April 17, 2026

Weekly Energy News

Market Commentary: NYMEX May natural gas futures rose roughly $0.05 to settle near $2.66/MMBtu on April 16, rebounding after testing mid-$2.50 levels the prior day. The move higher is largely driven by a mid-April cold front expected to bring cooler temperatures across the Midcontinent and Eastern U.S. over the next several days.

As a result, U.S. residential and commercial demand is projected to increase significantly, rising from about 12.3 Bcf/d on April 16 to an estimated 22–23 Bcf/d by April 19–20. Short-term, this demand spike—combined with tighter supply readings and steady LNG flows—could support prices over the next week.

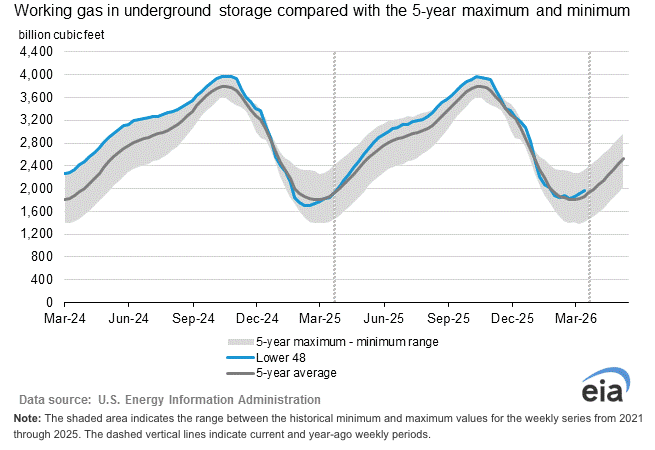

However, the broader market remains pressured by a growing storage surplus. Current inventories sit about 108 Bcf above normal and could expand to more than 170 Bcf by early May, which may weigh on prices longer term.

Looking ahead, the next storage report is expected to show another sizable injection. Early estimates point to a build near 87 Bcf for the week ending April 17—well above the five-year average of 64 Bcf and higher than last year’s 77 Bcf injection for the same period.

May 2026 NYMEX closed Thursday at $2.647

· High for the day $2.668

· Low for the day $2.588

Early trading for the prompt month is trading at $2.644

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

LNG Export Outlook: The U.S. Energy Information Administration (EIA) expects strong growth in LNG exports through 2027, driven by new export capacity and sustained global demand. U.S. LNG exports are forecast to average 17.0 Bcf/d in 2026, an increase of 1.9 Bcf/d, followed by another 9% rise in 2027. Pipeline exports are also expected to grow modestly over the same period.

Growth is being supported by global supply disruptions, particularly in Qatar, where outages and facility damage have tightened LNG availability. These disruptions—impacting roughly 20% of global supply—are increasing demand for U.S. LNG and helping keep export facilities running at high utilization rates.

On the supply side, U.S. export capacity continues to expand. Several major projects—including Corpus Christi Stage 3 and Golden Pass LNG—are set to begin operations in 2026, with additional facilities such as Port Arthur LNG and Rio Grande LNG expected online in 2027. Incremental capacity expansions at existing terminals are also contributing to overall growth.

Europe remains the primary destination for U.S. LNG, accounting for more than two-thirds of exports in 2025, with volumes reaching record levels. Meanwhile, exports to Asia declined, largely due to reduced shipments to China amid ongoing trade tensions. Other regions, including Egypt, saw notable increases in U.S. LNG imports.

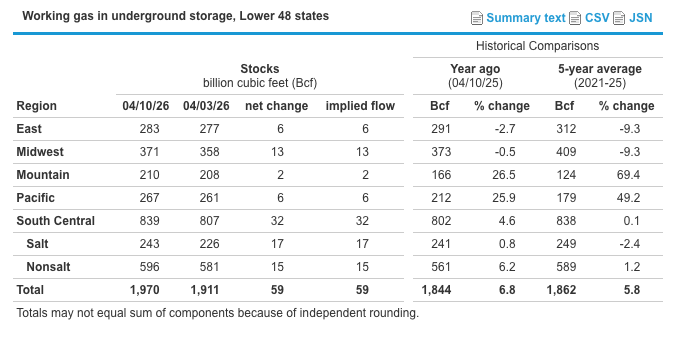

EIA Storage Update: The U.S. Energy Information Administration reported a 59 Bcf injection for the week ending April 10, exceeding market expectations. In response, NYMEX May futures hovered near $2.64/MMBtu immediately following the release before climbing modestly to around $2.66/MMBtu.

The reported build was above both analyst expectations (55 Bcf) and the five-year average of 38 Bcf for this time of year. It also surpassed last year’s 22 Bcf injection, reflecting relatively mild spring weather and reduced heating demand.

Weather: According to NOAA’s Long-Lead Seasonal Outlook, ENSO-neutral conditions are in place, with a transition to El Niño expected by early summer and likely to persist through the end of 2026.

Temperatures for May–July 2026 are expected to run above normal across most of the U.S., supporting stronger early-season cooling demand. The highest confidence (60–70%) for above-normal temperatures is centered over the Rockies and Great Basin.

The South and Southeast are also favored to be warmer than normal, though with slightly lower confidence (50–60%).

The main exception is the northern Plains, Upper Midwest, and Great Lakes, where temperature signals are weaker and near-normal conditions are most likely.

Alaska is also expected to experience above-normal temperatures.

Bottom line: Widespread warmth is expected to dominate the early summer period, with the strongest heat risk in the western U.S., while parts of the northern tier may see more moderate conditions.

Market Data:

April 17, 2026

Weekly Energy News

April 17, 2026

Market Commentary: NYMEX May natural gas futures rose roughly $0.05 to settle near $2.66/MMBtu on April 16, rebounding after testing mid-$2.50 levels the prior day. The move higher is largely driven by a mid-April cold front expected to bring cooler temperatures across the Midcontinent and Eastern U.S. over the next several days.

As a result, U.S. residential and commercial demand is projected to increase significantly, rising from about 12.3 Bcf/d on April 16 to an estimated 22–23 Bcf/d by April 19–20. Short-term, this demand spike—combined with tighter supply readings and steady LNG flows—could support prices over the next week.

However, the broader market remains pressured by a growing storage surplus. Current inventories sit about 108 Bcf above normal and could expand to more than 170 Bcf by early May, which may weigh on prices longer term.

Looking ahead, the next storage report is expected to show another sizable injection. Early estimates point to a build near 87 Bcf for the week ending April 17—well above the five-year average of 64 Bcf and higher than last year’s 77 Bcf injection for the same period.

May 2026 NYMEX closed Thursday at $2.647

· High for the day $2.668

· Low for the day $2.588

Early trading for the prompt month is trading at $2.644

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

LNG Export Outlook: The U.S. Energy Information Administration (EIA) expects strong growth in LNG exports through 2027, driven by new export capacity and sustained global demand. U.S. LNG exports are forecast to average 17.0 Bcf/d in 2026, an increase of 1.9 Bcf/d, followed by another 9% rise in 2027. Pipeline exports are also expected to grow modestly over the same period.

Growth is being supported by global supply disruptions, particularly in Qatar, where outages and facility damage have tightened LNG availability. These disruptions—impacting roughly 20% of global supply—are increasing demand for U.S. LNG and helping keep export facilities running at high utilization rates.

On the supply side, U.S. export capacity continues to expand. Several major projects—including Corpus Christi Stage 3 and Golden Pass LNG—are set to begin operations in 2026, with additional facilities such as Port Arthur LNG and Rio Grande LNG expected online in 2027. Incremental capacity expansions at existing terminals are also contributing to overall growth.

Europe remains the primary destination for U.S. LNG, accounting for more than two-thirds of exports in 2025, with volumes reaching record levels. Meanwhile, exports to Asia declined, largely due to reduced shipments to China amid ongoing trade tensions. Other regions, including Egypt, saw notable increases in U.S. LNG imports.

EIA Storage Update: The U.S. Energy Information Administration reported a 59 Bcf injection for the week ending April 10, exceeding market expectations. In response, NYMEX May futures hovered near $2.64/MMBtu immediately following the release before climbing modestly to around $2.66/MMBtu.

The reported build was above both analyst expectations (55 Bcf) and the five-year average of 38 Bcf for this time of year. It also surpassed last year’s 22 Bcf injection, reflecting relatively mild spring weather and reduced heating demand.

Weather: According to NOAA’s Long-Lead Seasonal Outlook, ENSO-neutral conditions are in place, with a transition to El Niño expected by early summer and likely to persist through the end of 2026.

Temperatures for May–July 2026 are expected to run above normal across most of the U.S., supporting stronger early-season cooling demand. The highest confidence (60–70%) for above-normal temperatures is centered over the Rockies and Great Basin.

The South and Southeast are also favored to be warmer than normal, though with slightly lower confidence (50–60%).

The main exception is the northern Plains, Upper Midwest, and Great Lakes, where temperature signals are weaker and near-normal conditions are most likely.

Alaska is also expected to experience above-normal temperatures.

Bottom line: Widespread warmth is expected to dominate the early summer period, with the strongest heat risk in the western U.S., while parts of the northern tier may see more moderate conditions.

Market Data:

April 17, 2026

April 17, 2026

Weekly Energy News

Market Commentary: NYMEX May natural gas futures rose roughly $0.05 to settle near $2.66/MMBtu on April 16, rebounding after testing mid-$2.50 levels the prior day. The move higher is largely driven by a mid-April cold front expected to bring cooler temperatures across the Midcontinent and Eastern U.S. over the next several days.

As a result, U.S. residential and commercial demand is projected to increase significantly, rising from about 12.3 Bcf/d on April 16 to an estimated 22–23 Bcf/d by April 19–20. Short-term, this demand spike—combined with tighter supply readings and steady LNG flows—could support prices over the next week.

However, the broader market remains pressured by a growing storage surplus. Current inventories sit about 108 Bcf above normal and could expand to more than 170 Bcf by early May, which may weigh on prices longer term.

Looking ahead, the next storage report is expected to show another sizable injection. Early estimates point to a build near 87 Bcf for the week ending April 17—well above the five-year average of 64 Bcf and higher than last year’s 77 Bcf injection for the same period.

May 2026 NYMEX closed Thursday at $2.647

· High for the day $2.668

· Low for the day $2.588

Early trading for the prompt month is trading at $2.644

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

LNG Export Outlook: The U.S. Energy Information Administration (EIA) expects strong growth in LNG exports through 2027, driven by new export capacity and sustained global demand. U.S. LNG exports are forecast to average 17.0 Bcf/d in 2026, an increase of 1.9 Bcf/d, followed by another 9% rise in 2027. Pipeline exports are also expected to grow modestly over the same period.

Growth is being supported by global supply disruptions, particularly in Qatar, where outages and facility damage have tightened LNG availability. These disruptions—impacting roughly 20% of global supply—are increasing demand for U.S. LNG and helping keep export facilities running at high utilization rates.

On the supply side, U.S. export capacity continues to expand. Several major projects—including Corpus Christi Stage 3 and Golden Pass LNG—are set to begin operations in 2026, with additional facilities such as Port Arthur LNG and Rio Grande LNG expected online in 2027. Incremental capacity expansions at existing terminals are also contributing to overall growth.

Europe remains the primary destination for U.S. LNG, accounting for more than two-thirds of exports in 2025, with volumes reaching record levels. Meanwhile, exports to Asia declined, largely due to reduced shipments to China amid ongoing trade tensions. Other regions, including Egypt, saw notable increases in U.S. LNG imports.

EIA Storage Update: The U.S. Energy Information Administration reported a 59 Bcf injection for the week ending April 10, exceeding market expectations. In response, NYMEX May futures hovered near $2.64/MMBtu immediately following the release before climbing modestly to around $2.66/MMBtu.

The reported build was above both analyst expectations (55 Bcf) and the five-year average of 38 Bcf for this time of year. It also surpassed last year’s 22 Bcf injection, reflecting relatively mild spring weather and reduced heating demand.

Weather: According to NOAA’s Long-Lead Seasonal Outlook, ENSO-neutral conditions are in place, with a transition to El Niño expected by early summer and likely to persist through the end of 2026.

Temperatures for May–July 2026 are expected to run above normal across most of the U.S., supporting stronger early-season cooling demand. The highest confidence (60–70%) for above-normal temperatures is centered over the Rockies and Great Basin.

The South and Southeast are also favored to be warmer than normal, though with slightly lower confidence (50–60%).

The main exception is the northern Plains, Upper Midwest, and Great Lakes, where temperature signals are weaker and near-normal conditions are most likely.

Alaska is also expected to experience above-normal temperatures.

Bottom line: Widespread warmth is expected to dominate the early summer period, with the strongest heat risk in the western U.S., while parts of the northern tier may see more moderate conditions.

April 17, 2026

Weekly Energy News

Market Commentary: NYMEX May natural gas futures rose roughly $0.05 to settle near $2.66/MMBtu on April 16, rebounding after testing mid-$2.50 levels the prior day. The move higher is largely driven by a mid-April cold front expected to bring cooler temperatures across the Midcontinent and Eastern U.S. over the next several days.

As a result, U.S. residential and commercial demand is projected to increase significantly, rising from about 12.3 Bcf/d on April 16 to an estimated 22–23 Bcf/d by April 19–20. Short-term, this demand spike—combined with tighter supply readings and steady LNG flows—could support prices over the next week.

However, the broader market remains pressured by a growing storage surplus. Current inventories sit about 108 Bcf above normal and could expand to more than 170 Bcf by early May, which may weigh on prices longer term.

Looking ahead, the next storage report is expected to show another sizable injection. Early estimates point to a build near 87 Bcf for the week ending April 17—well above the five-year average of 64 Bcf and higher than last year’s 77 Bcf injection for the same period.

May 2026 NYMEX closed Thursday at $2.647

· High for the day $2.668

· Low for the day $2.588

Early trading for the prompt month is trading at $2.644

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

LNG Export Outlook: The U.S. Energy Information Administration (EIA) expects strong growth in LNG exports through 2027, driven by new export capacity and sustained global demand. U.S. LNG exports are forecast to average 17.0 Bcf/d in 2026, an increase of 1.9 Bcf/d, followed by another 9% rise in 2027. Pipeline exports are also expected to grow modestly over the same period.

Growth is being supported by global supply disruptions, particularly in Qatar, where outages and facility damage have tightened LNG availability. These disruptions—impacting roughly 20% of global supply—are increasing demand for U.S. LNG and helping keep export facilities running at high utilization rates.

On the supply side, U.S. export capacity continues to expand. Several major projects—including Corpus Christi Stage 3 and Golden Pass LNG—are set to begin operations in 2026, with additional facilities such as Port Arthur LNG and Rio Grande LNG expected online in 2027. Incremental capacity expansions at existing terminals are also contributing to overall growth.

Europe remains the primary destination for U.S. LNG, accounting for more than two-thirds of exports in 2025, with volumes reaching record levels. Meanwhile, exports to Asia declined, largely due to reduced shipments to China amid ongoing trade tensions. Other regions, including Egypt, saw notable increases in U.S. LNG imports.

EIA Storage Update: The U.S. Energy Information Administration reported a 59 Bcf injection for the week ending April 10, exceeding market expectations. In response, NYMEX May futures hovered near $2.64/MMBtu immediately following the release before climbing modestly to around $2.66/MMBtu.

The reported build was above both analyst expectations (55 Bcf) and the five-year average of 38 Bcf for this time of year. It also surpassed last year’s 22 Bcf injection, reflecting relatively mild spring weather and reduced heating demand.

Weather: According to NOAA’s Long-Lead Seasonal Outlook, ENSO-neutral conditions are in place, with a transition to El Niño expected by early summer and likely to persist through the end of 2026.

Temperatures for May–July 2026 are expected to run above normal across most of the U.S., supporting stronger early-season cooling demand. The highest confidence (60–70%) for above-normal temperatures is centered over the Rockies and Great Basin.

The South and Southeast are also favored to be warmer than normal, though with slightly lower confidence (50–60%).

The main exception is the northern Plains, Upper Midwest, and Great Lakes, where temperature signals are weaker and near-normal conditions are most likely.

Alaska is also expected to experience above-normal temperatures.

Bottom line: Widespread warmth is expected to dominate the early summer period, with the strongest heat risk in the western U.S., while parts of the northern tier may see more moderate conditions.

April 17, 2026

Weekly Energy News

Market Commentary: NYMEX May natural gas futures rose roughly $0.05 to settle near $2.66/MMBtu on April 16, rebounding after testing mid-$2.50 levels the prior day. The move higher is largely driven by a mid-April cold front expected to bring cooler temperatures across the Midcontinent and Eastern U.S. over the next several days.

As a result, U.S. residential and commercial demand is projected to increase significantly, rising from about 12.3 Bcf/d on April 16 to an estimated 22–23 Bcf/d by April 19–20. Short-term, this demand spike—combined with tighter supply readings and steady LNG flows—could support prices over the next week.

However, the broader market remains pressured by a growing storage surplus. Current inventories sit about 108 Bcf above normal and could expand to more than 170 Bcf by early May, which may weigh on prices longer term.

Looking ahead, the next storage report is expected to show another sizable injection. Early estimates point to a build near 87 Bcf for the week ending April 17—well above the five-year average of 64 Bcf and higher than last year’s 77 Bcf injection for the same period.

May 2026 NYMEX closed Thursday at $2.647

· High for the day $2.668

· Low for the day $2.588

Early trading for the prompt month is trading at $2.644

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

LNG Export Outlook: The U.S. Energy Information Administration (EIA) expects strong growth in LNG exports through 2027, driven by new export capacity and sustained global demand. U.S. LNG exports are forecast to average 17.0 Bcf/d in 2026, an increase of 1.9 Bcf/d, followed by another 9% rise in 2027. Pipeline exports are also expected to grow modestly over the same period.

Growth is being supported by global supply disruptions, particularly in Qatar, where outages and facility damage have tightened LNG availability. These disruptions—impacting roughly 20% of global supply—are increasing demand for U.S. LNG and helping keep export facilities running at high utilization rates.

On the supply side, U.S. export capacity continues to expand. Several major projects—including Corpus Christi Stage 3 and Golden Pass LNG—are set to begin operations in 2026, with additional facilities such as Port Arthur LNG and Rio Grande LNG expected online in 2027. Incremental capacity expansions at existing terminals are also contributing to overall growth.

Europe remains the primary destination for U.S. LNG, accounting for more than two-thirds of exports in 2025, with volumes reaching record levels. Meanwhile, exports to Asia declined, largely due to reduced shipments to China amid ongoing trade tensions. Other regions, including Egypt, saw notable increases in U.S. LNG imports.

EIA Storage Update: The U.S. Energy Information Administration reported a 59 Bcf injection for the week ending April 10, exceeding market expectations. In response, NYMEX May futures hovered near $2.64/MMBtu immediately following the release before climbing modestly to around $2.66/MMBtu.

The reported build was above both analyst expectations (55 Bcf) and the five-year average of 38 Bcf for this time of year. It also surpassed last year’s 22 Bcf injection, reflecting relatively mild spring weather and reduced heating demand.

Weather: According to NOAA’s Long-Lead Seasonal Outlook, ENSO-neutral conditions are in place, with a transition to El Niño expected by early summer and likely to persist through the end of 2026.

Temperatures for May–July 2026 are expected to run above normal across most of the U.S., supporting stronger early-season cooling demand. The highest confidence (60–70%) for above-normal temperatures is centered over the Rockies and Great Basin.

The South and Southeast are also favored to be warmer than normal, though with slightly lower confidence (50–60%).

The main exception is the northern Plains, Upper Midwest, and Great Lakes, where temperature signals are weaker and near-normal conditions are most likely.

Alaska is also expected to experience above-normal temperatures.

Bottom line: Widespread warmth is expected to dominate the early summer period, with the strongest heat risk in the western U.S., while parts of the northern tier may see more moderate conditions.

April 17, 2026

Market Commentary: NYMEX May natural gas futures rose roughly $0.05 to settle near $2.66/MMBtu on April 16, rebounding after testing mid-$2.50 levels the prior day. The move higher is largely driven by a mid-April cold front expected to bring cooler temperatures across the Midcontinent and Eastern U.S. over the next several days.

As a result, U.S. residential and commercial demand is projected to increase significantly, rising from about 12.3 Bcf/d on April 16 to an estimated 22–23 Bcf/d by April 19–20. Short-term, this demand spike—combined with tighter supply readings and steady LNG flows—could support prices over the next week.

However, the broader market remains pressured by a growing storage surplus. Current inventories sit about 108 Bcf above normal and could expand to more than 170 Bcf by early May, which may weigh on prices longer term.

Looking ahead, the next storage report is expected to show another sizable injection. Early estimates point to a build near 87 Bcf for the week ending April 17—well above the five-year average of 64 Bcf and higher than last year’s 77 Bcf injection for the same period.

May 2026 NYMEX closed Thursday at $2.647

· High for the day $2.668

· Low for the day $2.588

Early trading for the prompt month is trading at $2.644

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

LNG Export Outlook: The U.S. Energy Information Administration (EIA) expects strong growth in LNG exports through 2027, driven by new export capacity and sustained global demand. U.S. LNG exports are forecast to average 17.0 Bcf/d in 2026, an increase of 1.9 Bcf/d, followed by another 9% rise in 2027. Pipeline exports are also expected to grow modestly over the same period.

Growth is being supported by global supply disruptions, particularly in Qatar, where outages and facility damage have tightened LNG availability. These disruptions—impacting roughly 20% of global supply—are increasing demand for U.S. LNG and helping keep export facilities running at high utilization rates.

On the supply side, U.S. export capacity continues to expand. Several major projects—including Corpus Christi Stage 3 and Golden Pass LNG—are set to begin operations in 2026, with additional facilities such as Port Arthur LNG and Rio Grande LNG expected online in 2027. Incremental capacity expansions at existing terminals are also contributing to overall growth.

Europe remains the primary destination for U.S. LNG, accounting for more than two-thirds of exports in 2025, with volumes reaching record levels. Meanwhile, exports to Asia declined, largely due to reduced shipments to China amid ongoing trade tensions. Other regions, including Egypt, saw notable increases in U.S. LNG imports.

EIA Storage Update: The U.S. Energy Information Administration reported a 59 Bcf injection for the week ending April 10, exceeding market expectations. In response, NYMEX May futures hovered near $2.64/MMBtu immediately following the release before climbing modestly to around $2.66/MMBtu.

The reported build was above both analyst expectations (55 Bcf) and the five-year average of 38 Bcf for this time of year. It also surpassed last year’s 22 Bcf injection, reflecting relatively mild spring weather and reduced heating demand.

Weather: According to NOAA’s Long-Lead Seasonal Outlook, ENSO-neutral conditions are in place, with a transition to El Niño expected by early summer and likely to persist through the end of 2026.

Temperatures for May–July 2026 are expected to run above normal across most of the U.S., supporting stronger early-season cooling demand. The highest confidence (60–70%) for above-normal temperatures is centered over the Rockies and Great Basin.

The South and Southeast are also favored to be warmer than normal, though with slightly lower confidence (50–60%).

The main exception is the northern Plains, Upper Midwest, and Great Lakes, where temperature signals are weaker and near-normal conditions are most likely.

Alaska is also expected to experience above-normal temperatures.

Bottom line: Widespread warmth is expected to dominate the early summer period, with the strongest heat risk in the western U.S., while parts of the northern tier may see more moderate conditions.

April 17, 2026

Weekly Energy News

Market Commentary: NYMEX May natural gas futures rose roughly $0.05 to settle near $2.66/MMBtu on April 16, rebounding after testing mid-$2.50 levels the prior day. The move higher is largely driven by a mid-April cold front expected to bring cooler temperatures across the Midcontinent and Eastern U.S. over the next several days.

As a result, U.S. residential and commercial demand is projected to increase significantly, rising from about 12.3 Bcf/d on April 16 to an estimated 22–23 Bcf/d by April 19–20. Short-term, this demand spike—combined with tighter supply readings and steady LNG flows—could support prices over the next week.

However, the broader market remains pressured by a growing storage surplus. Current inventories sit about 108 Bcf above normal and could expand to more than 170 Bcf by early May, which may weigh on prices longer term.

Looking ahead, the next storage report is expected to show another sizable injection. Early estimates point to a build near 87 Bcf for the week ending April 17—well above the five-year average of 64 Bcf and higher than last year’s 77 Bcf injection for the same period.

May 2026 NYMEX closed Thursday at $2.647

· High for the day $2.668

· Low for the day $2.588

Early trading for the prompt month is trading at $2.644

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

LNG Export Outlook: The U.S. Energy Information Administration (EIA) expects strong growth in LNG exports through 2027, driven by new export capacity and sustained global demand. U.S. LNG exports are forecast to average 17.0 Bcf/d in 2026, an increase of 1.9 Bcf/d, followed by another 9% rise in 2027. Pipeline exports are also expected to grow modestly over the same period.

Growth is being supported by global supply disruptions, particularly in Qatar, where outages and facility damage have tightened LNG availability. These disruptions—impacting roughly 20% of global supply—are increasing demand for U.S. LNG and helping keep export facilities running at high utilization rates.

On the supply side, U.S. export capacity continues to expand. Several major projects—including Corpus Christi Stage 3 and Golden Pass LNG—are set to begin operations in 2026, with additional facilities such as Port Arthur LNG and Rio Grande LNG expected online in 2027. Incremental capacity expansions at existing terminals are also contributing to overall growth.

Europe remains the primary destination for U.S. LNG, accounting for more than two-thirds of exports in 2025, with volumes reaching record levels. Meanwhile, exports to Asia declined, largely due to reduced shipments to China amid ongoing trade tensions. Other regions, including Egypt, saw notable increases in U.S. LNG imports.

EIA Storage Update: The U.S. Energy Information Administration reported a 59 Bcf injection for the week ending April 10, exceeding market expectations. In response, NYMEX May futures hovered near $2.64/MMBtu immediately following the release before climbing modestly to around $2.66/MMBtu.

The reported build was above both analyst expectations (55 Bcf) and the five-year average of 38 Bcf for this time of year. It also surpassed last year’s 22 Bcf injection, reflecting relatively mild spring weather and reduced heating demand.

Weather: According to NOAA’s Long-Lead Seasonal Outlook, ENSO-neutral conditions are in place, with a transition to El Niño expected by early summer and likely to persist through the end of 2026.

Temperatures for May–July 2026 are expected to run above normal across most of the U.S., supporting stronger early-season cooling demand. The highest confidence (60–70%) for above-normal temperatures is centered over the Rockies and Great Basin.

The South and Southeast are also favored to be warmer than normal, though with slightly lower confidence (50–60%).

The main exception is the northern Plains, Upper Midwest, and Great Lakes, where temperature signals are weaker and near-normal conditions are most likely.

Alaska is also expected to experience above-normal temperatures.

Bottom line: Widespread warmth is expected to dominate the early summer period, with the strongest heat risk in the western U.S., while parts of the northern tier may see more moderate conditions.

April 17, 2026

Weekly Energy News

Market Commentary: NYMEX May natural gas futures rose roughly $0.05 to settle near $2.66/MMBtu on April 16, rebounding after testing mid-$2.50 levels the prior day. The move higher is largely driven by a mid-April cold front expected to bring cooler temperatures across the Midcontinent and Eastern U.S. over the next several days.

As a result, U.S. residential and commercial demand is projected to increase significantly, rising from about 12.3 Bcf/d on April 16 to an estimated 22–23 Bcf/d by April 19–20. Short-term, this demand spike—combined with tighter supply readings and steady LNG flows—could support prices over the next week.

However, the broader market remains pressured by a growing storage surplus. Current inventories sit about 108 Bcf above normal and could expand to more than 170 Bcf by early May, which may weigh on prices longer term.

Looking ahead, the next storage report is expected to show another sizable injection. Early estimates point to a build near 87 Bcf for the week ending April 17—well above the five-year average of 64 Bcf and higher than last year’s 77 Bcf injection for the same period.

May 2026 NYMEX closed Thursday at $2.647

· High for the day $2.668

· Low for the day $2.588

Early trading for the prompt month is trading at $2.644

· https://www.cmegroup.com/markets/energy/natural-gas/natural-gas.html

· https://www.fxempire.com/commodities/natural-gas

LNG Export Outlook: The U.S. Energy Information Administration (EIA) expects strong growth in LNG exports through 2027, driven by new export capacity and sustained global demand. U.S. LNG exports are forecast to average 17.0 Bcf/d in 2026, an increase of 1.9 Bcf/d, followed by another 9% rise in 2027. Pipeline exports are also expected to grow modestly over the same period.

Growth is being supported by global supply disruptions, particularly in Qatar, where outages and facility damage have tightened LNG availability. These disruptions—impacting roughly 20% of global supply—are increasing demand for U.S. LNG and helping keep export facilities running at high utilization rates.

On the supply side, U.S. export capacity continues to expand. Several major projects—including Corpus Christi Stage 3 and Golden Pass LNG—are set to begin operations in 2026, with additional facilities such as Port Arthur LNG and Rio Grande LNG expected online in 2027. Incremental capacity expansions at existing terminals are also contributing to overall growth.

Europe remains the primary destination for U.S. LNG, accounting for more than two-thirds of exports in 2025, with volumes reaching record levels. Meanwhile, exports to Asia declined, largely due to reduced shipments to China amid ongoing trade tensions. Other regions, including Egypt, saw notable increases in U.S. LNG imports.

EIA Storage Update: The U.S. Energy Information Administration reported a 59 Bcf injection for the week ending April 10, exceeding market expectations. In response, NYMEX May futures hovered near $2.64/MMBtu immediately following the release before climbing modestly to around $2.66/MMBtu.

The reported build was above both analyst expectations (55 Bcf) and the five-year average of 38 Bcf for this time of year. It also surpassed last year’s 22 Bcf injection, reflecting relatively mild spring weather and reduced heating demand.

Weather: According to NOAA’s Long-Lead Seasonal Outlook, ENSO-neutral conditions are in place, with a transition to El Niño expected by early summer and likely to persist through the end of 2026.

Temperatures for May–July 2026 are expected to run above normal across most of the U.S., supporting stronger early-season cooling demand. The highest confidence (60–70%) for above-normal temperatures is centered over the Rockies and Great Basin.

The South and Southeast are also favored to be warmer than normal, though with slightly lower confidence (50–60%).

The main exception is the northern Plains, Upper Midwest, and Great Lakes, where temperature signals are weaker and near-normal conditions are most likely.

Alaska is also expected to experience above-normal temperatures.

Bottom line: Widespread warmth is expected to dominate the early summer period, with the strongest heat risk in the western U.S., while parts of the northern tier may see more moderate conditions.

Make Your Choice Gas Selection in Three Easy Steps

Click here to access our online tool, or call our Choice gas commodity experts at 1 (877) 790-4990.

Step 1: Enter your account number

- Your Black Hills Energy account number is located at the top right-hand corner of your bill.

Step 2: Review price options and make your selection

Step 3: Confirm your selection and enter your control number

- You received a control number in your 2026 Choice Gas selection packet mailed to you from Black Hills Energy. If you cannot locate this, you can retrieve your control number by calling 877-245-3506 or visit choicegas.com

Once enrolled, you will be removed from supplier marketing communications within 24 hours.

Sign Up for Our Energy Newsletters

Sign Up