April 24, 2026

Weekly Energy News

Market Commentary: Natural gas markets moved lower on April 23 following the latest storage data from the U.S. Energy Information Administration. The agency reported a 103 Bcf injection into U.S. gas storage for the week ending April 17, exceeding market expectations of 95 Bcf and coming in well above both the five-year average injection of 64 Bcf and last year’s 77 Bcf build. Even with a slight downward revision to the prior week’s storage levels, the report was viewed as bearish and contributed to downward pressure on prices.

In response, NYMEX Henry Hub futures for May delivery fell immediately after the release, dropping about five cents to $2.60/MMBtu and briefly dipping below $2.57/MMBtu during intraday trading before stabilizing near $2.60 by early afternoon. The decline reflects a broader loosening in market fundamentals, driven largely by weaker demand trends.

May 2026 NYMEX closed Thursday at $2.614

· High for the day $2.74

· Low for the day $2.568

Early trading for the prompt month is trading at $2.688

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

April demand, particularly in the residential and commercial sectors, has remained well below average due to mild weather conditions. However, forecasts suggest a seasonal rebound, with demand expected to rise above the five-year average in late April and early May. Analysts note that the transition toward more typical weather patterns could provide some near-term support for prices, though the absence of early-season heat may limit bullish momentum heading into summer.

Total demand fell by nearly 7 Bcf/d in the week ending April 17, with residential and commercial demand dropping sharply and remaining significantly below historical norms. Industrial demand also declined modestly, while power sector demand provided a partial offset with a weekly increase. On the supply side, overall production edged lower, though increased imports from Canada helped mitigate some of the decline.

Looking ahead, early data for the current week shows a modest recovery in demand, particularly in the residential-commercial segment. As a result, storage injections are expected to return closer to seasonal norms. Estimates for the week ending April 24 point to an injection of approximately 62 Bcf, aligning closely with the five-year average and significantly below last year’s 105 Bcf build for the same period.

In the broader energy sector, U.S. drilling activity ticked slightly higher in mid-April. Total active rigs increased to 577, driven by gains in oil-directed drilling, while natural gas-focused rigs saw a slight decline. The Permian Basin continues to lead activity, adding rigs and maintaining its position as the most active oil-producing region in the country, while other major basins showed mixed performance.

Looking further out, expectations for U.S. production remain cautiously optimistic. Industry executives anticipate moderate production growth over the next two years, supported by efficiency improvements rather than aggressive expansion.

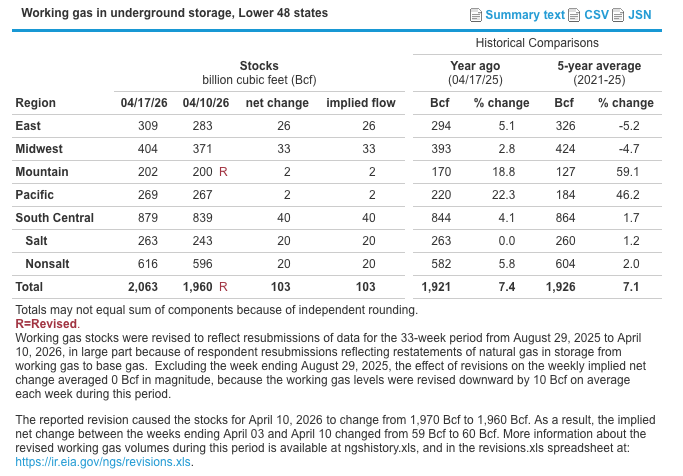

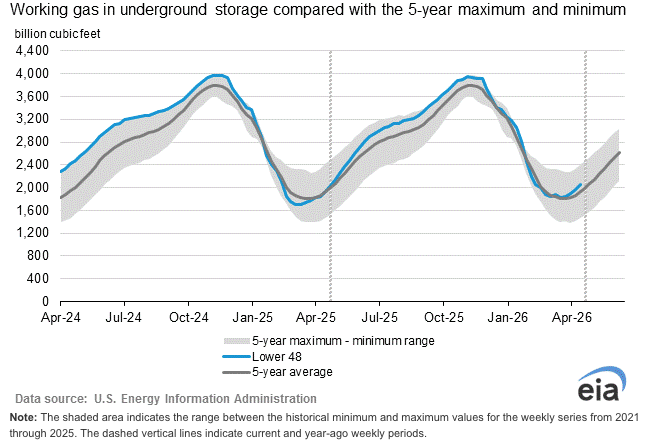

EIA Storage Report: According to estimates from the U.S. Energy Information Administration, working gas in storage stood at 2,063 Bcf as of Friday, April 17, 2026, reflecting a weekly increase of 103 Bcf. Storage levels were 142 Bcf higher than the same time last year and 137 Bcf above the five-year average of 1,926 Bcf. Overall, total working gas inventories remain within the historical five-year range.

Weather: Weather patterns across the United States may shift later in 2026 as El Niño conditions are increasingly expected to develop. The NOAA Climate Prediction Center has issued an El Niño watch, with forecasts calling for a transition from La Niña to ENSO-neutral conditions in the near term, followed by El Niño emerging by summer and persisting through the end of the year.

Confidence in this outlook continues to build, with some projections suggesting the potential for a stronger-than-average El Niño. In certain scenarios, sea surface temperature anomalies could climb well above normal, raising the possibility of a more impactful El Niño depending on how atmospheric and oceanic conditions evolve over the coming months.

El Niño typically shifts the Pacific jet stream southward, leading to warmer and drier conditions across the northern United States. Historically, this pattern results in milder, less snowy winters in the Midwest, while other seasons tend to see cooler, wetter conditions in late summer and fall, followed by drier trends in the spring.

In addition to temperature and precipitation impacts, El Niño often suppresses Atlantic hurricane activity. Stronger upper-level winds and increased atmospheric stability create less favorable conditions for storm development, which typically leads to a quieter hurricane season.

Market Data:

April 24, 2026

Weekly Energy News

April 24, 2026

Market Commentary: Natural gas markets moved lower on April 23 following the latest storage data from the U.S. Energy Information Administration. The agency reported a 103 Bcf injection into U.S. gas storage for the week ending April 17, exceeding market expectations of 95 Bcf and coming in well above both the five-year average injection of 64 Bcf and last year’s 77 Bcf build. Even with a slight downward revision to the prior week’s storage levels, the report was viewed as bearish and contributed to downward pressure on prices.

In response, NYMEX Henry Hub futures for May delivery fell immediately after the release, dropping about five cents to $2.60/MMBtu and briefly dipping below $2.57/MMBtu during intraday trading before stabilizing near $2.60 by early afternoon. The decline reflects a broader loosening in market fundamentals, driven largely by weaker demand trends.

May 2026 NYMEX closed Thursday at $2.614

· High for the day $2.74

· Low for the day $2.568

Early trading for the prompt month is trading at $2.688

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

April demand, particularly in the residential and commercial sectors, has remained well below average due to mild weather conditions. However, forecasts suggest a seasonal rebound, with demand expected to rise above the five-year average in late April and early May. Analysts note that the transition toward more typical weather patterns could provide some near-term support for prices, though the absence of early-season heat may limit bullish momentum heading into summer.

Total demand fell by nearly 7 Bcf/d in the week ending April 17, with residential and commercial demand dropping sharply and remaining significantly below historical norms. Industrial demand also declined modestly, while power sector demand provided a partial offset with a weekly increase. On the supply side, overall production edged lower, though increased imports from Canada helped mitigate some of the decline.

Looking ahead, early data for the current week shows a modest recovery in demand, particularly in the residential-commercial segment. As a result, storage injections are expected to return closer to seasonal norms. Estimates for the week ending April 24 point to an injection of approximately 62 Bcf, aligning closely with the five-year average and significantly below last year’s 105 Bcf build for the same period.

In the broader energy sector, U.S. drilling activity ticked slightly higher in mid-April. Total active rigs increased to 577, driven by gains in oil-directed drilling, while natural gas-focused rigs saw a slight decline. The Permian Basin continues to lead activity, adding rigs and maintaining its position as the most active oil-producing region in the country, while other major basins showed mixed performance.

Looking further out, expectations for U.S. production remain cautiously optimistic. Industry executives anticipate moderate production growth over the next two years, supported by efficiency improvements rather than aggressive expansion.

EIA Storage Report: According to estimates from the U.S. Energy Information Administration, working gas in storage stood at 2,063 Bcf as of Friday, April 17, 2026, reflecting a weekly increase of 103 Bcf. Storage levels were 142 Bcf higher than the same time last year and 137 Bcf above the five-year average of 1,926 Bcf. Overall, total working gas inventories remain within the historical five-year range.

Weather: Weather patterns across the United States may shift later in 2026 as El Niño conditions are increasingly expected to develop. The NOAA Climate Prediction Center has issued an El Niño watch, with forecasts calling for a transition from La Niña to ENSO-neutral conditions in the near term, followed by El Niño emerging by summer and persisting through the end of the year.

Confidence in this outlook continues to build, with some projections suggesting the potential for a stronger-than-average El Niño. In certain scenarios, sea surface temperature anomalies could climb well above normal, raising the possibility of a more impactful El Niño depending on how atmospheric and oceanic conditions evolve over the coming months.

El Niño typically shifts the Pacific jet stream southward, leading to warmer and drier conditions across the northern United States. Historically, this pattern results in milder, less snowy winters in the Midwest, while other seasons tend to see cooler, wetter conditions in late summer and fall, followed by drier trends in the spring.

In addition to temperature and precipitation impacts, El Niño often suppresses Atlantic hurricane activity. Stronger upper-level winds and increased atmospheric stability create less favorable conditions for storm development, which typically leads to a quieter hurricane season.

Market Data:

April 24, 2026

April 24, 2026

Weekly Energy News

Market Commentary: Natural gas markets moved lower on April 23 following the latest storage data from the U.S. Energy Information Administration. The agency reported a 103 Bcf injection into U.S. gas storage for the week ending April 17, exceeding market expectations of 95 Bcf and coming in well above both the five-year average injection of 64 Bcf and last year’s 77 Bcf build. Even with a slight downward revision to the prior week’s storage levels, the report was viewed as bearish and contributed to downward pressure on prices.

In response, NYMEX Henry Hub futures for May delivery fell immediately after the release, dropping about five cents to $2.60/MMBtu and briefly dipping below $2.57/MMBtu during intraday trading before stabilizing near $2.60 by early afternoon. The decline reflects a broader loosening in market fundamentals, driven largely by weaker demand trends.

May 2026 NYMEX closed Thursday at $2.614

· High for the day $2.74

· Low for the day $2.568

Early trading for the prompt month is trading at $2.688

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

April demand, particularly in the residential and commercial sectors, has remained well below average due to mild weather conditions. However, forecasts suggest a seasonal rebound, with demand expected to rise above the five-year average in late April and early May. Analysts note that the transition toward more typical weather patterns could provide some near-term support for prices, though the absence of early-season heat may limit bullish momentum heading into summer.

Total demand fell by nearly 7 Bcf/d in the week ending April 17, with residential and commercial demand dropping sharply and remaining significantly below historical norms. Industrial demand also declined modestly, while power sector demand provided a partial offset with a weekly increase. On the supply side, overall production edged lower, though increased imports from Canada helped mitigate some of the decline.

Looking ahead, early data for the current week shows a modest recovery in demand, particularly in the residential-commercial segment. As a result, storage injections are expected to return closer to seasonal norms. Estimates for the week ending April 24 point to an injection of approximately 62 Bcf, aligning closely with the five-year average and significantly below last year’s 105 Bcf build for the same period.

In the broader energy sector, U.S. drilling activity ticked slightly higher in mid-April. Total active rigs increased to 577, driven by gains in oil-directed drilling, while natural gas-focused rigs saw a slight decline. The Permian Basin continues to lead activity, adding rigs and maintaining its position as the most active oil-producing region in the country, while other major basins showed mixed performance.

Looking further out, expectations for U.S. production remain cautiously optimistic. Industry executives anticipate moderate production growth over the next two years, supported by efficiency improvements rather than aggressive expansion.

EIA Storage Report: According to estimates from the U.S. Energy Information Administration, working gas in storage stood at 2,063 Bcf as of Friday, April 17, 2026, reflecting a weekly increase of 103 Bcf. Storage levels were 142 Bcf higher than the same time last year and 137 Bcf above the five-year average of 1,926 Bcf. Overall, total working gas inventories remain within the historical five-year range.

Weather: Weather patterns across the United States may shift later in 2026 as El Niño conditions are increasingly expected to develop. The NOAA Climate Prediction Center has issued an El Niño watch, with forecasts calling for a transition from La Niña to ENSO-neutral conditions in the near term, followed by El Niño emerging by summer and persisting through the end of the year.

Confidence in this outlook continues to build, with some projections suggesting the potential for a stronger-than-average El Niño. In certain scenarios, sea surface temperature anomalies could climb well above normal, raising the possibility of a more impactful El Niño depending on how atmospheric and oceanic conditions evolve over the coming months.

El Niño typically shifts the Pacific jet stream southward, leading to warmer and drier conditions across the northern United States. Historically, this pattern results in milder, less snowy winters in the Midwest, while other seasons tend to see cooler, wetter conditions in late summer and fall, followed by drier trends in the spring.

In addition to temperature and precipitation impacts, El Niño often suppresses Atlantic hurricane activity. Stronger upper-level winds and increased atmospheric stability create less favorable conditions for storm development, which typically leads to a quieter hurricane season.

April 24, 2026

Weekly Energy News

Market Commentary: Natural gas markets moved lower on April 23 following the latest storage data from the U.S. Energy Information Administration. The agency reported a 103 Bcf injection into U.S. gas storage for the week ending April 17, exceeding market expectations of 95 Bcf and coming in well above both the five-year average injection of 64 Bcf and last year’s 77 Bcf build. Even with a slight downward revision to the prior week’s storage levels, the report was viewed as bearish and contributed to downward pressure on prices.

In response, NYMEX Henry Hub futures for May delivery fell immediately after the release, dropping about five cents to $2.60/MMBtu and briefly dipping below $2.57/MMBtu during intraday trading before stabilizing near $2.60 by early afternoon. The decline reflects a broader loosening in market fundamentals, driven largely by weaker demand trends.

May 2026 NYMEX closed Thursday at $2.614

· High for the day $2.74

· Low for the day $2.568

Early trading for the prompt month is trading at $2.688

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

April demand, particularly in the residential and commercial sectors, has remained well below average due to mild weather conditions. However, forecasts suggest a seasonal rebound, with demand expected to rise above the five-year average in late April and early May. Analysts note that the transition toward more typical weather patterns could provide some near-term support for prices, though the absence of early-season heat may limit bullish momentum heading into summer.

Total demand fell by nearly 7 Bcf/d in the week ending April 17, with residential and commercial demand dropping sharply and remaining significantly below historical norms. Industrial demand also declined modestly, while power sector demand provided a partial offset with a weekly increase. On the supply side, overall production edged lower, though increased imports from Canada helped mitigate some of the decline.

Looking ahead, early data for the current week shows a modest recovery in demand, particularly in the residential-commercial segment. As a result, storage injections are expected to return closer to seasonal norms. Estimates for the week ending April 24 point to an injection of approximately 62 Bcf, aligning closely with the five-year average and significantly below last year’s 105 Bcf build for the same period.

In the broader energy sector, U.S. drilling activity ticked slightly higher in mid-April. Total active rigs increased to 577, driven by gains in oil-directed drilling, while natural gas-focused rigs saw a slight decline. The Permian Basin continues to lead activity, adding rigs and maintaining its position as the most active oil-producing region in the country, while other major basins showed mixed performance.

Looking further out, expectations for U.S. production remain cautiously optimistic. Industry executives anticipate moderate production growth over the next two years, supported by efficiency improvements rather than aggressive expansion.

EIA Storage Report: According to estimates from the U.S. Energy Information Administration, working gas in storage stood at 2,063 Bcf as of Friday, April 17, 2026, reflecting a weekly increase of 103 Bcf. Storage levels were 142 Bcf higher than the same time last year and 137 Bcf above the five-year average of 1,926 Bcf. Overall, total working gas inventories remain within the historical five-year range.

Weather: Weather patterns across the United States may shift later in 2026 as El Niño conditions are increasingly expected to develop. The NOAA Climate Prediction Center has issued an El Niño watch, with forecasts calling for a transition from La Niña to ENSO-neutral conditions in the near term, followed by El Niño emerging by summer and persisting through the end of the year.

Confidence in this outlook continues to build, with some projections suggesting the potential for a stronger-than-average El Niño. In certain scenarios, sea surface temperature anomalies could climb well above normal, raising the possibility of a more impactful El Niño depending on how atmospheric and oceanic conditions evolve over the coming months.

El Niño typically shifts the Pacific jet stream southward, leading to warmer and drier conditions across the northern United States. Historically, this pattern results in milder, less snowy winters in the Midwest, while other seasons tend to see cooler, wetter conditions in late summer and fall, followed by drier trends in the spring.

In addition to temperature and precipitation impacts, El Niño often suppresses Atlantic hurricane activity. Stronger upper-level winds and increased atmospheric stability create less favorable conditions for storm development, which typically leads to a quieter hurricane season.

April 24, 2026

Weekly Energy News

Market Commentary: Natural gas markets moved lower on April 23 following the latest storage data from the U.S. Energy Information Administration. The agency reported a 103 Bcf injection into U.S. gas storage for the week ending April 17, exceeding market expectations of 95 Bcf and coming in well above both the five-year average injection of 64 Bcf and last year’s 77 Bcf build. Even with a slight downward revision to the prior week’s storage levels, the report was viewed as bearish and contributed to downward pressure on prices.

In response, NYMEX Henry Hub futures for May delivery fell immediately after the release, dropping about five cents to $2.60/MMBtu and briefly dipping below $2.57/MMBtu during intraday trading before stabilizing near $2.60 by early afternoon. The decline reflects a broader loosening in market fundamentals, driven largely by weaker demand trends.

May 2026 NYMEX closed Thursday at $2.614

· High for the day $2.74

· Low for the day $2.568

Early trading for the prompt month is trading at $2.688

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

April demand, particularly in the residential and commercial sectors, has remained well below average due to mild weather conditions. However, forecasts suggest a seasonal rebound, with demand expected to rise above the five-year average in late April and early May. Analysts note that the transition toward more typical weather patterns could provide some near-term support for prices, though the absence of early-season heat may limit bullish momentum heading into summer.

Total demand fell by nearly 7 Bcf/d in the week ending April 17, with residential and commercial demand dropping sharply and remaining significantly below historical norms. Industrial demand also declined modestly, while power sector demand provided a partial offset with a weekly increase. On the supply side, overall production edged lower, though increased imports from Canada helped mitigate some of the decline.

Looking ahead, early data for the current week shows a modest recovery in demand, particularly in the residential-commercial segment. As a result, storage injections are expected to return closer to seasonal norms. Estimates for the week ending April 24 point to an injection of approximately 62 Bcf, aligning closely with the five-year average and significantly below last year’s 105 Bcf build for the same period.

In the broader energy sector, U.S. drilling activity ticked slightly higher in mid-April. Total active rigs increased to 577, driven by gains in oil-directed drilling, while natural gas-focused rigs saw a slight decline. The Permian Basin continues to lead activity, adding rigs and maintaining its position as the most active oil-producing region in the country, while other major basins showed mixed performance.

Looking further out, expectations for U.S. production remain cautiously optimistic. Industry executives anticipate moderate production growth over the next two years, supported by efficiency improvements rather than aggressive expansion.

EIA Storage Report: According to estimates from the U.S. Energy Information Administration, working gas in storage stood at 2,063 Bcf as of Friday, April 17, 2026, reflecting a weekly increase of 103 Bcf. Storage levels were 142 Bcf higher than the same time last year and 137 Bcf above the five-year average of 1,926 Bcf. Overall, total working gas inventories remain within the historical five-year range.

Weather: Weather patterns across the United States may shift later in 2026 as El Niño conditions are increasingly expected to develop. The NOAA Climate Prediction Center has issued an El Niño watch, with forecasts calling for a transition from La Niña to ENSO-neutral conditions in the near term, followed by El Niño emerging by summer and persisting through the end of the year.

Confidence in this outlook continues to build, with some projections suggesting the potential for a stronger-than-average El Niño. In certain scenarios, sea surface temperature anomalies could climb well above normal, raising the possibility of a more impactful El Niño depending on how atmospheric and oceanic conditions evolve over the coming months.

El Niño typically shifts the Pacific jet stream southward, leading to warmer and drier conditions across the northern United States. Historically, this pattern results in milder, less snowy winters in the Midwest, while other seasons tend to see cooler, wetter conditions in late summer and fall, followed by drier trends in the spring.

In addition to temperature and precipitation impacts, El Niño often suppresses Atlantic hurricane activity. Stronger upper-level winds and increased atmospheric stability create less favorable conditions for storm development, which typically leads to a quieter hurricane season.

April 24, 2026

Market Commentary: Natural gas markets moved lower on April 23 following the latest storage data from the U.S. Energy Information Administration. The agency reported a 103 Bcf injection into U.S. gas storage for the week ending April 17, exceeding market expectations of 95 Bcf and coming in well above both the five-year average injection of 64 Bcf and last year’s 77 Bcf build. Even with a slight downward revision to the prior week’s storage levels, the report was viewed as bearish and contributed to downward pressure on prices.

In response, NYMEX Henry Hub futures for May delivery fell immediately after the release, dropping about five cents to $2.60/MMBtu and briefly dipping below $2.57/MMBtu during intraday trading before stabilizing near $2.60 by early afternoon. The decline reflects a broader loosening in market fundamentals, driven largely by weaker demand trends.

May 2026 NYMEX closed Thursday at $2.614

· High for the day $2.74

· Low for the day $2.568

Early trading for the prompt month is trading at $2.688

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

April demand, particularly in the residential and commercial sectors, has remained well below average due to mild weather conditions. However, forecasts suggest a seasonal rebound, with demand expected to rise above the five-year average in late April and early May. Analysts note that the transition toward more typical weather patterns could provide some near-term support for prices, though the absence of early-season heat may limit bullish momentum heading into summer.

Total demand fell by nearly 7 Bcf/d in the week ending April 17, with residential and commercial demand dropping sharply and remaining significantly below historical norms. Industrial demand also declined modestly, while power sector demand provided a partial offset with a weekly increase. On the supply side, overall production edged lower, though increased imports from Canada helped mitigate some of the decline.

Looking ahead, early data for the current week shows a modest recovery in demand, particularly in the residential-commercial segment. As a result, storage injections are expected to return closer to seasonal norms. Estimates for the week ending April 24 point to an injection of approximately 62 Bcf, aligning closely with the five-year average and significantly below last year’s 105 Bcf build for the same period.

In the broader energy sector, U.S. drilling activity ticked slightly higher in mid-April. Total active rigs increased to 577, driven by gains in oil-directed drilling, while natural gas-focused rigs saw a slight decline. The Permian Basin continues to lead activity, adding rigs and maintaining its position as the most active oil-producing region in the country, while other major basins showed mixed performance.

Looking further out, expectations for U.S. production remain cautiously optimistic. Industry executives anticipate moderate production growth over the next two years, supported by efficiency improvements rather than aggressive expansion.

EIA Storage Report: According to estimates from the U.S. Energy Information Administration, working gas in storage stood at 2,063 Bcf as of Friday, April 17, 2026, reflecting a weekly increase of 103 Bcf. Storage levels were 142 Bcf higher than the same time last year and 137 Bcf above the five-year average of 1,926 Bcf. Overall, total working gas inventories remain within the historical five-year range.

Weather: Weather patterns across the United States may shift later in 2026 as El Niño conditions are increasingly expected to develop. The NOAA Climate Prediction Center has issued an El Niño watch, with forecasts calling for a transition from La Niña to ENSO-neutral conditions in the near term, followed by El Niño emerging by summer and persisting through the end of the year.

Confidence in this outlook continues to build, with some projections suggesting the potential for a stronger-than-average El Niño. In certain scenarios, sea surface temperature anomalies could climb well above normal, raising the possibility of a more impactful El Niño depending on how atmospheric and oceanic conditions evolve over the coming months.

El Niño typically shifts the Pacific jet stream southward, leading to warmer and drier conditions across the northern United States. Historically, this pattern results in milder, less snowy winters in the Midwest, while other seasons tend to see cooler, wetter conditions in late summer and fall, followed by drier trends in the spring.

In addition to temperature and precipitation impacts, El Niño often suppresses Atlantic hurricane activity. Stronger upper-level winds and increased atmospheric stability create less favorable conditions for storm development, which typically leads to a quieter hurricane season.

April 24, 2026

Weekly Energy News

Market Commentary: Natural gas markets moved lower on April 23 following the latest storage data from the U.S. Energy Information Administration. The agency reported a 103 Bcf injection into U.S. gas storage for the week ending April 17, exceeding market expectations of 95 Bcf and coming in well above both the five-year average injection of 64 Bcf and last year’s 77 Bcf build. Even with a slight downward revision to the prior week’s storage levels, the report was viewed as bearish and contributed to downward pressure on prices.

In response, NYMEX Henry Hub futures for May delivery fell immediately after the release, dropping about five cents to $2.60/MMBtu and briefly dipping below $2.57/MMBtu during intraday trading before stabilizing near $2.60 by early afternoon. The decline reflects a broader loosening in market fundamentals, driven largely by weaker demand trends.

May 2026 NYMEX closed Thursday at $2.614

· High for the day $2.74

· Low for the day $2.568

Early trading for the prompt month is trading at $2.688

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

April demand, particularly in the residential and commercial sectors, has remained well below average due to mild weather conditions. However, forecasts suggest a seasonal rebound, with demand expected to rise above the five-year average in late April and early May. Analysts note that the transition toward more typical weather patterns could provide some near-term support for prices, though the absence of early-season heat may limit bullish momentum heading into summer.

Total demand fell by nearly 7 Bcf/d in the week ending April 17, with residential and commercial demand dropping sharply and remaining significantly below historical norms. Industrial demand also declined modestly, while power sector demand provided a partial offset with a weekly increase. On the supply side, overall production edged lower, though increased imports from Canada helped mitigate some of the decline.

Looking ahead, early data for the current week shows a modest recovery in demand, particularly in the residential-commercial segment. As a result, storage injections are expected to return closer to seasonal norms. Estimates for the week ending April 24 point to an injection of approximately 62 Bcf, aligning closely with the five-year average and significantly below last year’s 105 Bcf build for the same period.

In the broader energy sector, U.S. drilling activity ticked slightly higher in mid-April. Total active rigs increased to 577, driven by gains in oil-directed drilling, while natural gas-focused rigs saw a slight decline. The Permian Basin continues to lead activity, adding rigs and maintaining its position as the most active oil-producing region in the country, while other major basins showed mixed performance.

Looking further out, expectations for U.S. production remain cautiously optimistic. Industry executives anticipate moderate production growth over the next two years, supported by efficiency improvements rather than aggressive expansion.

EIA Storage Report: According to estimates from the U.S. Energy Information Administration, working gas in storage stood at 2,063 Bcf as of Friday, April 17, 2026, reflecting a weekly increase of 103 Bcf. Storage levels were 142 Bcf higher than the same time last year and 137 Bcf above the five-year average of 1,926 Bcf. Overall, total working gas inventories remain within the historical five-year range.

Weather: Weather patterns across the United States may shift later in 2026 as El Niño conditions are increasingly expected to develop. The NOAA Climate Prediction Center has issued an El Niño watch, with forecasts calling for a transition from La Niña to ENSO-neutral conditions in the near term, followed by El Niño emerging by summer and persisting through the end of the year.

Confidence in this outlook continues to build, with some projections suggesting the potential for a stronger-than-average El Niño. In certain scenarios, sea surface temperature anomalies could climb well above normal, raising the possibility of a more impactful El Niño depending on how atmospheric and oceanic conditions evolve over the coming months.

El Niño typically shifts the Pacific jet stream southward, leading to warmer and drier conditions across the northern United States. Historically, this pattern results in milder, less snowy winters in the Midwest, while other seasons tend to see cooler, wetter conditions in late summer and fall, followed by drier trends in the spring.

In addition to temperature and precipitation impacts, El Niño often suppresses Atlantic hurricane activity. Stronger upper-level winds and increased atmospheric stability create less favorable conditions for storm development, which typically leads to a quieter hurricane season.

April 24, 2026

Weekly Energy News

Market Commentary: Natural gas markets moved lower on April 23 following the latest storage data from the U.S. Energy Information Administration. The agency reported a 103 Bcf injection into U.S. gas storage for the week ending April 17, exceeding market expectations of 95 Bcf and coming in well above both the five-year average injection of 64 Bcf and last year’s 77 Bcf build. Even with a slight downward revision to the prior week’s storage levels, the report was viewed as bearish and contributed to downward pressure on prices.

In response, NYMEX Henry Hub futures for May delivery fell immediately after the release, dropping about five cents to $2.60/MMBtu and briefly dipping below $2.57/MMBtu during intraday trading before stabilizing near $2.60 by early afternoon. The decline reflects a broader loosening in market fundamentals, driven largely by weaker demand trends.

May 2026 NYMEX closed Thursday at $2.614

· High for the day $2.74

· Low for the day $2.568

Early trading for the prompt month is trading at $2.688

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

April demand, particularly in the residential and commercial sectors, has remained well below average due to mild weather conditions. However, forecasts suggest a seasonal rebound, with demand expected to rise above the five-year average in late April and early May. Analysts note that the transition toward more typical weather patterns could provide some near-term support for prices, though the absence of early-season heat may limit bullish momentum heading into summer.

Total demand fell by nearly 7 Bcf/d in the week ending April 17, with residential and commercial demand dropping sharply and remaining significantly below historical norms. Industrial demand also declined modestly, while power sector demand provided a partial offset with a weekly increase. On the supply side, overall production edged lower, though increased imports from Canada helped mitigate some of the decline.

Looking ahead, early data for the current week shows a modest recovery in demand, particularly in the residential-commercial segment. As a result, storage injections are expected to return closer to seasonal norms. Estimates for the week ending April 24 point to an injection of approximately 62 Bcf, aligning closely with the five-year average and significantly below last year’s 105 Bcf build for the same period.

In the broader energy sector, U.S. drilling activity ticked slightly higher in mid-April. Total active rigs increased to 577, driven by gains in oil-directed drilling, while natural gas-focused rigs saw a slight decline. The Permian Basin continues to lead activity, adding rigs and maintaining its position as the most active oil-producing region in the country, while other major basins showed mixed performance.

Looking further out, expectations for U.S. production remain cautiously optimistic. Industry executives anticipate moderate production growth over the next two years, supported by efficiency improvements rather than aggressive expansion.

EIA Storage Report: According to estimates from the U.S. Energy Information Administration, working gas in storage stood at 2,063 Bcf as of Friday, April 17, 2026, reflecting a weekly increase of 103 Bcf. Storage levels were 142 Bcf higher than the same time last year and 137 Bcf above the five-year average of 1,926 Bcf. Overall, total working gas inventories remain within the historical five-year range.

Weather: Weather patterns across the United States may shift later in 2026 as El Niño conditions are increasingly expected to develop. The NOAA Climate Prediction Center has issued an El Niño watch, with forecasts calling for a transition from La Niña to ENSO-neutral conditions in the near term, followed by El Niño emerging by summer and persisting through the end of the year.

Confidence in this outlook continues to build, with some projections suggesting the potential for a stronger-than-average El Niño. In certain scenarios, sea surface temperature anomalies could climb well above normal, raising the possibility of a more impactful El Niño depending on how atmospheric and oceanic conditions evolve over the coming months.

El Niño typically shifts the Pacific jet stream southward, leading to warmer and drier conditions across the northern United States. Historically, this pattern results in milder, less snowy winters in the Midwest, while other seasons tend to see cooler, wetter conditions in late summer and fall, followed by drier trends in the spring.

In addition to temperature and precipitation impacts, El Niño often suppresses Atlantic hurricane activity. Stronger upper-level winds and increased atmospheric stability create less favorable conditions for storm development, which typically leads to a quieter hurricane season.

Make Your Choice Gas Selection in Three Easy Steps

Click here to access our online tool, or call our Choice gas commodity experts at 1 (877) 790-4990.

Step 1: Enter your account number

- Your Black Hills Energy account number is located at the top right-hand corner of your bill.

Step 2: Review price options and make your selection

Step 3: Confirm your selection and enter your control number

- You received a control number in your 2026 Choice Gas selection packet mailed to you from Black Hills Energy. If you cannot locate this, you can retrieve your control number by calling 877-245-3506 or visit choicegas.com

Once enrolled, you will be removed from supplier marketing communications within 24 hours.

Sign Up for Our Energy Newsletters

Sign UpRecent Posts