEX May futures rising to around $2.96/MMBtu and the April contract briefly touching $3.00.

The withdrawal reduced total storage to 1.829 Tcf, likely marking the seasonal low. This followed an unusual mid-March injection the prior week. Compared to the five-year average draw of 21 Bcf for this period, the latest data was relatively supportive for prices.

April 2026 NYMEX closed Thursday at $2.999

· High for the day $3.025

· Low for the day $2.918

Early trading for the prompt month is trading at $3.049

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Outlook: Despite the bullish storage report, natural gas prices have softened back below $3/MMBtu as the market enters the spring shoulder season. Prices briefly approached $3.50 earlier in the month, driven by geopolitical tensions and strength in oil markets, but have since retreated to the low-$2.90s.

Looking ahead, fundamentals remain weak, with expectations for storage surpluses to widen in the coming weeks. Analysts anticipate a return to storage injections, with estimates around a 38 Bcf build for the week ending March 27—exceeding both last year’s 30 Bcf injection and contrasting with the five-year average withdrawal.

EIA Storage Report: Working gas in storage totaled 1,829 Bcf as of March 20, 2026, according to EIA estimates—down 54 Bcf week over week. Inventories were 90 Bcf higher than the same time last year and 14 Bcf above the five-year average (1,815 Bcf), remaining within the historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: Spring officially began on March 20, and early forecasts point to a warmer-than-normal season for much of the U.S. A large, record-setting heat dome has already brought summer-like conditions to parts of the West, with temperatures climbing into the 90s and even exceeding 100°F in some areas.

Looking ahead, the National Oceanic and Atmospheric Administration Spring Outlook (April–June) indicates above-average temperatures across most of the country, with the strongest likelihood centered in the central Great Basin, Rockies, and Southwest. Cooler exceptions may occur in portions of the northern Plains, Great Lakes, and Northeast.

Drought conditions are also expected to expand or intensify across the West and south-central Plains. In the near term, typical spring variability will continue, with alternating warm and cool periods across the Midwest and Northeast as the heat dome expands eastward.

Source: USA Today (March 21, 2026)

March 27, 2026

Weekly Energy News

Market Commentary: The U.S. Energy Information Administration (EIA) reported a 54 Bcf withdrawal from U.S. natural gas storage for the week ending March 20, above market expectations of 48 Bcf. The larger-than-expected draw provided modest bullish support, with NYMEX May futures rising to around $2.96/MMBtu and the April contract briefly touching $3.00.

The withdrawal reduced total storage to 1.829 Tcf, likely marking the seasonal low. This followed an unusual mid-March injection the prior week. Compared to the five-year average draw of 21 Bcf for this period, the latest data was relatively supportive for prices.

April 2026 NYMEX closed Thursday at $2.999

· High for the day $3.025

· Low for the day $2.918

Early trading for the prompt month is trading at $3.049

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Outlook: Despite the bullish storage report, natural gas prices have softened back below $3/MMBtu as the market enters the spring shoulder season. Prices briefly approached $3.50 earlier in the month, driven by geopolitical tensions and strength in oil markets, but have since retreated to the low-$2.90s.

Looking ahead, fundamentals remain weak, with expectations for storage surpluses to widen in the coming weeks. Analysts anticipate a return to storage injections, with estimates around a 38 Bcf build for the week ending March 27—exceeding both last year’s 30 Bcf injection and contrasting with the five-year average withdrawal.

EIA Storage Report: Working gas in storage totaled 1,829 Bcf as of March 20, 2026, according to EIA estimates—down 54 Bcf week over week. Inventories were 90 Bcf higher than the same time last year and 14 Bcf above the five-year average (1,815 Bcf), remaining within the historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: Spring officially began on March 20, and early forecasts point to a warmer-than-normal season for much of the U.S. A large, record-setting heat dome has already brought summer-like conditions to parts of the West, with temperatures climbing into the 90s and even exceeding 100°F in some areas.

Looking ahead, the National Oceanic and Atmospheric Administration Spring Outlook (April–June) indicates above-average temperatures across most of the country, with the strongest likelihood centered in the central Great Basin, Rockies, and Southwest. Cooler exceptions may occur in portions of the northern Plains, Great Lakes, and Northeast.

Drought conditions are also expected to expand or intensify across the West and south-central Plains. In the near term, typical spring variability will continue, with alternating warm and cool periods across the Midwest and Northeast as the heat dome expands eastward.

Source: USA Today (March 21, 2026)

March 27, 2026

Market Commentary: The U.S. Energy Information Administration (EIA) reported a 54 Bcf withdrawal from U.S. natural gas storage for the week ending March 20, above market expectations of 48 Bcf. The larger-than-expected draw provided modest bullish support, with NYMEX May futures rising to around $2.96/MMBtu and the April contract briefly touching $3.00.

The withdrawal reduced total storage to 1.829 Tcf, likely marking the seasonal low. This followed an unusual mid-March injection the prior week. Compared to the five-year average draw of 21 Bcf for this period, the latest data was relatively supportive for prices.

April 2026 NYMEX closed Thursday at $2.999

· High for the day $3.025

· Low for the day $2.918

Early trading for the prompt month is trading at $3.049

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Outlook: Despite the bullish storage report, natural gas prices have softened back below $3/MMBtu as the market enters the spring shoulder season. Prices briefly approached $3.50 earlier in the month, driven by geopolitical tensions and strength in oil markets, but have since retreated to the low-$2.90s.

Looking ahead, fundamentals remain weak, with expectations for storage surpluses to widen in the coming weeks. Analysts anticipate a return to storage injections, with estimates around a 38 Bcf build for the week ending March 27—exceeding both last year’s 30 Bcf injection and contrasting with the five-year average withdrawal.

EIA Storage Report: Working gas in storage totaled 1,829 Bcf as of March 20, 2026, according to EIA estimates—down 54 Bcf week over week. Inventories were 90 Bcf higher than the same time last year and 14 Bcf above the five-year average (1,815 Bcf), remaining within the historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: Spring officially began on March 20, and early forecasts point to a warmer-than-normal season for much of the U.S. A large, record-setting heat dome has already brought summer-like conditions to parts of the West, with temperatures climbing into the 90s and even exceeding 100°F in some areas.

Looking ahead, the National Oceanic and Atmospheric Administration Spring Outlook (April–June) indicates above-average temperatures across most of the country, with the strongest likelihood centered in the central Great Basin, Rockies, and Southwest. Cooler exceptions may occur in portions of the northern Plains, Great Lakes, and Northeast.

Drought conditions are also expected to expand or intensify across the West and south-central Plains. In the near term, typical spring variability will continue, with alternating warm and cool periods across the Midwest and Northeast as the heat dome expands eastward.

Source: USA Today (March 21, 2026)

March 27, 2026

Weekly Energy News

Market Commentary: The U.S. Energy Information Administration (EIA) reported a 54 Bcf withdrawal from U.S. natural gas storage for the week ending March 20, above market expectations of 48 Bcf. The larger-than-expected draw provided modest bullish support, with NYMEX May futures rising to around $2.96/MMBtu and the April contract briefly touching $3.00.

The withdrawal reduced total storage to 1.829 Tcf, likely marking the seasonal low. This followed an unusual mid-March injection the prior week. Compared to the five-year average draw of 21 Bcf for this period, the latest data was relatively supportive for prices.

April 2026 NYMEX closed Thursday at $2.999

· High for the day $3.025

· Low for the day $2.918

Early trading for the prompt month is trading at $3.049

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Outlook: Despite the bullish storage report, natural gas prices have softened back below $3/MMBtu as the market enters the spring shoulder season. Prices briefly approached $3.50 earlier in the month, driven by geopolitical tensions and strength in oil markets, but have since retreated to the low-$2.90s.

Looking ahead, fundamentals remain weak, with expectations for storage surpluses to widen in the coming weeks. Analysts anticipate a return to storage injections, with estimates around a 38 Bcf build for the week ending March 27—exceeding both last year’s 30 Bcf injection and contrasting with the five-year average withdrawal.

EIA Storage Report: Working gas in storage totaled 1,829 Bcf as of March 20, 2026, according to EIA estimates—down 54 Bcf week over week. Inventories were 90 Bcf higher than the same time last year and 14 Bcf above the five-year average (1,815 Bcf), remaining within the historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: Spring officially began on March 20, and early forecasts point to a warmer-than-normal season for much of the U.S. A large, record-setting heat dome has already brought summer-like conditions to parts of the West, with temperatures climbing into the 90s and even exceeding 100°F in some areas.

Looking ahead, the National Oceanic and Atmospheric Administration Spring Outlook (April–June) indicates above-average temperatures across most of the country, with the strongest likelihood centered in the central Great Basin, Rockies, and Southwest. Cooler exceptions may occur in portions of the northern Plains, Great Lakes, and Northeast.

Drought conditions are also expected to expand or intensify across the West and south-central Plains. In the near term, typical spring variability will continue, with alternating warm and cool periods across the Midwest and Northeast as the heat dome expands eastward.

Source: USA Today (March 21, 2026)

March 27, 2026

Weekly Energy News

Market Commentary: The U.S. Energy Information Administration (EIA) reported a 54 Bcf withdrawal from U.S. natural gas storage for the week ending March 20, above market expectations of 48 Bcf. The larger-than-expected draw provided modest bullish support, with NYMEX May futures rising to around $2.96/MMBtu and the April contract briefly touching $3.00.

The withdrawal reduced total storage to 1.829 Tcf, likely marking the seasonal low. This followed an unusual mid-March injection the prior week. Compared to the five-year average draw of 21 Bcf for this period, the latest data was relatively supportive for prices.

April 2026 NYMEX closed Thursday at $2.999

· High for the day $3.025

· Low for the day $2.918

Early trading for the prompt month is trading at $3.049

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Outlook: Despite the bullish storage report, natural gas prices have softened back below $3/MMBtu as the market enters the spring shoulder season. Prices briefly approached $3.50 earlier in the month, driven by geopolitical tensions and strength in oil markets, but have since retreated to the low-$2.90s.

Looking ahead, fundamentals remain weak, with expectations for storage surpluses to widen in the coming weeks. Analysts anticipate a return to storage injections, with estimates around a 38 Bcf build for the week ending March 27—exceeding both last year’s 30 Bcf injection and contrasting with the five-year average withdrawal.

EIA Storage Report: Working gas in storage totaled 1,829 Bcf as of March 20, 2026, according to EIA estimates—down 54 Bcf week over week. Inventories were 90 Bcf higher than the same time last year and 14 Bcf above the five-year average (1,815 Bcf), remaining within the historical range.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2021 through 2025. The dashed vertical lines indicate current and year-ago weekly periods.

Weather: Spring officially began on March 20, and early forecasts point to a warmer-than-normal season for much of the U.S. A large, record-setting heat dome has already brought summer-like conditions to parts of the West, with temperatures climbing into the 90s and even exceeding 100°F in some areas.

Looking ahead, the National Oceanic and Atmospheric Administration Spring Outlook (April–June) indicates above-average temperatures across most of the country, with the strongest likelihood centered in the central Great Basin, Rockies, and Southwest. Cooler exceptions may occur in portions of the northern Plains, Great Lakes, and Northeast.

Drought conditions are also expected to expand or intensify across the West and south-central Plains. In the near term, typical spring variability will continue, with alternating warm and cool periods across the Midwest and Northeast as the heat dome expands eastward.

Source: USA Today (March 21, 2026)

Make Your Choice Gas Selection in Three Easy Steps

Click here to access our online tool, or call our Choice gas commodity experts at 1 (877) 790-4990.

Step 1: Enter your account number

- Your Black Hills Energy account number is located at the top right-hand corner of your bill.

Step 2: Review price options and make your selection

Step 3: Confirm your selection and enter your control number

- You received a control number in your 2026 Choice Gas selection packet mailed to you from Black Hills Energy. If you cannot locate this, you can retrieve your control number by calling 877-245-3506 or visit choicegas.com

Once enrolled, you will be removed from supplier marketing communications within 24 hours.

Sign Up for Our Energy Newsletters

Sign UpRecent Posts