July 10, 2026

Weekly Energy News

Market Update:

Natural gas markets fell sharply this week following a third consecutive bearish EIA storage report. The August 2026 NYMEX contract settled at $3.012/MMBtu on July 9, down $0.200 on the day, after EIA reported a 61 Bcf injection — 10 Bcf above the Platts consensus of 51 Bcf. Henry Hub spot for July 10 flows was $3.145/MMBtu. The national average settled at $2.560/MMBtu.

August 2026 NYMEX closed Thursday at $3.012

· High for the day $3.244

· Low for the day $2991

Early trading for the prompt month is trading at $2.935

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Freeport LNG announced it will begin major maintenance starting July 10 through late August, putting roughly 20 cargoes/month of export capacity at risk. Middle East tensions continue to affect roughly 20% of global LNG flows through the Strait of Hormuz, keeping international prices elevated — the August JKM benchmark settled at $17.976/MMBtu on July 9.

In a positive development, the first LNG cargo from Sempra's Energia Costa Azul terminal in Baja California departed July 7 for South Korea, adding new Pacific Basin supply. Domestically, Permian Basin production averaged 25 Bcf/d in early July, up from 23.9 Bcf/d in June, helped by the Gulf Coast Express expansion that came online June 23.

EIA Storage Report:

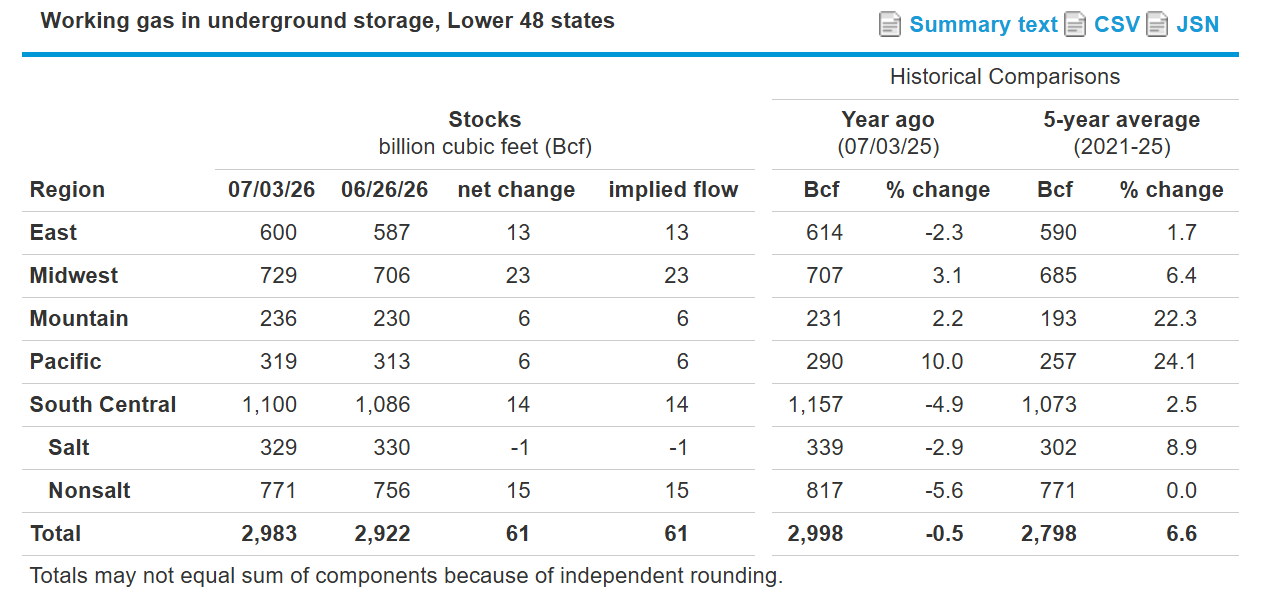

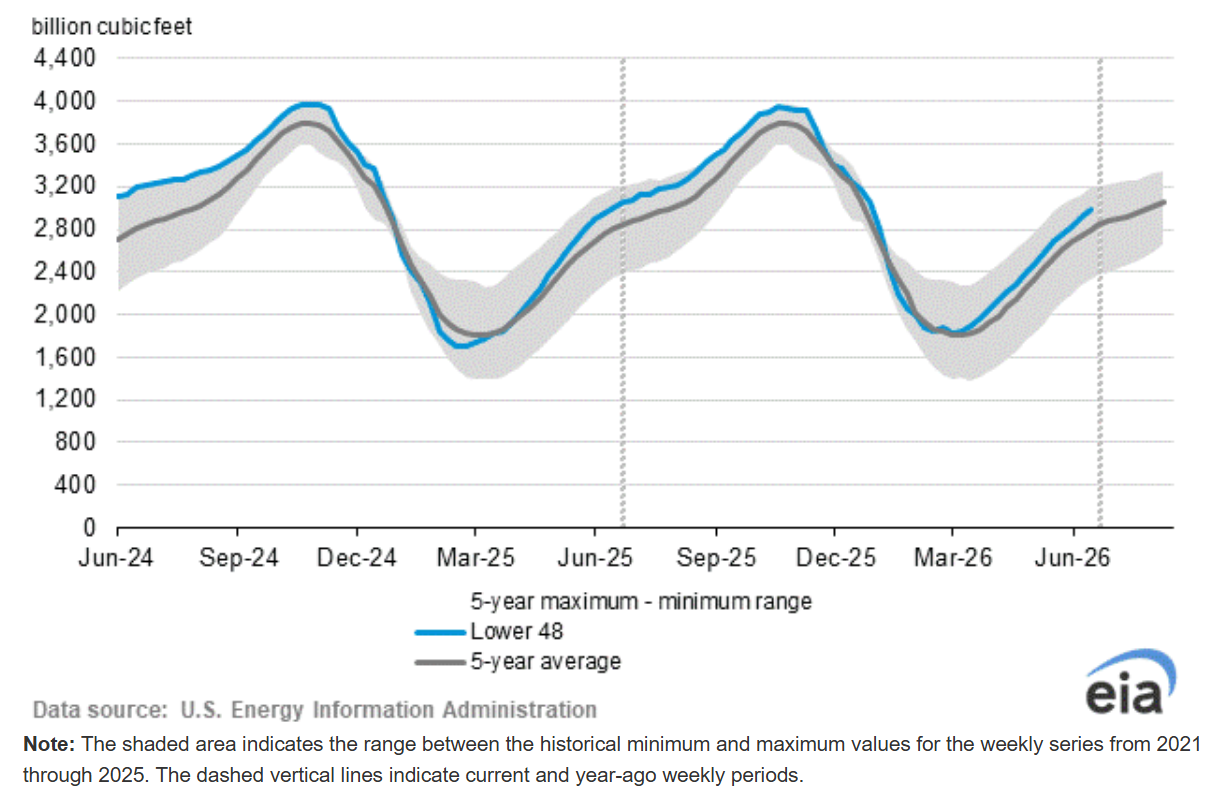

EIA reported a 61 Bcf injection for the week ended July 3, bringing total working gas to 2,983 Bcf. The build came in 10 Bcf above expectations and widened the surplus to the five-year average to 185 Bcf— the highest since September 2025. Inventories are now just 15 Bcf below year-ago levels. Looking ahead, the consensus estimate for the week ending July 10 is approximately 43 Bcf.

Weather:

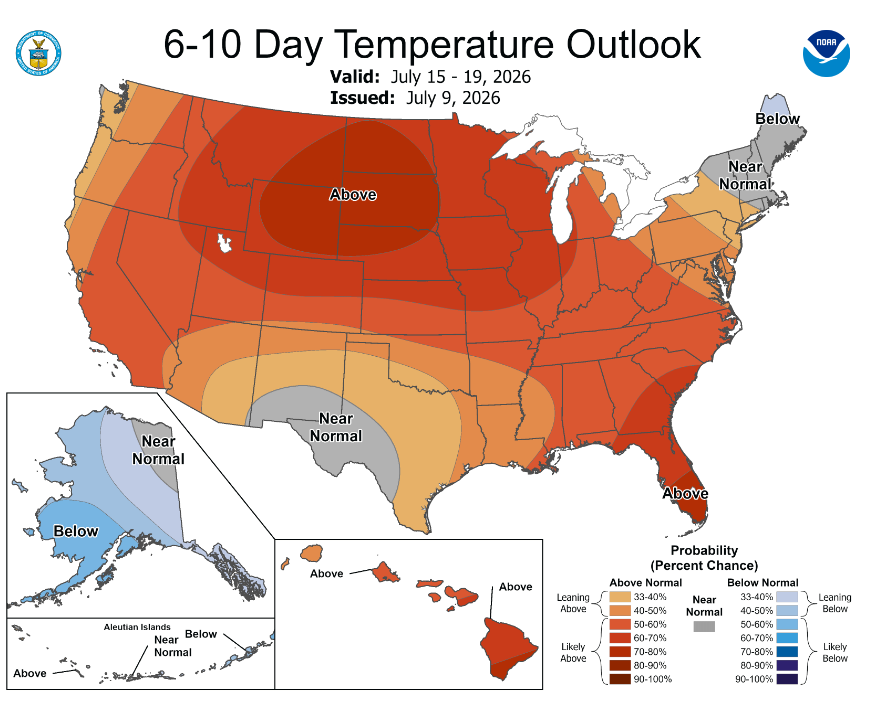

Power sector gas demand averaged 44.2 Bcf/d for the week ended July 3, up 4.5 Bcf/d week over week. NOAA's 8-14 day outlook calls for above-normal temperatures across much of the South, Southeast, and Central US through late July, with the August outlook showing 1-4 degrees F above normal for most of the continental U.S. Despite the summer heat, the widening storage surplus continues to cap price upside.

Market Data:

July 10, 2026

Weekly Energy News

July 10, 2026

Market Update:

Natural gas markets fell sharply this week following a third consecutive bearish EIA storage report. The August 2026 NYMEX contract settled at $3.012/MMBtu on July 9, down $0.200 on the day, after EIA reported a 61 Bcf injection — 10 Bcf above the Platts consensus of 51 Bcf. Henry Hub spot for July 10 flows was $3.145/MMBtu. The national average settled at $2.560/MMBtu.

August 2026 NYMEX closed Thursday at $3.012

· High for the day $3.244

· Low for the day $2991

Early trading for the prompt month is trading at $2.935

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Freeport LNG announced it will begin major maintenance starting July 10 through late August, putting roughly 20 cargoes/month of export capacity at risk. Middle East tensions continue to affect roughly 20% of global LNG flows through the Strait of Hormuz, keeping international prices elevated — the August JKM benchmark settled at $17.976/MMBtu on July 9.

In a positive development, the first LNG cargo from Sempra's Energia Costa Azul terminal in Baja California departed July 7 for South Korea, adding new Pacific Basin supply. Domestically, Permian Basin production averaged 25 Bcf/d in early July, up from 23.9 Bcf/d in June, helped by the Gulf Coast Express expansion that came online June 23.

EIA Storage Report:

EIA reported a 61 Bcf injection for the week ended July 3, bringing total working gas to 2,983 Bcf. The build came in 10 Bcf above expectations and widened the surplus to the five-year average to 185 Bcf— the highest since September 2025. Inventories are now just 15 Bcf below year-ago levels. Looking ahead, the consensus estimate for the week ending July 10 is approximately 43 Bcf.

Weather:

Power sector gas demand averaged 44.2 Bcf/d for the week ended July 3, up 4.5 Bcf/d week over week. NOAA's 8-14 day outlook calls for above-normal temperatures across much of the South, Southeast, and Central US through late July, with the August outlook showing 1-4 degrees F above normal for most of the continental U.S. Despite the summer heat, the widening storage surplus continues to cap price upside.

Market Data:

July 10, 2026

July 10, 2026

Weekly Energy News

Market Update:

Natural gas markets fell sharply this week following a third consecutive bearish EIA storage report. The August 2026 NYMEX contract settled at $3.012/MMBtu on July 9, down $0.200 on the day, after EIA reported a 61 Bcf injection — 10 Bcf above the Platts consensus of 51 Bcf. Henry Hub spot for July 10 flows was $3.145/MMBtu. The national average settled at $2.560/MMBtu.

August 2026 NYMEX closed Thursday at $3.012

· High for the day $3.244

· Low for the day $2991

Early trading for the prompt month is trading at $2.935

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Freeport LNG announced it will begin major maintenance starting July 10 through late August, putting roughly 20 cargoes/month of export capacity at risk. Middle East tensions continue to affect roughly 20% of global LNG flows through the Strait of Hormuz, keeping international prices elevated — the August JKM benchmark settled at $17.976/MMBtu on July 9.

In a positive development, the first LNG cargo from Sempra's Energia Costa Azul terminal in Baja California departed July 7 for South Korea, adding new Pacific Basin supply. Domestically, Permian Basin production averaged 25 Bcf/d in early July, up from 23.9 Bcf/d in June, helped by the Gulf Coast Express expansion that came online June 23.

EIA Storage Report:

EIA reported a 61 Bcf injection for the week ended July 3, bringing total working gas to 2,983 Bcf. The build came in 10 Bcf above expectations and widened the surplus to the five-year average to 185 Bcf— the highest since September 2025. Inventories are now just 15 Bcf below year-ago levels. Looking ahead, the consensus estimate for the week ending July 10 is approximately 43 Bcf.

Weather:

Power sector gas demand averaged 44.2 Bcf/d for the week ended July 3, up 4.5 Bcf/d week over week. NOAA's 8-14 day outlook calls for above-normal temperatures across much of the South, Southeast, and Central US through late July, with the August outlook showing 1-4 degrees F above normal for most of the continental U.S. Despite the summer heat, the widening storage surplus continues to cap price upside.

July 10, 2026

Weekly Energy News

Market Update:

Natural gas markets fell sharply this week following a third consecutive bearish EIA storage report. The August 2026 NYMEX contract settled at $3.012/MMBtu on July 9, down $0.200 on the day, after EIA reported a 61 Bcf injection — 10 Bcf above the Platts consensus of 51 Bcf. Henry Hub spot for July 10 flows was $3.145/MMBtu. The national average settled at $2.560/MMBtu.

August 2026 NYMEX closed Thursday at $3.012

· High for the day $3.244

· Low for the day $2991

Early trading for the prompt month is trading at $2.935

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Freeport LNG announced it will begin major maintenance starting July 10 through late August, putting roughly 20 cargoes/month of export capacity at risk. Middle East tensions continue to affect roughly 20% of global LNG flows through the Strait of Hormuz, keeping international prices elevated — the August JKM benchmark settled at $17.976/MMBtu on July 9.

In a positive development, the first LNG cargo from Sempra's Energia Costa Azul terminal in Baja California departed July 7 for South Korea, adding new Pacific Basin supply. Domestically, Permian Basin production averaged 25 Bcf/d in early July, up from 23.9 Bcf/d in June, helped by the Gulf Coast Express expansion that came online June 23.

EIA Storage Report:

EIA reported a 61 Bcf injection for the week ended July 3, bringing total working gas to 2,983 Bcf. The build came in 10 Bcf above expectations and widened the surplus to the five-year average to 185 Bcf— the highest since September 2025. Inventories are now just 15 Bcf below year-ago levels. Looking ahead, the consensus estimate for the week ending July 10 is approximately 43 Bcf.

Weather:

Power sector gas demand averaged 44.2 Bcf/d for the week ended July 3, up 4.5 Bcf/d week over week. NOAA's 8-14 day outlook calls for above-normal temperatures across much of the South, Southeast, and Central US through late July, with the August outlook showing 1-4 degrees F above normal for most of the continental U.S. Despite the summer heat, the widening storage surplus continues to cap price upside.

July 10, 2026

Weekly Energy News

Market Update:

Natural gas markets fell sharply this week following a third consecutive bearish EIA storage report. The August 2026 NYMEX contract settled at $3.012/MMBtu on July 9, down $0.200 on the day, after EIA reported a 61 Bcf injection — 10 Bcf above the Platts consensus of 51 Bcf. Henry Hub spot for July 10 flows was $3.145/MMBtu. The national average settled at $2.560/MMBtu.

August 2026 NYMEX closed Thursday at $3.012

· High for the day $3.244

· Low for the day $2991

Early trading for the prompt month is trading at $2.935

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Freeport LNG announced it will begin major maintenance starting July 10 through late August, putting roughly 20 cargoes/month of export capacity at risk. Middle East tensions continue to affect roughly 20% of global LNG flows through the Strait of Hormuz, keeping international prices elevated — the August JKM benchmark settled at $17.976/MMBtu on July 9.

In a positive development, the first LNG cargo from Sempra's Energia Costa Azul terminal in Baja California departed July 7 for South Korea, adding new Pacific Basin supply. Domestically, Permian Basin production averaged 25 Bcf/d in early July, up from 23.9 Bcf/d in June, helped by the Gulf Coast Express expansion that came online June 23.

EIA Storage Report:

EIA reported a 61 Bcf injection for the week ended July 3, bringing total working gas to 2,983 Bcf. The build came in 10 Bcf above expectations and widened the surplus to the five-year average to 185 Bcf— the highest since September 2025. Inventories are now just 15 Bcf below year-ago levels. Looking ahead, the consensus estimate for the week ending July 10 is approximately 43 Bcf.

Weather:

Power sector gas demand averaged 44.2 Bcf/d for the week ended July 3, up 4.5 Bcf/d week over week. NOAA's 8-14 day outlook calls for above-normal temperatures across much of the South, Southeast, and Central US through late July, with the August outlook showing 1-4 degrees F above normal for most of the continental U.S. Despite the summer heat, the widening storage surplus continues to cap price upside.

July 10, 2026

Market Update:

Natural gas markets fell sharply this week following a third consecutive bearish EIA storage report. The August 2026 NYMEX contract settled at $3.012/MMBtu on July 9, down $0.200 on the day, after EIA reported a 61 Bcf injection — 10 Bcf above the Platts consensus of 51 Bcf. Henry Hub spot for July 10 flows was $3.145/MMBtu. The national average settled at $2.560/MMBtu.

August 2026 NYMEX closed Thursday at $3.012

· High for the day $3.244

· Low for the day $2991

Early trading for the prompt month is trading at $2.935

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Freeport LNG announced it will begin major maintenance starting July 10 through late August, putting roughly 20 cargoes/month of export capacity at risk. Middle East tensions continue to affect roughly 20% of global LNG flows through the Strait of Hormuz, keeping international prices elevated — the August JKM benchmark settled at $17.976/MMBtu on July 9.

In a positive development, the first LNG cargo from Sempra's Energia Costa Azul terminal in Baja California departed July 7 for South Korea, adding new Pacific Basin supply. Domestically, Permian Basin production averaged 25 Bcf/d in early July, up from 23.9 Bcf/d in June, helped by the Gulf Coast Express expansion that came online June 23.

EIA Storage Report:

EIA reported a 61 Bcf injection for the week ended July 3, bringing total working gas to 2,983 Bcf. The build came in 10 Bcf above expectations and widened the surplus to the five-year average to 185 Bcf— the highest since September 2025. Inventories are now just 15 Bcf below year-ago levels. Looking ahead, the consensus estimate for the week ending July 10 is approximately 43 Bcf.

Weather:

Power sector gas demand averaged 44.2 Bcf/d for the week ended July 3, up 4.5 Bcf/d week over week. NOAA's 8-14 day outlook calls for above-normal temperatures across much of the South, Southeast, and Central US through late July, with the August outlook showing 1-4 degrees F above normal for most of the continental U.S. Despite the summer heat, the widening storage surplus continues to cap price upside.

July 10, 2026

Weekly Energy News

Market Update:

Natural gas markets fell sharply this week following a third consecutive bearish EIA storage report. The August 2026 NYMEX contract settled at $3.012/MMBtu on July 9, down $0.200 on the day, after EIA reported a 61 Bcf injection — 10 Bcf above the Platts consensus of 51 Bcf. Henry Hub spot for July 10 flows was $3.145/MMBtu. The national average settled at $2.560/MMBtu.

August 2026 NYMEX closed Thursday at $3.012

· High for the day $3.244

· Low for the day $2991

Early trading for the prompt month is trading at $2.935

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Freeport LNG announced it will begin major maintenance starting July 10 through late August, putting roughly 20 cargoes/month of export capacity at risk. Middle East tensions continue to affect roughly 20% of global LNG flows through the Strait of Hormuz, keeping international prices elevated — the August JKM benchmark settled at $17.976/MMBtu on July 9.

In a positive development, the first LNG cargo from Sempra's Energia Costa Azul terminal in Baja California departed July 7 for South Korea, adding new Pacific Basin supply. Domestically, Permian Basin production averaged 25 Bcf/d in early July, up from 23.9 Bcf/d in June, helped by the Gulf Coast Express expansion that came online June 23.

EIA Storage Report:

EIA reported a 61 Bcf injection for the week ended July 3, bringing total working gas to 2,983 Bcf. The build came in 10 Bcf above expectations and widened the surplus to the five-year average to 185 Bcf— the highest since September 2025. Inventories are now just 15 Bcf below year-ago levels. Looking ahead, the consensus estimate for the week ending July 10 is approximately 43 Bcf.

Weather:

Power sector gas demand averaged 44.2 Bcf/d for the week ended July 3, up 4.5 Bcf/d week over week. NOAA's 8-14 day outlook calls for above-normal temperatures across much of the South, Southeast, and Central US through late July, with the August outlook showing 1-4 degrees F above normal for most of the continental U.S. Despite the summer heat, the widening storage surplus continues to cap price upside.

July 10, 2026

Weekly Energy News

Market Update:

Natural gas markets fell sharply this week following a third consecutive bearish EIA storage report. The August 2026 NYMEX contract settled at $3.012/MMBtu on July 9, down $0.200 on the day, after EIA reported a 61 Bcf injection — 10 Bcf above the Platts consensus of 51 Bcf. Henry Hub spot for July 10 flows was $3.145/MMBtu. The national average settled at $2.560/MMBtu.

August 2026 NYMEX closed Thursday at $3.012

· High for the day $3.244

· Low for the day $2991

Early trading for the prompt month is trading at $2.935

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

Freeport LNG announced it will begin major maintenance starting July 10 through late August, putting roughly 20 cargoes/month of export capacity at risk. Middle East tensions continue to affect roughly 20% of global LNG flows through the Strait of Hormuz, keeping international prices elevated — the August JKM benchmark settled at $17.976/MMBtu on July 9.

In a positive development, the first LNG cargo from Sempra's Energia Costa Azul terminal in Baja California departed July 7 for South Korea, adding new Pacific Basin supply. Domestically, Permian Basin production averaged 25 Bcf/d in early July, up from 23.9 Bcf/d in June, helped by the Gulf Coast Express expansion that came online June 23.

EIA Storage Report:

EIA reported a 61 Bcf injection for the week ended July 3, bringing total working gas to 2,983 Bcf. The build came in 10 Bcf above expectations and widened the surplus to the five-year average to 185 Bcf— the highest since September 2025. Inventories are now just 15 Bcf below year-ago levels. Looking ahead, the consensus estimate for the week ending July 10 is approximately 43 Bcf.

Weather:

Power sector gas demand averaged 44.2 Bcf/d for the week ended July 3, up 4.5 Bcf/d week over week. NOAA's 8-14 day outlook calls for above-normal temperatures across much of the South, Southeast, and Central US through late July, with the August outlook showing 1-4 degrees F above normal for most of the continental U.S. Despite the summer heat, the widening storage surplus continues to cap price upside.

Make Your Choice Gas Selection in Three Easy Steps

Click here to access our online tool, or call our Choice gas commodity experts at 1 (877) 790-4990.

Step 1: Enter your account number

- Your Black Hills Energy account number is located at the top right-hand corner of your bill.

Step 2: Review price options and make your selection

Step 3: Confirm your selection and enter your control number

- You received a control number in your 2026 Choice Gas selection packet mailed to you from Black Hills Energy. If you cannot locate this, you can retrieve your control number by calling 877-245-3506 or visit choicegas.com

Once enrolled, you will be removed from supplier marketing communications within 24 hours.

Sign Up for Our Energy Newsletters

Sign Up